kynny/iStock via Getty Images

Shenandoah Telecommunications Company (NASDAQ:SHEN) is a mid-Atlantic company that primarily provides broadband communication services to the region, with a smaller tower colocation business.

Over the last couple of years, the share price has gone nowhere after plunging from its 2-year high of approximately $61.00 per share on July 5, 2021, to a 52-week low of $15.62 on December 30, 2022. It has since climbed to a little over $17.00 per share as I write, but there is little in the way of positive catalysts to suggest the company has a sustainable growth trajectory ahead of it.

TradingView

In this capital-intensive business companies like SHEN, they have to spend just to keep up with its competitors, and there isn’t much in the way of differentiation that allows a competitive advantage in the sector.

Having said that, its Glo Fiber business has a lot of momentum behind it and should continue to grow over the next couple of years, and possibly more, but the amount of money the company is spending to grow this business, along with maintaining its other businesses, leaves little room for sustainable profits in the years ahead.

The company has a strong enough balance sheet to continue spending on growth without putting the company in a difficult financial position, but how this will boost the performance of the company over the long term has yet to be answered, since it competes in a very defined region of the country.

In this article we’ll look at its latest earnings numbers, Glo Fiber, and why the path to sustainable growth and profitability isn’t clear.

Some of the numbers

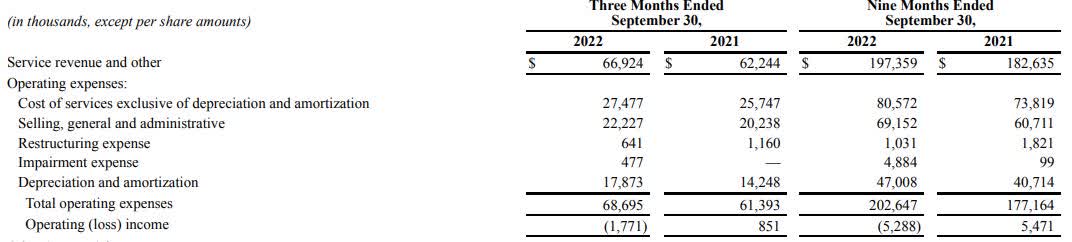

Revenue in the third quarter of 2022 was $66.9 million, up 7 percent from revenue of $62.2 million in the third quarter of 2021. Revenue in the first nine months of 2022 was $197.4 million, compared to revenue of $182.6 million in the first nine months of 2021.

Operating expenses continued to climb, coming in at $68.7 million in the third quarter of 2022, for an operating loss of $1.77 million, compared to $851,000 gain in the third quarter of 2021, on total operating expenses of $61.4 million. Operating expenses for the first nine months of 2022 were $202.6 million, for a loss of $5.3 million, compared to operating expenses of $177.2 million in the first nine months of 2021, for a gain of $5.5 million.

Company 10-Q

Adjusted EBITDA in the reporting period was $19.0 million, up 0.2 percent from adjusted EBITDA of $18.9 in the same quarter last year.

Net loss in the reporting period was $(2.7) million, or $(0.05) per diluted share, missing by $0.07. Net loss in the first nine months of 2022 was $(6.6) million, or $(0.13) per diluted share.

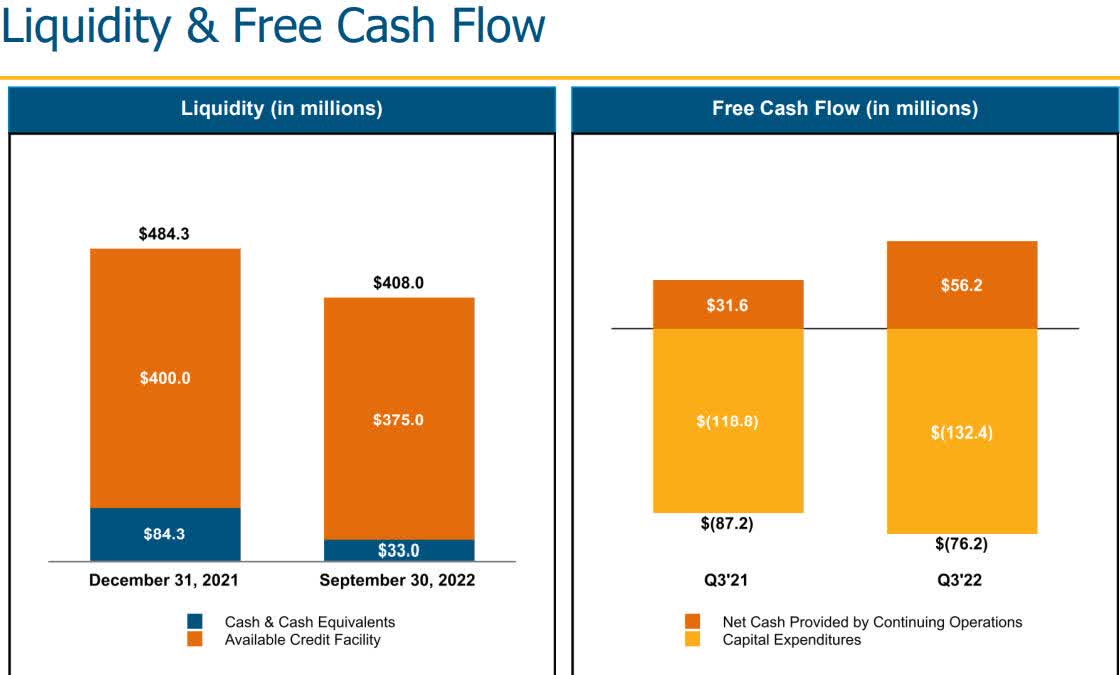

CapEx in the first nine months of 2022 was $132.4 million, up $13.6 million from CapEX of $118.8 million in the first nine months of 2021. The increase was attributed to higher spending concerning the expansion of its Glo Fiber network in its Broadband segment.

At the end of the third quarter of 2022 the company had cash and cash equivalents of $33.0 million and $375 million available under its delayed draw term loans and revolving line of credit. The company had long-term debt of approximately $25 million at the end of the quarter, with no material debt maturities until 2026.

Investor Presentation

Free cash flow was negative $(76.2) million, compared to negative free cash flow of $(87.2) million in the third quarter of 2021.

Segment performance

Broadband segment

Revenue from its Broadband segment was $62.4 million in the third quarter, up 7.7 percent from revenue of $57.9 million in the third quarter of 2021. Of that, $48.7 million came from residential and SMB.

Adjusted EBITDA in the segment for the reporting period was $22.2 million, with an adjusted EBITDA margin of 35.7 percent, compared to adjusted EBITDA of $22.3 million in the third quarter of 2021, with an adjusted EBITDA margin of 38.5 percent.

Investor Presentation

Tower segment

In its Tower segment the company generated revenue of $4.7 million in the reporting period, up 5.1 percent from the $4.4 million in revenue generated in the third quarter of 2021.

Adjusted EBITDA in the third quarter of 2022 was $3.0 million, with an adjusted EBITDA margin of 64.9 percent, compared to adjusted EBITDA of $2.6 million in the third quarter of 2021, with an adjusted EBITDA margin of 59.3 percent.

For those that don’t know, its Tower segment owns cell towers, where it leases out colocation space to generate revenue.

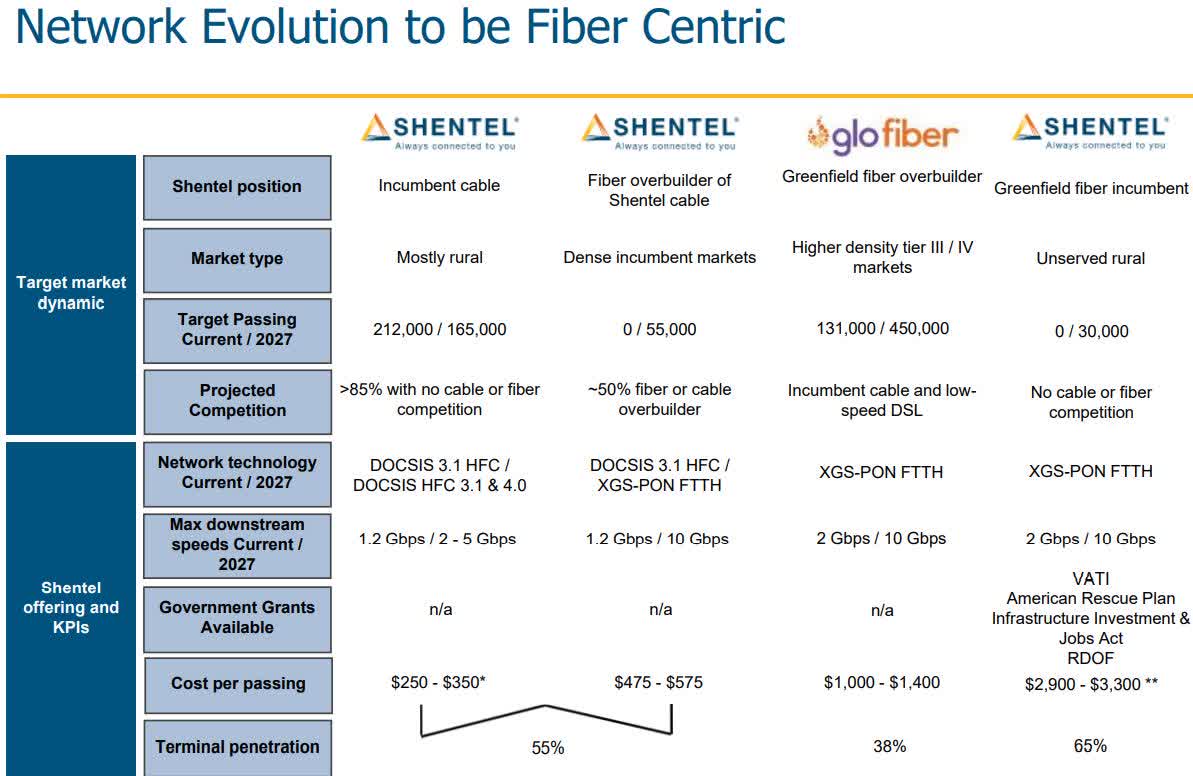

Glo Fiber

Revenue from Glo Fiber continues to soar, increasing 20 percent sequentially, and soaring 116 percent year-over-year. For the first time since SHEN launched Glo Fiber three years ago, it contributed positive adjusted EBITDA for the first time, even though it was incrementally. That could bode well for the future of the company if that improves in the quarters and years ahead as it scales.

Management believes momentum will continue with Glo Fiber and will continue to boost share with its fiber-to-the-home platform.

Investor Presentation

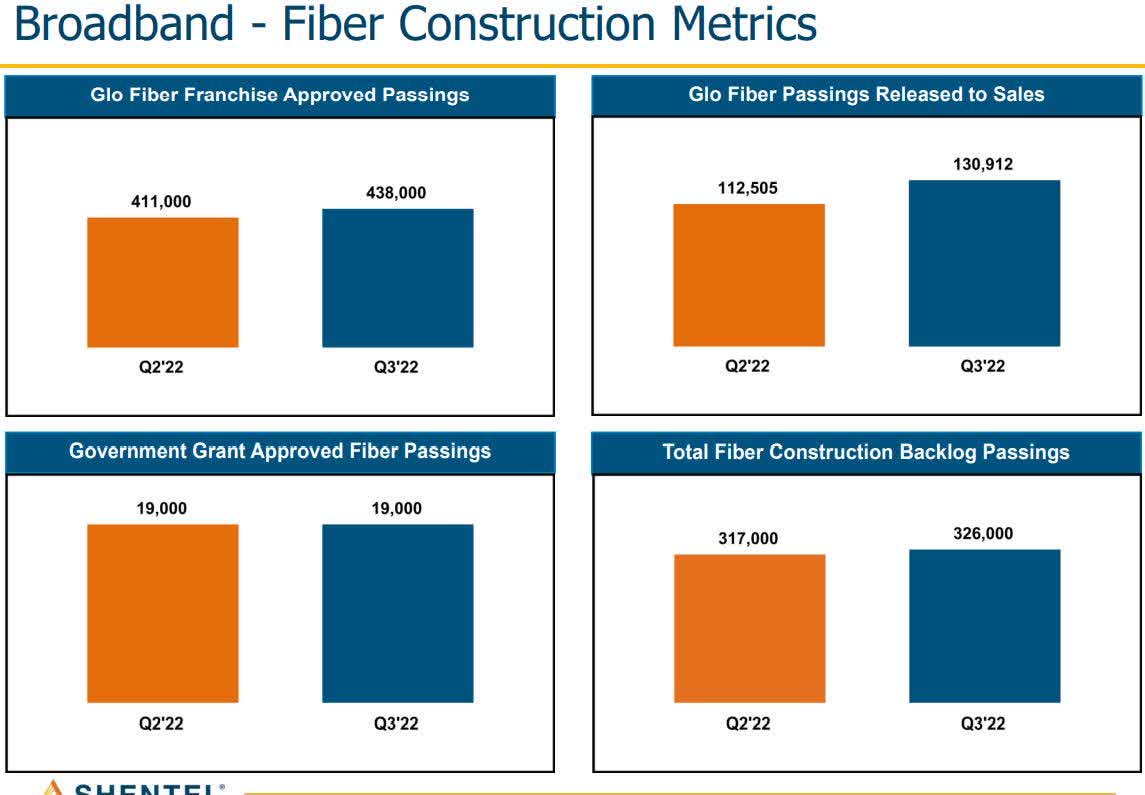

The company added over 18,000 new Glo Fiber passings in the third quarter of 2022, increasing the total number to approximately 131,000 passings. By the end of 2026, the company believes it has a visible path to surpass 450,000 passings, with an average cost capacity between $1,000 and $1,400. Costs in 2022 have been in the lower half of the range, but labor and material inflation are expected to push it to the higher end of the range in the years ahead. As of the end of the third quarter of 2022, 76 percent of Glo Fiber customers were solely single-play broadband, 19 percent were double-play, and 5 percent were triple-play.

In the reporting period churn in Glo Fiber improved by 12 basis points in comparison to the third quarter of 2021, to 1.2 percent.

Conclusion

The company has been spending a lot to maintain and attempt to grow its business, and has plans to continue to do so, with the company allocating $74 million for upgrading its cable networks in order support multi-gig services over the next 5 years. That’s one of the pieces of the puzzle pointing to the company needing to spend a lot of capital just for upgrades; that’s what I mean when pointing to the company just being able to tread water.

Management reinforced that when stating it expects adjusted EBITDA margins in broadband to slightly improve on an annual basis. What improvement it does have with adjusted EBITDA margins will come from Glo Fiber scaling, and the costs associated with softer development ease in the quarters and years ahead. With the company primarily focusing on the growth of its Glo Fiber business, it’s going to continue to dedicate a significant amount of CapEx to accelerate growth in the unit. With some of the costs being removed out of operations and expected incremental adjusted EBITDA margin contribution as it scales, the company could start to slowly move toward profitability, although at a very modest pace.

The bottom line to me is SHEN operates in a capital-intensive business that requires a lot of spend for upgrades in a sector where it’s getting hard to differentiate in the minds of customers.

In urban markets it should be able to grow its Glo Fiber business at a nice pace over at least the next couple of years, and that should modestly improve the top and bottom lines of the company, all other things being equal.

Even so, there just aren’t enough catalysts to drive growth at a pace it would meaningfully drive the share price of the company up.

Be the first to comment