Chunumunu

Quick Introduction To Business Development Companies (“BDCs”)

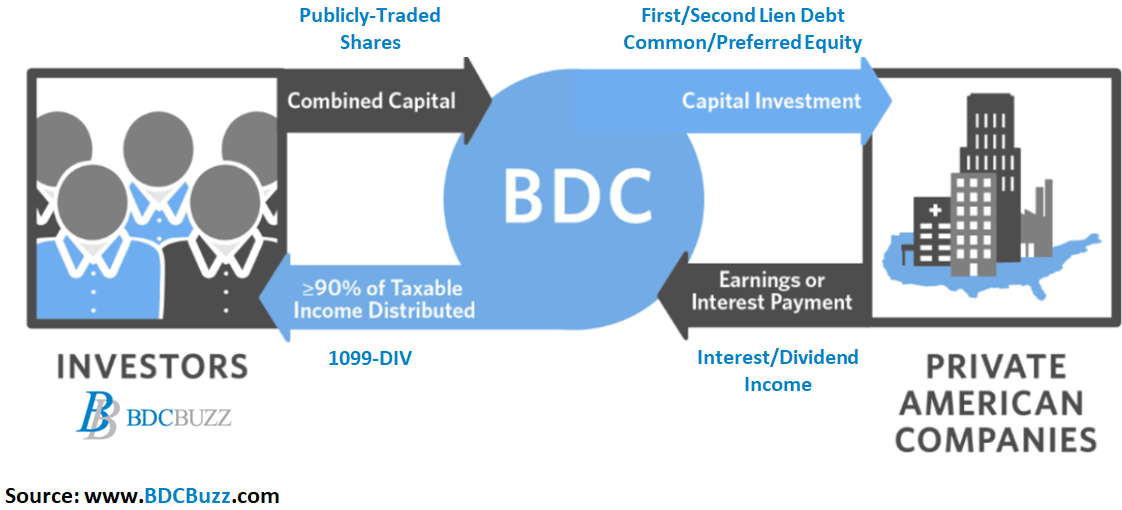

Business development companies (“BDCs”) invest shareholder capital in privately owned, small- and medium-sized U.S. companies. BDCs aim to generate income and capital gains when the companies they invest in are sold, much like venture capital or private equity funds. Anyone can invest in BDCs, as they are public companies traded on major stock exchanges.

BDC Buzz

Investment Grade BDC Bonds/Notes

Many BDCs have investment grade (“IG”) bonds/notes for lower-risk investors that do not mind lower yields/returns. Thanks to the recent declines in fixed income, the traditional bond market is now offering some excellent values, especially in the BDC sector, and I will discuss over the coming weeks. However, many of these bonds are now rebounding and I have started making purchases of mid duration maturities, which for me is between 3 and 6 years.

Traditional bonds do not trade on stock exchanges but are available through your brokerage using CUSIP numbers with a face/maturity value of $1,000. These bonds pay interest semi-annually with a pro-rated interest payment on the purchase date. Brokerages express the trading prices as a percentage of the face value.

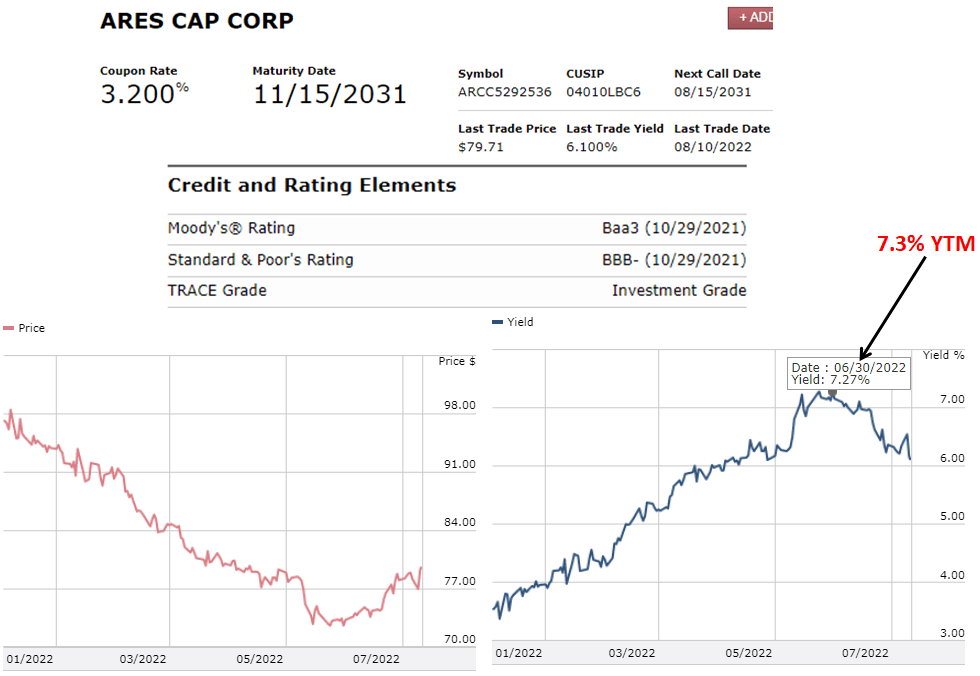

As discussed later, ARCC’s 2031 bond is currently priced at $79.71, which implies a current value of $797.10 for each bond. For more information on examples of how to trade bonds using CUSIPs and limit orders, please see the following link.

Most BDC bonds have credit ratings from Moody’s and/or S&P and so far, no BDC has ever defaulted for the reasons discussed last week in:

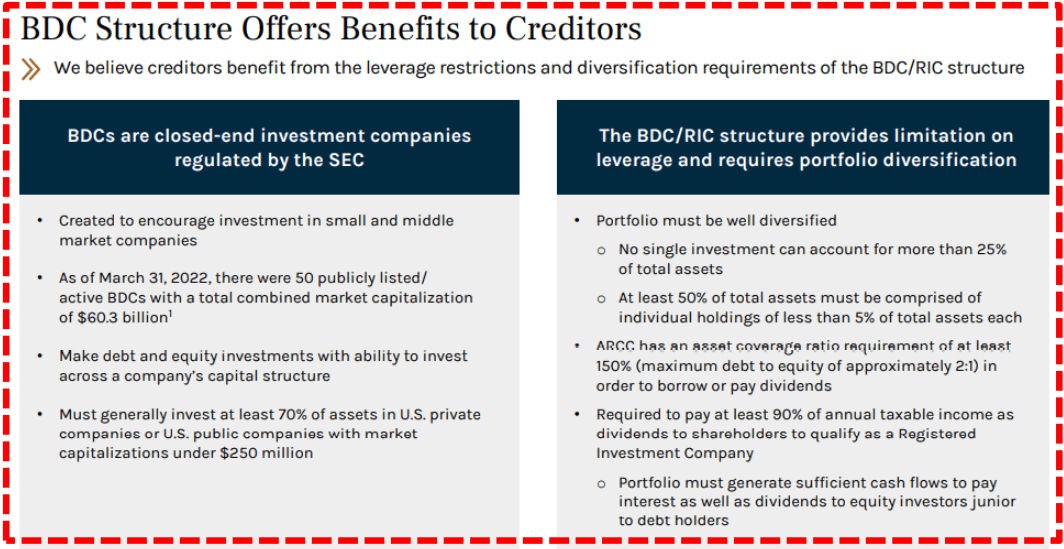

As shown below, BDCs are highly regulated with plenty of protections for investors in the common stock and debt obligations, such as the amount of leverage (asset coverage ratios discussed later), asset diversification, and having a portfolio that can “generate sufficient cash flows to pay interest as well as dividends to equity investors junior to debt holders”:

ARCC

ARCC

Ares Capital’s Investment Grade Bonds

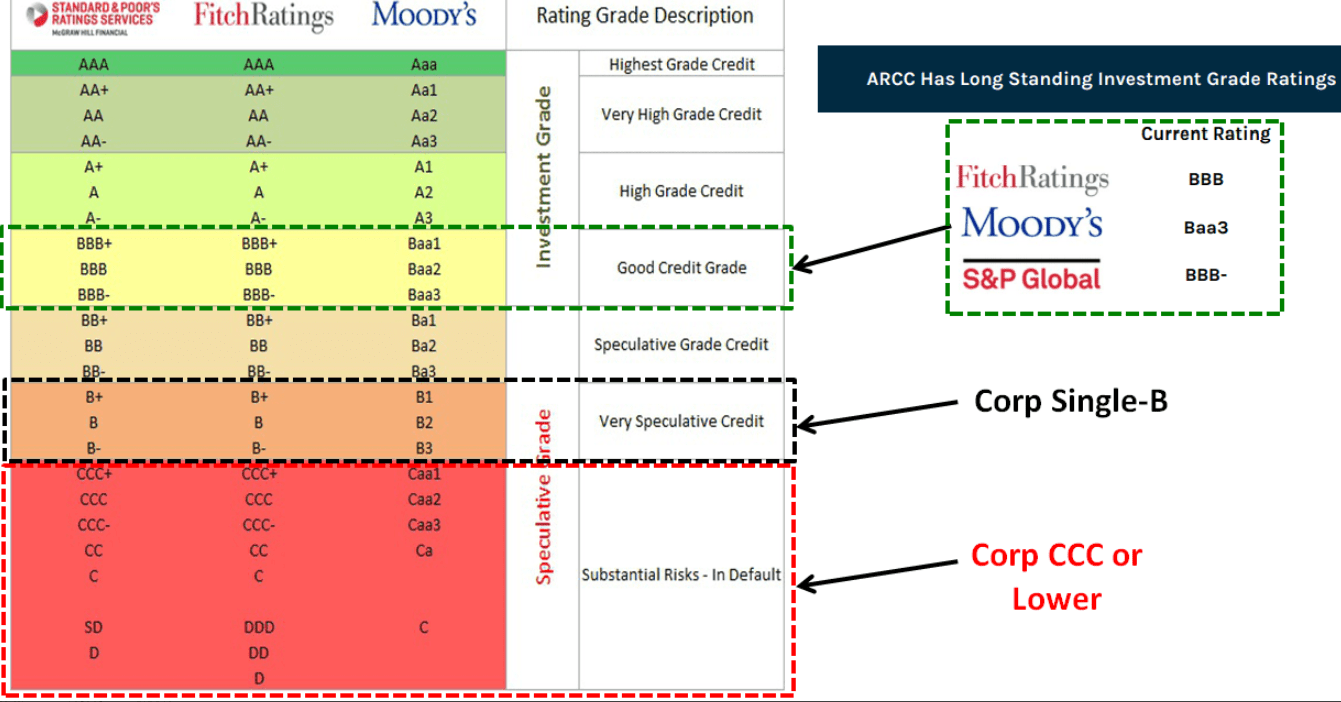

Ares Capital (NASDAQ:ARCC) has 9 investment grade bonds (CUSIPs: 04010LAU7, 04010LAX1, 04010LAV5, 04010LAY9, 04010LAZ6, 04010LBA0, 04010LBD4, 04010LBB8, 04010LBC6) that are investment grade rated by both S&P, Fitch, and Moody’s:

Credit Agencies

As discussed in the previously linked article, the “Asset Coverage Ratio” is a financial metric that measures how well a company can repay its debts by selling or liquidating its assets. The higher the asset coverage ratio, the more times a company can cover its debt. Therefore, a company with a high asset coverage ratio is considered less risky than a company with a low asset coverage ratio. BDCs are required to maintain minimum asset coverage of 150% providing strong protection to bondholders, which is one of the reasons that no publicly traded BDC has ever filed for bankruptcy nor defaulted on bond holders in the history of the sector.

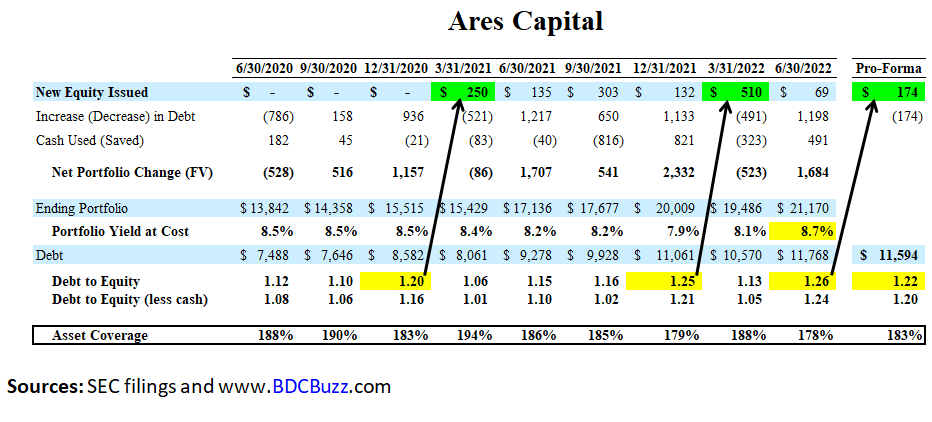

As of June 30, 2022, ARCC’s asset coverage ratio was 178%. However, on August 2, 2022, ARCC issued 9,200,000 shares at a price of $19.00 per share, resulting in net proceeds of approximately $174.4 million, after deducting discounts and commissions and estimated offering expenses.

As shown below, the pro-forma asset coverage ratio would be closer to 183% but of course does not take into account other changes including portfolio growth or exits.

BDC Buzz

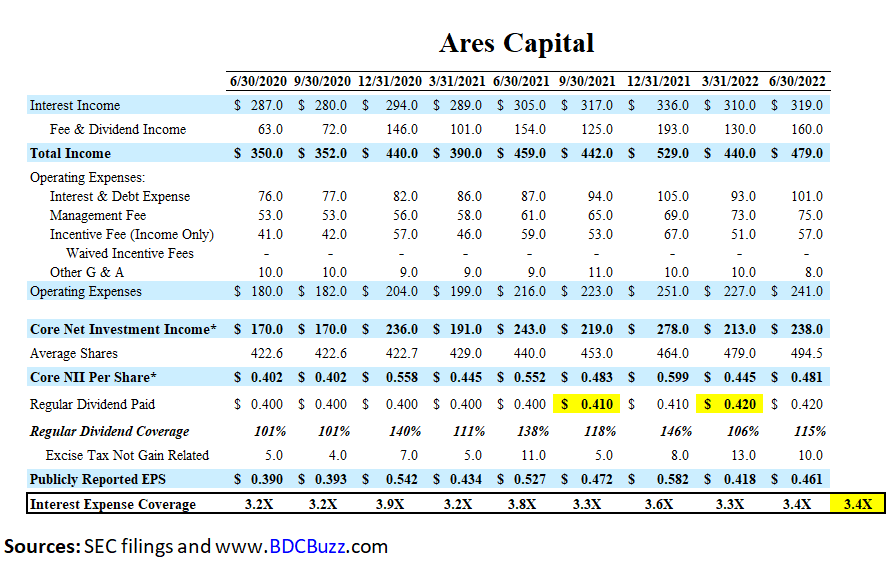

The “Interest Expense Coverage” ratio is used to see how well a company can pay the interest on outstanding debt. Also called the times-interest-earned ratio, this ratio is used by creditors and prospective lenders to assess the risk of lending capital to a firm. A higher coverage ratio is better, although the ideal ratio may vary by industry. When a company’s interest coverage ratio is only 1.5 times or lower, its ability to meet interest expenses may be questionable.

ARCC’s interest expense coverage ratio has historically averaged around 3.4 times, as shown below:

BDC Buzz

BDC Interest Rate Sensitivity Driving Dividend Increases

As predicted in previous articles, many BDCs have announced dividend increases over the last few weeks partially related to rising interest rates. My article from last month “Fixed 6.5% Return On Main Street’s Investment Grade Bond” mentioned the following:

There’s a good chance that many BDCs will be increasing dividends over the coming quarters, especially as the Fed will likely increase rates by another 75 points today [July 27, 2022], driving a significant improvement in this analysis for most BDCs

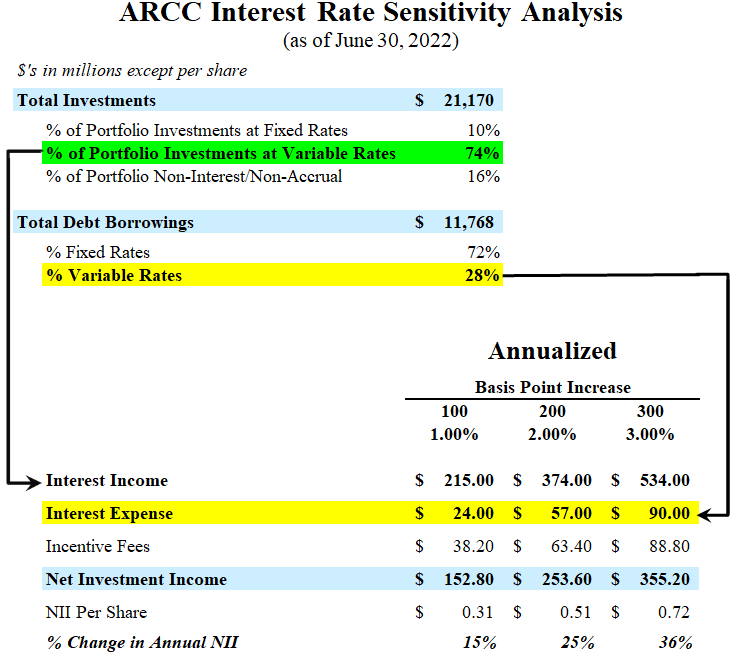

Interest rate sensitivity refers to the change in earnings that may result from changes in interest rates. As of June 30, 2022, 74% of ARCC’s portfolio investments bore interest at variable rates, 10% at fixed rates, 16% were non-interest earning or were on non-accrual status. The Revolving Credit Facility, the Revolving Funding Facility, the SMBC Funding Facility and the BNP Funding Facility bear interest at variable rates with no interest rate floors. The Unsecured Notes and the 2024 Convertible Notes bear interest at fixed rates.

Based on our estimates of increasing earnings from higher interest rates coupled with the strength of our investment portfolio, we have increased our regular quarterly dividend to $0.43 per share. Our balance sheet remains a notable source of strength with ample liquidity, moderate leverage and over 70% of our outstanding debt derived from long-dated, fixed rate unsecured notes. The second quarter increases in market rates have yet to fully flow through our earnings. We estimate our second quarter earnings would have been approximately $0.05 per share higher if the market rate increases during the second quarter would have been in place for the full quarter. We believe we are well positioned for our earnings to benefit from further increases in short term market interest rates.

BDC Buzz

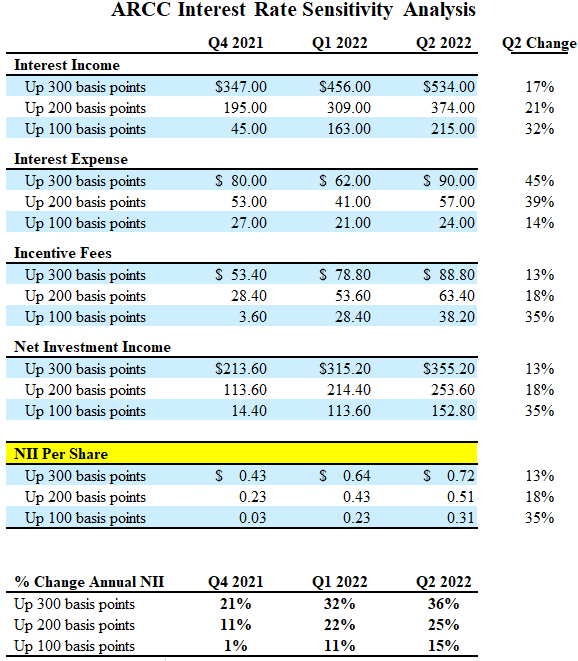

The following table shows the change from Q4 2021 to Q2 2022 with the impact from a 100 basis points increase changing from an additional $0.03 per share of annual earnings (as of December 31, 2021) to $0.31 per share (as of June 30, 2022).

“We don’t believe a tightening monetary cycle will have negative effects on us. Our large weight floating rate loan portfolio is financed by mostly fixed rate unsecured sources of financing and our assets are largely floating rate investments. We believe this positions us well to have our net interest earnings benefit from rising rates.”

BDC Buzz

Current Yields For Common Stock and Bonds

My previous best case projections for ARCC predicted an increase in the regular quarterly to $0.43 per share for Q3 2022 and I am expecting another dividend increase for Q4 2022 partially related to higher interest rates but also portfolio growth and/or additional income from Ivy Hill Asset Management (“IHAM”) partially due to the previously announced acquisition of the direct lending portfolio of Annaly Capital Management (NLY):

We just did a very large transaction there, obviously buying this portfolio from Annaly. They took on $1 billion plus of assets. We made a substantial investment in the company that’s a little bit of a needle mover for this quarter relative to others. In this quarter, we actually had a not necessarily expected one-time dividend from an equity investment in a portfolio company. But then the lion’s share of the increase as you can probably expect is our continued investment in Ivy Hill, that’s larger, it’s going to just be paying us a larger dividend going forward.

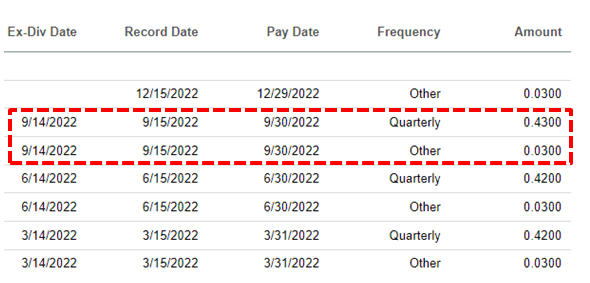

Previously, ARCC announced the $0.12 per share of “additional dividends” paid evenly each quarter for a total of $0.46 per share for Q3 2022:

Seeking Alpha

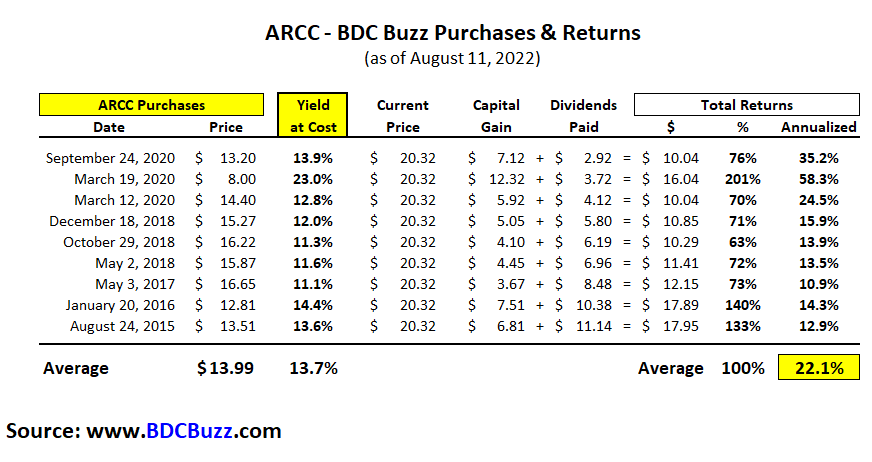

The “Annualized” return shown below shows the actual compounding of annual returns. This is the true return each year, which has averaged almost 22% over the last 9 purchases, even after taking into account the recent market pullback.

BDC Buzz

ARCC’s bonds due 2026 through 2031 (4 to 9 years) were trading around 20% below par but have started to rebound. For example, its 2031 bond was trading below 73 on June 30, 2022, and is now almost 80 but still yielding over 6%. It is important to note that is almost a 10% gain (from 73 to 80) just over the last 6 weeks and you are still getting a yield-to-maturity of over 6% for new purchases:

FINRA

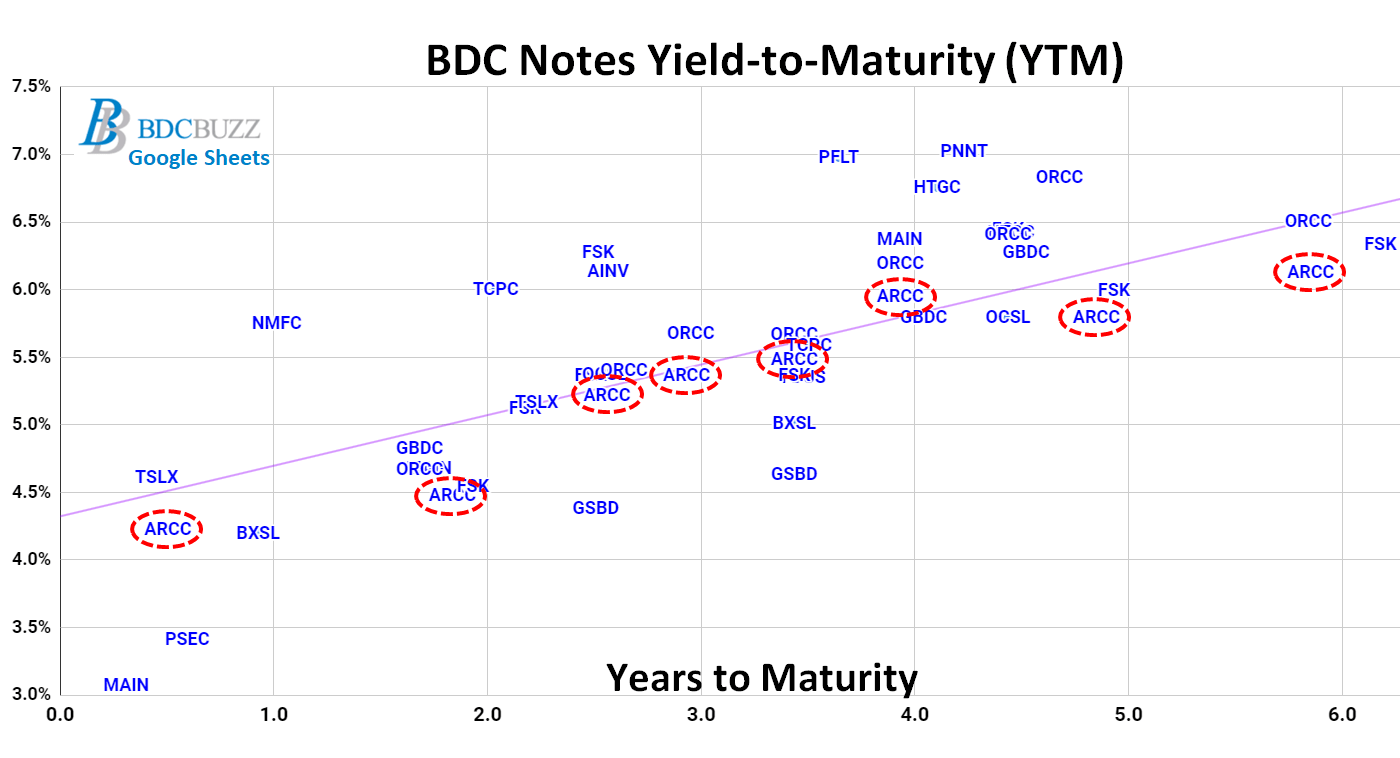

The following chart is from the BDC Google Sheets showing ARCC’s bonds and I will continue to cover many other BDCs listed below, including their asset and interest expense coverage ratios.

It is interesting to note that many of ARCC’s bonds are currently at relatively lower yields for similar maturities but likely related to being higher quality and higher trading volumes/liquidity.

BDC Google Sheets

Conclusion – Risk-Adjusted Returns

Given the uncertainty of upcoming returns from equity/stock positions, I would suggest that investors take this opportunity to lock in 6% returns provided by investment grade notes. ARCC is a higher quality company and investors can use a ‘barbell approach’ by investing a portion in the common stock as well as the investment grade bonds.

The key risk to the bondholder is a default by ARCC, which is extremely remote given the company’s history/performance:

- ARCC is one of the best-of-breed BDCs with a long track record of returns through previous market cycles

- Asset coverage of debt is 183% and by regulation must be at least 150%

- Interest expense coverage has averaged around 3.4 times, which is much higher than most companies

- ARCC’s bonds are rated investment grade by S&P, Moody’s, and Fitch

- No publicly traded BDC has ever filed for bankruptcy and impaired debt holders in the history of the sector

- ARCC’s stock is currently yielding 9% compared to its bonds around 6% for an average of 7.5%

Be the first to comment