Spencer Platt

While the trading frenzies of 2021 are far behind us, I think the early market bounce in 2023 is an especially favorable tailwind for Robinhood (NASDAQ:HOOD), the trading app that has caught younger investors by storm. Deeply hurt by the market’s fracture last year, Robinhood has slumped from the decline in risk-taking, particularly from waning interest in cryptocurrencies. As we look ahead to 2023 with fresh eyes, however, I think this millennial-oriented brokerage is poised to win.

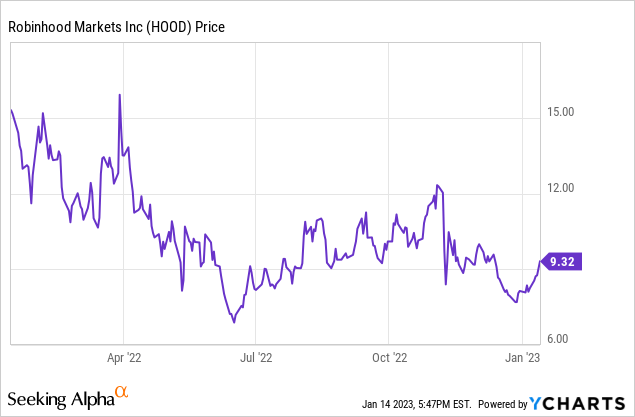

Down more than 35% over the past twelve months, Robinhood has surged a sharp ~15% since the start of 2023 – yet I think this rebound rally is just beginning.

A number of bullish drivers for Robinhood

There are a number of reasons to be bullish on Robinhood right now. Obviously, the so-far short-lived recovery in markets has buoyed investor confidence and re-sparked an interest in trading. As reported by the Wall Street Journal, interest in options (options market-making is one of Robinhood’s most lucrative revenue streams) has surged on account of high interest rates, with more investors in particular selling puts in order to invest the premiums in high-yield instruments. Higher interest rates, in fact, are also helping Robinhood to boost its net interest income as its spread on lending and client balances increases.

And from a product perspective, Robinhood just rolled out retirement accounts. While Robinhood’s primarily younger demographic is unlikely to bring in high average retirement balances, opening up this account type positions Robinhood well for deposit growth in the future as it continues to take clients away from traditional brokerages.

I remain bullish on Robinhood and am holding the stock confidently in my portfolio. Here is my full long-term bullish thesis on the name:

- Robinhood is dominating in the millennial/Gen Z demographics that will soon overtake the bulk of worldwide wealth. Traditional brokerages are still catching up to Robinhood’s popularity. Market cycles have always occurred and will continue to occur; there will be periods of frenzied trading and there will be periods of calm. But over the arc of time, Robinhood’s share of market activity will grow.

- Product innovation never stops. Part of what makes Robinhood so appealing is that it’s often first-to-market (or at least, first to popularize) many new key features. Crypto trading, cash advances, and easy access to low-cost margin were some of Robinhood’s key defining advantages. Retirement accounts will help to attract an even wider pool of assets to Robinhood.

- Diversified revenue streams. When interest rates were low and cash was cheap, Robinhood benefited from buoyant market activity. But now, as interest rates have shot up and put a chill over trading volumes, Robinhood is benefiting from higher interest spreads. Put in other words, Robinhood has now navigated through recessionary cycle and has proven itself capable of sustaining.

- Profitability in mind: When trading volumes were high in 2021, Robinhood generated positive adjusted EBITDA every quarter. Amid the current trading crunch, the company is making targeted structural adjustments to its workforce to enable it to maintain profitability going forward. While the down cycle in the markets won’t last forever, the belt-tightening and operational discipline that Robinhood is exercising now will certainly sustain.

The bottom line here: buy into Robinhood before the market fully catches wind of the uptick.

Recent trends show sequential improvement

Unfortunately it will be awhile until we see Robinhood’s Q1 results and the impact of the January rebound on its financials, but even going back to Q3 (September quarter) we can see signs of life in Robinhood’s trading activity.

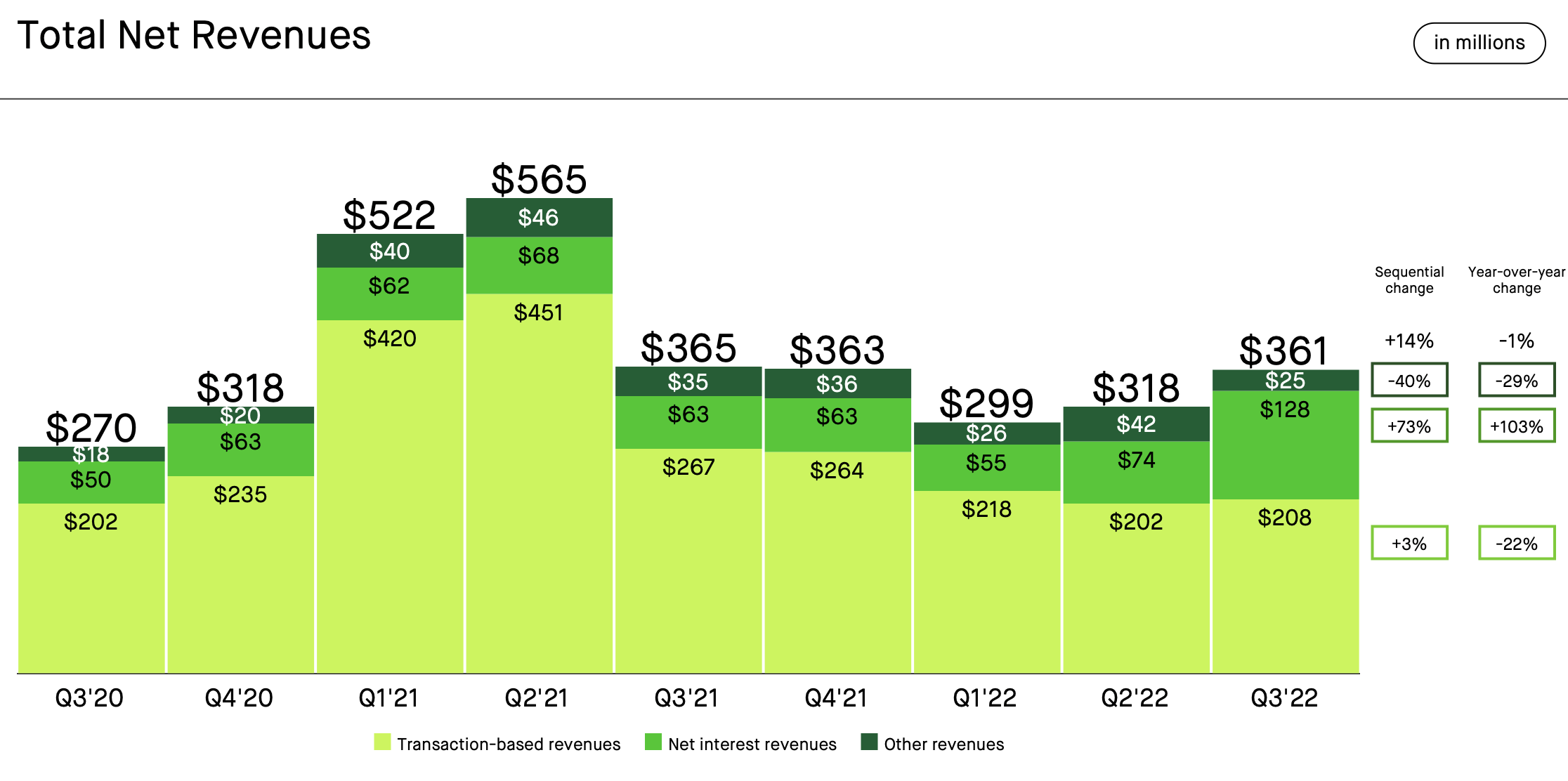

Robinhood’s total revenue in Q3 grew 14% y/y sequentially to $361 million and was roughly flat to last year. We can see that in spite of transaction volume weakness, what has helped Robinhood stay afloat is a ~2x y/y increase in net interest revenues.

Robinhood revenue trends (Robinhood Q3 earnings deck)

The table below breaks down how Robinhood generates net interest income. We can see that alongside a boost in margin interest, Robinhood is now also generating significant investments on its held cash and deposits, versus virtually nothing in last year’s low-rate environment:

Robinhood net interest revenue (Robinhood Q3 earnings deck)

Per CFO Jason Warnick’s remarks on the Q3 earnings call, the company continues to expect net interest revenue to grow in Q4:

Looking ahead to Q4, we’re encouraged by what looks likely to be another quarter of net interest revenue growth. As we consider what we see today for the forward Fed curve, customer balances and deposit rates, as well as a decrease in our margin book and securities lending so far in the quarter, we anticipate Q4 net interest revenues will be up by roughly $25 million from Q3. We could certainly come in higher or lower than that level, so we’ll have to see how Q4 plays out.”

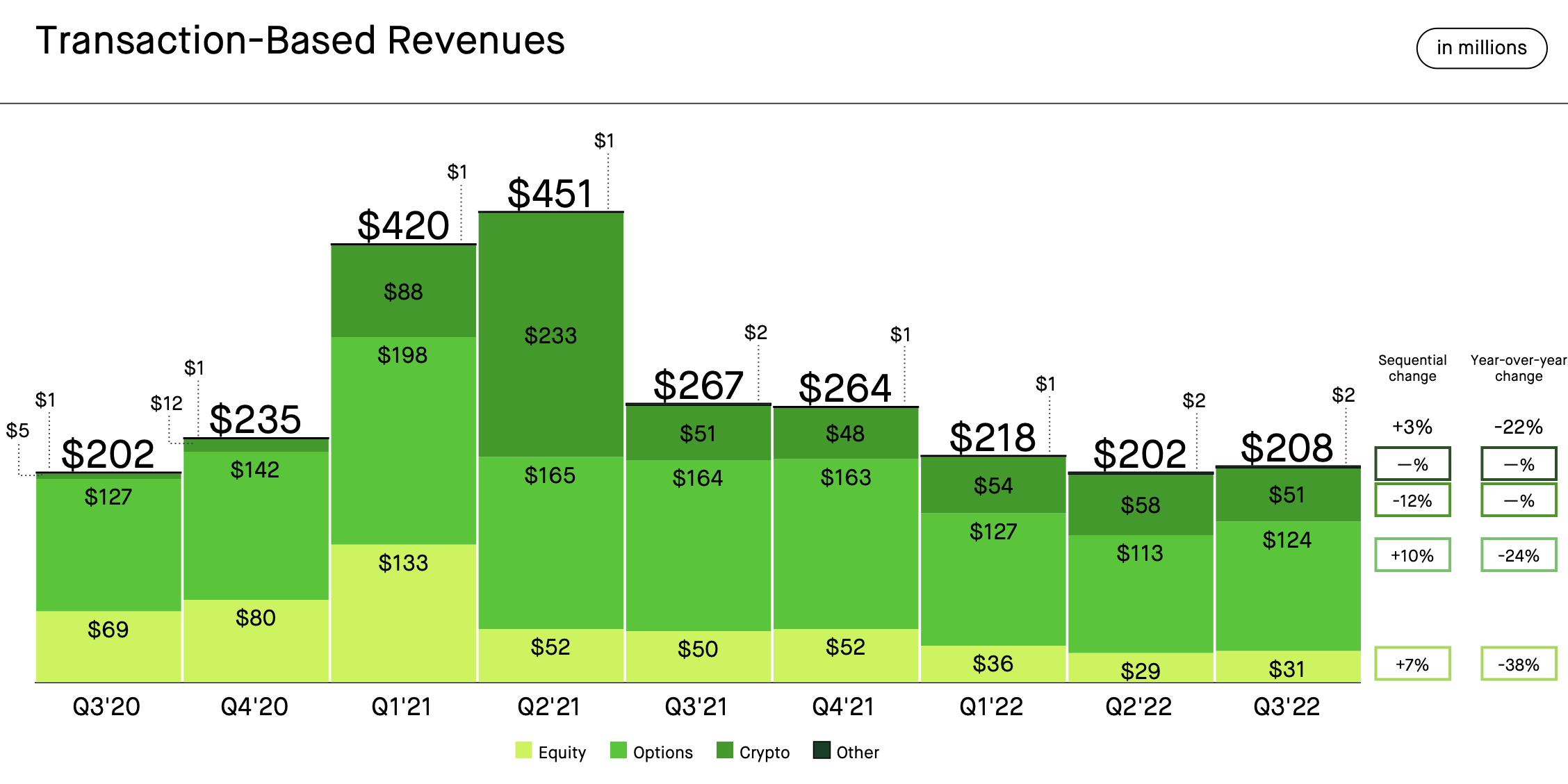

On the transactional side, meanwhile, while equity trading revenue remains quite low, we can see a 10% sequential (and 24% y/y) boost in Robinhood’s crypto trading income, which represents more than half of Robinhood’s transactional revenue. We expect equity trading revenue and volumes to be up corresponding to the market recovery in Q1 (provided that sustains).

Robinhood transactional revenue (Robinhood Q3 earnings deck)

The company also increased its total funded accounts by 60k in the quarter, ending the quarter at 22.9 million accounts. The company has also reported strong 17% y/y growth in deposits, driven in part by the relatively high interest rates (currently at 4%) that Robinhood is offering to its Gold customers. Management also noted that customer churn remains low.

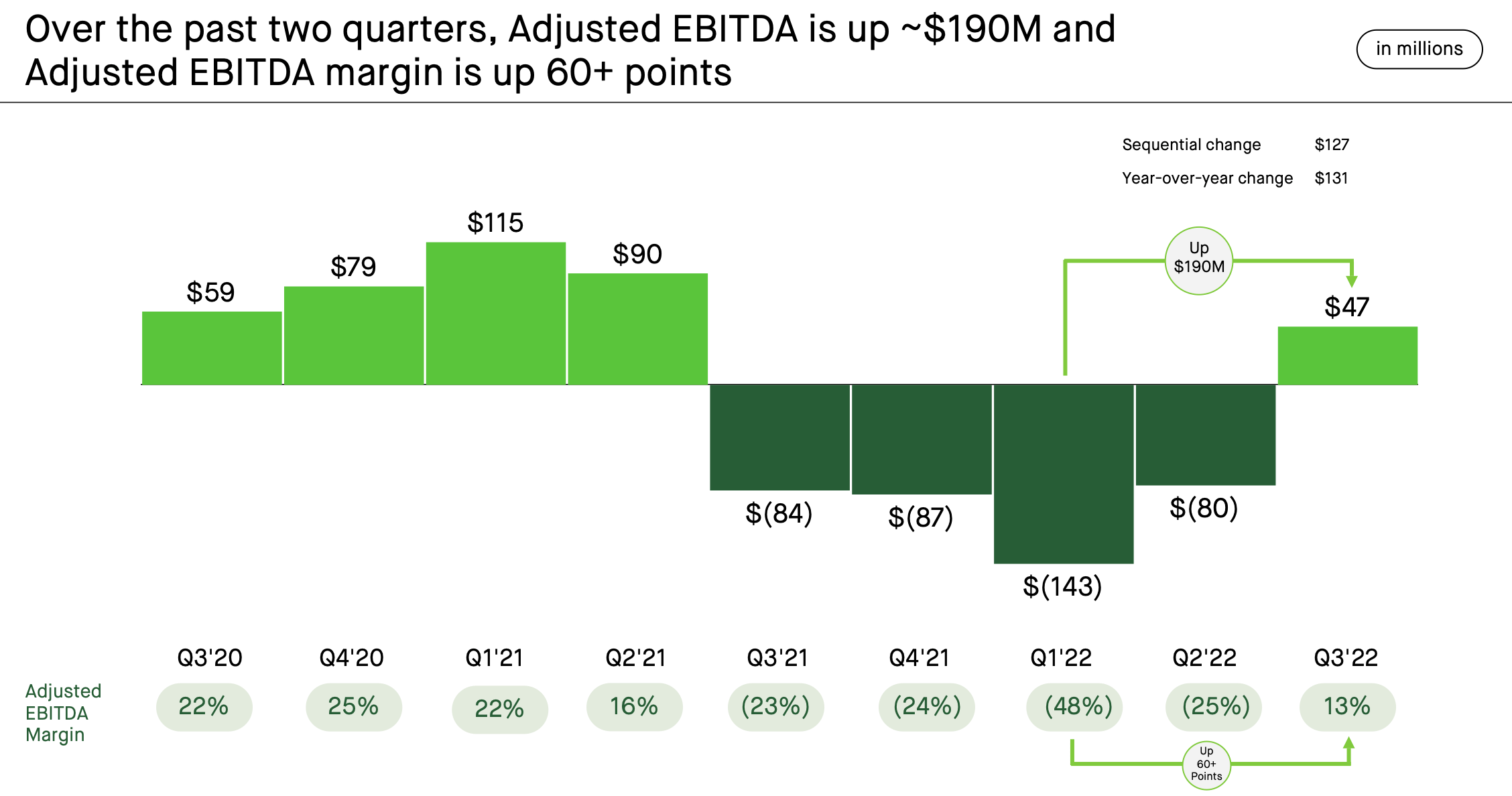

Robinhood also achieved positive adjusted EBITDA margins of 13% in Q3, one quarter ahead of its target to hit breakeven by Q4. This is a testament to Robinhood’s aggressive cost-cutting and layoffs, helping the company achieve margin levels on par to the height of market activity in the first half of 2021.

Robinhood adjusted EBITDA (Robinhood Q3 earnings deck)

In my view, the company’s now-healthy bottom line will be a source of comfort to investors in the currently risk-averse market.

Risks and key takeaways

A healthy market rebound so far in January, plus higher interest rates feeding a jump in net interest income, should help Robinhood to recover from its 2022 doldrums. And with the company’s opex base reduced thanks to its cost-cutting measures in 2022, Robinhood looks set to drive a re-acceleration in growth and scale toward meaningful profitability.

There are risks, of course. The first is crypto, which is Robinhood’s largest revenue stream (thanks to the spread that Robinhood earns on facilitating these trades). Though prices are rebounding, the general hype over crypto trading has died down after so many investors got burned in the 2022 crash – which may mean muted trading volumes are here to stay. The second is headline risk, as Robinhood’s payment for order flow (PFOF) business model has always attracted a lightning rod of criticism (though certainly not enough to keep the company from adding new accounts and building up its deposit streams).

This being said, I think Robinhood’s tailwinds plus the current low entry point more than make up for these potential pitfalls. Stay long here.

Be the first to comment