Mohammed Haneefa Nizamudeen

Seagen (NASDAQ:SGEN) is a Seattle-area based pharmaceutical company with a growing portfolio of cancer therapies. In 2022 the stock price was driven up by talk of a possible buyout by Merck (see Seagen with and without a Merck Buyout), but that hope faded, and the stock price with it. Here I will briefly review Q3 2022 results, noting that Q4 2022 results will be released on February 15. I will focus on recent approvals and the rest of the therapy pipeline, as they seem to be holding up the stock price. Seagen continues to lose money, and though that is mainly due to reinvestment in R&D, it still should be cause for a reasonable degree of caution.

Q3 2022 Seagen Results

Seagen Q3 2022 results were reported on October 27, 2022. Revenue was up 20% y/y to $510 million. Despite that, GAAP net loss was $191 million or $1.03 per share. Expenses were dominated by R&D spending of $384 million. While technically an expense, that could be considered reinvestment. In theory Seagen could become profitable simply by cutting R&D, but of course that would not be the best strategy for the long run. Cash and equivalents ended at $1.76 billion, with no debt, so negative cash flow can go on for a while longer without the need to issue more stock.

|

Seagen Revenues by product ($ millions): |

||||

|

Q3 2022 |

Q2 2022 |

Q3 2021 |

y/y increase |

|

|

Adcetris |

$219 |

$202 |

$185 |

18% |

|

royalties |

44 |

39 |

41 |

7% |

|

Padcev |

105 |

124 |

95 |

11% |

|

Tukysa |

88 |

89 |

87 |

1% |

|

Tivdak |

16 |

17 |

0 |

na |

|

Collaboration |

38 |

27 |

17 |

131% |

Source: SGEN Q2 and Q3 2022 results releases, data arrangement by author

Looking at revenue, Adcetris continues to lead growth. It should continue to grow until it loses patent protection, as the label is still being expanded to new indications. Unless better therapies are approved for its indications and then reduce its market share. Padcev is making good progress and in April 2022 was approved in the EU as a monotherapy for advanced or metastatic urothelial cancer patients who have previously received a platinum-containing chemotherapy and a PD-1/L1 inhibitor. Tukysa has paused growth, but I will discuss a new development in the next section. Tivdak is the latest commercial therapy, approved for cervical cancer.

Tukysa approved for HER2+ colorectal cancer

On January 19, 2023 Seagen announced the FDA approved Tukysa for colorectal cancer. More specifically, Tukysa in combination with trastuzumab (Herceptin) was given accelerated approval in patients with previously treated RAS wild-type, HER2-positive metastatic colorectal cancer. The accelerated approval was based on Phase 2 trial data. Because it is an accelerated approval a confirmatory trial may be required for full approval. This could be a particularly valuable indication since it is the first FDA approval for HER2+ metastatic colorectal cancer. Patients who had this type of cancer generally have poor outcomes if they progress after their frontline chemotherapy. Biomarker testing can show which patients have HER2+ cancers. Still, there is room for improvement. The trial resulted in an 38% overall response rate, but only a 3.6% complete response rate.

Padcev BLA for urothelial cancer accepted by FDA

In partnership with Astellas (TSE:4503) and Merck (MRK), on December 20, 2022 Seagen announced the FDA had accepted a supplemental BLA for Padcev for first-line metastatic urothelial cancer, when patients are not eligible for cisplatin chemotherapy. This is when dosed in combination with Keytruda, Merck’s PD-1 immunotherapy agent. If approved this would expand the labels for both Padcev and Keytruda. The PDUFA decision date was set to April 21, 2023. Urothelial cancer is the most common type of bladder cancer and, once it reaches an advanced stage, typically has poor outcomes. About half of advanced urothelial cancer patients in the U.S. are ineligible for cisplatin chemotherapy. The combination is continuing to be tested in a Phase 3 confirmatory study. Two additional Phase 3 trials are being conducted with the combination in muscle-invasive bladder cancer.

Adcetris Phase 2 Hodgkin Lymphoma data positive

On December 12, 2022, Seagen announced positive Phase 2 Adcetris data for Hodgkin Lymphoma. The trial tested Adcetris in combination with chemotherapy and Bristol Myers’ (BMY) Opdivo PL-1 therapy for both early and advanced classical Hodgkin Lymphoma. For the advanced lymphoma there was a remarkable 88% complete response rate, with 95% of patients showing progression free survival at 12 months. For the early-stage lymphoma the complete response rate was a bit lower at 92%, while progression free survival was not yet available. The trial is ongoing.

Adcetris is an ADC (antibody-drug conjugate) directed at CD30, a cell membrane protein that is overexpressed by some cancers. It is already approved for adults with previously untreated stage 3 or 4 classic Hodgkin Lymphoma and several other lymphomas. It is jointly developed with Takeda. It is undergoing additional label-expansion trials in PTCL (peripheral T-cell lymphoma), relapsing/remitting Hodgkin Lymphoma, and in solid tumors.

Rest of Pipeline

The Seagen pipeline is dominated by label extension studies for the currently approved products. Other products in Phase 2 clinical trials are disitamab vedotin and ladiratuzumab vedotin. I count 8 agents that are in Phase 1 trials. Given that going from Phase 1 trial to FDA approval is a multi-year process, it would appear Seagen has new approvals potentially lined up for the rest of the decade. Its ADC platform has been very successful, so I also expect Seagen to move candidates from preclinical to clinical trials on a regular basis.

Analysis and Conclusion

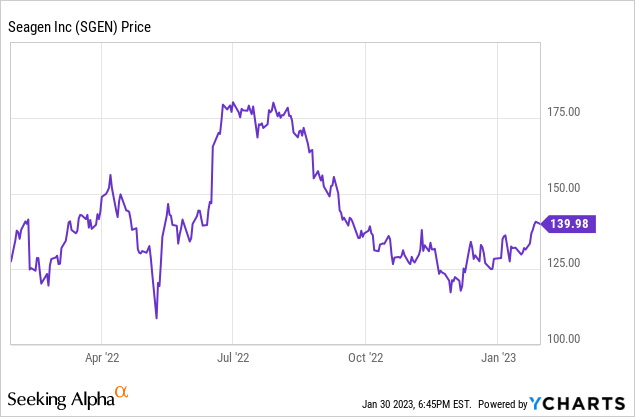

I characterize Seagen as reasonably priced, given its revenue, net income trends, and pipeline. Currently the stock price, $139.98 at the close on January 30, 2023, is about in the middle of its 52-week range, between the low of $105.43 and the high of $183.00. Its market capitalization is around $26 billion. To justify a $26 billion market cap, if you want even just a 5% earnings return, you would need annual earnings of $1.3 billion. Clearly, Seagen has some work ahead to get to that minimal standard. On the other hand, it has a platform that can create new product candidates and has shown it can get some through the clinical process and into commercial sales. So currently much of the stock value is in the pipeline and in the newly introduced therapies that, hopefully, have a significant ramp ahead. I believe that can be attractive to long-term investors, as long as they realize the potential downsides of valuing a pipeline before it has produced profits.

With product revenue now running at an annual rate of over $2 billion, and likely to ramp more quickly as the pipeline ripens, my assessment may be being conservative. If Q3 2023 revenue increases by another 20% and expenses are kept level, net loss would be about $90 million. Another year at that pace of growth could result in cash-flow break even some time in 2024. If I am right, that means current cash should last until that point. Still, much future success is assumed in the current price and market capitalization.

Be the first to comment