ipopba/iStock via Getty Images

In the high-growth selloff that has accelerated over the last six months, there have been few businesses that have been ravaged quite as severely as Sea Limited (NYSE:SE).

Sea declined from a high of over $370 in October last year to a current price of $110, losing 70% of its value from all-time highs, and was down nearly 80% at recent lows.

This decline is far more than other emerging market e-commerce and fintech peers such as MercadoLibre, Inc. (MELI), which is only down 50% from recent highs. While there are concerns around the Sea investment case, there is still quite a lot going well for the business.

Leadership in Southeast Asian Markets Continues

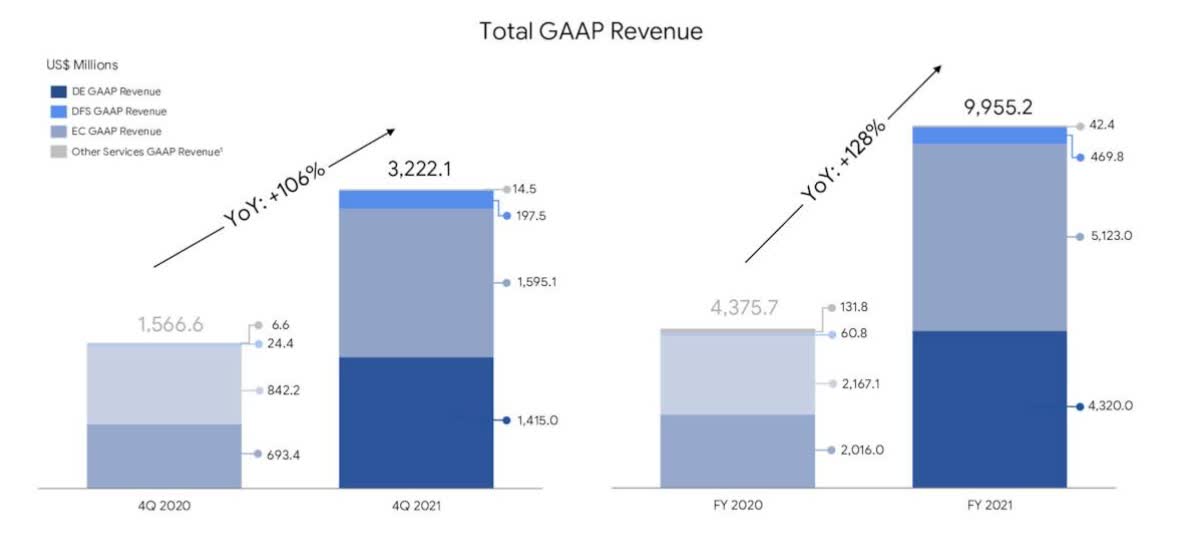

Sea Limited continues to post impressive top-line numbers, and market leadership remains strong in key markets across Southeast Asia. The business recently announced revenue growth of 106% year over year, with the businesses e-commerce and fintech segments, in particular, doing very well.

SE Q4’21 Earnings

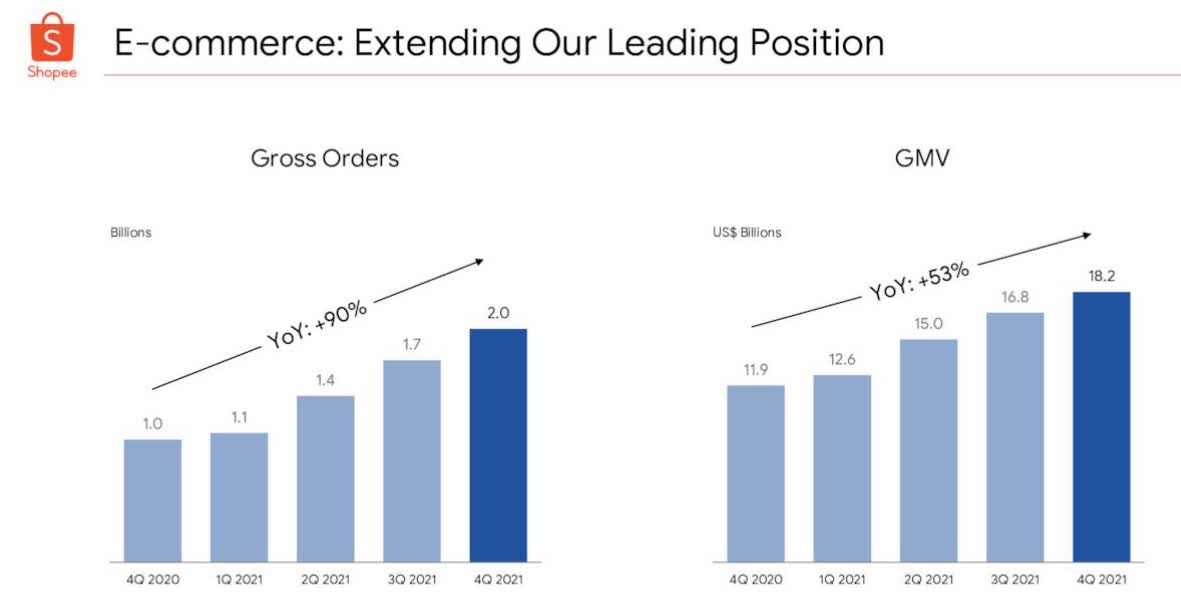

While Garena revenues from Sea’s Free Fire franchise continue to prop up the business, Sea’s e-commerce platform Shopee is driving much of the recent growth that Sea has seen. Shopee is seeing a solid expansion of order volume and gross merchandise volume expansion. Order volume grew 90% year over year, with gross merchandise increasing 50% yearly.

SE Q4’21 Earnings Report

Beyond just revenue growth, Shopee continues to deliver market leadership in key markets in Southeast Asia. Sea highlighted in its most recent earnings call that the business continues to dominate App Store Rankings across each of its South East Asian markets. Sea’s metrics in both average Monthly Active Users and time spent in-app continue to dominate competitors.

The business remains the e-commerce market leader in markets including Taiwan, Malaysia, Philippines and Singapore. Sea has even pulled ahead in Indonesia, after a close battle with Tokopedia in this market. Sea maintains dominant numbers in critical metrics such as user engagement and transaction frequency, both keys to cementing a network effect and keeping merchants interested in the Shopee platform.

Shopee users transact on the platform nearly 6x a month, a rate that has been steadily increasing over the last few years, with engagement and time on the platform also higher than its competitors in the region. Users spend nearly 30 minutes per day on its app across its markets.

Profitability Looks Close At Hand

It’s no secret that Sea has been aggressively subsidizing both merchandise pricing on the platform and shipping costs through a combination of low merchant commissions and user promotions.

This market investment has resulted in relatively low take rates and heavy shipping subsidies, which mask the business’s actual cost of service delivery. The strategy here makes sense. Building initial market share should be a pathway to repeat user visits to the platform.

Once a user establishes Shopee as their preferred platform, SE can slowly withdraw the level of the subsidy and increase its take rate. It also creates the pathway for additional service monetization. Sea is driving the Shopee e-commerce business to achieve operating profit throughout Southeast Asia and Taiwan by year-end.

Profitability appears to be a realistic outcome. Sea will likely benefit from increasing order frequency and reduced promotions and incentives with time.

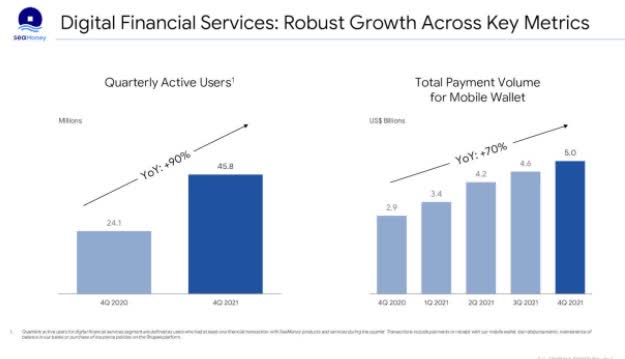

Sea Money Is Starting To Scale

Sea Money is turning into a bright spot for Sea. The business grew revenue in this segment more than 8X year-over-year to deliver $195M. Quarterly users increased 90% to 46M, while mobile wallet payment volume reached $5B, up 70% year over year.

SE Q4’21 Earnings Deck

Sea Money is at an inflection point. The business forecasts revenue growth of 155%, which will deliver ~$1.1B in revenue in 2022. Sea’s strong user base has attracted the attention of large merchants such as 7-11 and Subway, who are now accepting Sea Money in-store in several markets.

The business has capitalized on the successful platform traction of Sea Money to extend the value proposition for in-store point of sale payments. I expect more product innovation to come with Sea Money. Sea now has banking licenses in Singapore and Indonesia which should mean additional future use cases that SE can deliver.

The economics of Sea Money should be highly favorable to Sea. Through targeted promotions, user acquisition is very efficient to acquire users via Sea’s existing platforms.

Sea management expects the business to be cash flow break-even in 2023. While Sea’s progress has been positive in certain areas, SE has received some knocks that have raised questions about the investment case.

Sea’s Cash Cow Is Facing Setbacks

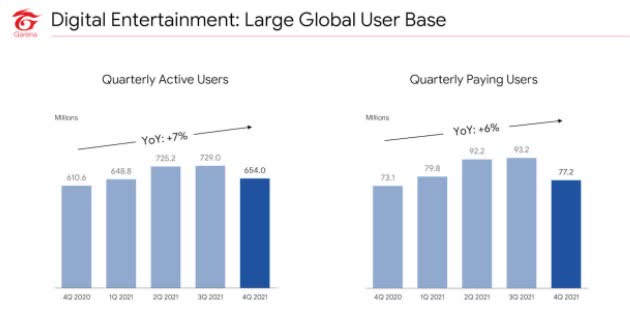

The biggest knock on the Sea investment case is the dramatic slowdown in Garena quarterly active users, which declined 10% quarter over quarter. Quarterly paying users were also down nearly 17%.

SE Q4’21 Earnings Report

The reasons for the decline need to be put into context. Sea’s Free Fire franchise was released in 2017 and became the most downloaded mobile game globally by 2019.

After several years of strong user growth, it is natural that new users would peak, and user growth would start to level off. Still, Sea is looking at ways to extend Free Fire’s engagement with innovative off-line campaigns to build user engagement and extend Free Fire’s utility.

However, the Free Fire declines more specifically hurt Sea because Sea has successfully used the heavy profitability from the Free Fire gaming franchise to drive Shopee penetration in existing markets and help SE expand into new markets.

The profits of the Garena business help enable the subsidization of promotional discounts for new users and aggressive discounts on shipping that Sea also provides its customers. With the Garena user declines, there are questions now as to what extent Sea will be able to continue with such expansion.

SE Q4’21 Earnings Report

Garena’s slowdown will also hit SE’s near term revenue. While Shopee and Sea Money will record strong revenue growth in ’22, Garena will actually see a decline in revenue based on SE’s forecast, which will slow overall group revenue to consensus growth of just 35%, from over 100% in 2021.

Sea Is Pulling Back From Global Expansion

Sea aggressively expanded into new markets over the last couple of years. These new markets have included Brazil and Mexico in Latin America and a host of other markets in Asia and Europe, notably India, France, and Spain.

This aggressive expansion raised many eyebrows and questions that Sea may have expanded too quickly, particularly in markets where it didn’t appear to have any unique value proposition or sustainable competitive advantage.

There were fears that dynamics it had successfully exploited in Southeast Asia, with diverse product selection, low prices, and gamification of the user experience, may not win the day in some of these new markets.

With the Garena cash cow experiencing some issues, Sea has increasingly had to make hard choices concerning capital allocation. India has been a recent casualty here, although Sea may have partially had its hand forced due to a ban imposed on Free Fire by the Indian government.

The reasons for SE’s Free Fire ban in India have been opaque, though the involvement of Tencent on SE’s share registry is suspected. Similarly, Sea also announced its recent exit from France, another market it had entered within the last six months. Sea’s exit from these markets may appear to blow long-term global growth ambitions.

I take a contrary view: both markets were not ones where I believe there was a clear advantage and a long-term path to profitability for Sea, in the way that core markets in Southeast Asia or even Latin America may offer. Sea still has a market presence in several other global markets, such as Poland and Spain, which offer avenues for expansion, and its SE Asia markets still offer the potential for significant, long term growth.

Being forced to be more disciplined with capital and quickly exiting non-performing markets should enhance Sea’s path to profitability and ultimately help the business achieve this objective faster.

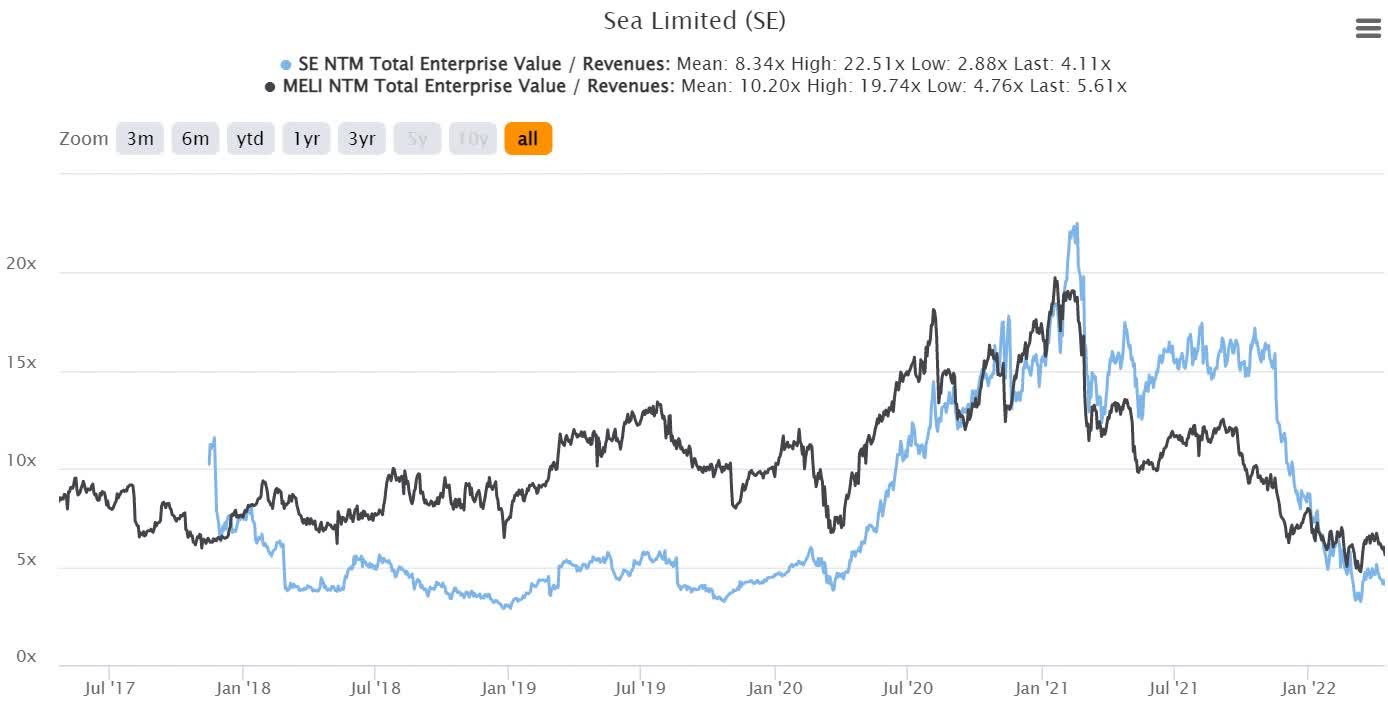

Thoughts On Relative Valuation

Through much of 2021, Sea displayed a massive valuation premium to other emerging market peers, particularly MercadoLibre. This premium made little sense because MercadoLibre has a much higher take rate and better profitability than Sea.

MELI also has a proven and sustainable model for growth and market leadership that has been battle-tested in key markets such as Brazil and Mexico against global giants such as Amazon and Alibaba, for much of the last decade. I found it curious that the market thought to award Sea with such a high premium.

SE 04’21 Earnings Report

Nevertheless, this premium has now fizzled out, such that Sea trades at a more appropriate discount on valuation relative to MercadoLibre. This discount is fair in light of Sea’s recent stumbles, yet Sea is still underpriced relative to the business’s historical valuation and improved market leadership in key markets.

Concluding Thoughts

While MercadoLibre is my preferred emerging market e-commerce and fintech platform, Sea represents a still worthy yet slightly higher risk option for Southeast Asian commerce and digital financial services. The risk of the investment case has undoubtedly risen over the last couple of months.

Yet, core engagement and market leadership suggest that Sea continues to execute well and is on a path to market dominance in SE Asia. Valuation also remains more compelling than any time over the last 18 months.

Be the first to comment