Editor’s note: Seeking Alpha is proud to welcome Samuel McColgan as a new contributor. It’s easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Side view of dry bulk carriers cargo ship in the sea Miro Nenchev

The fortunes of dry bulk companies are strongly associated with the supply/demand dynamic. While supply is low, demand is currently lower and prices are falling. Supply changes slowly due to long-lived assets with lengthy lead times, yet demand fluctuates much faster. Demand will likely improve before supply, and when it does, prices will rise and dry bulk will prosper.

Safe Bulkers (NYSE:SB) is very well-positioned to perform in the coming years. It is prepared better than most for incoming environmental regulation changes with a young and efficient fleet. Additionally, management prioritizes shareholders and the stock is very cheap.

Supply low, demand choppy

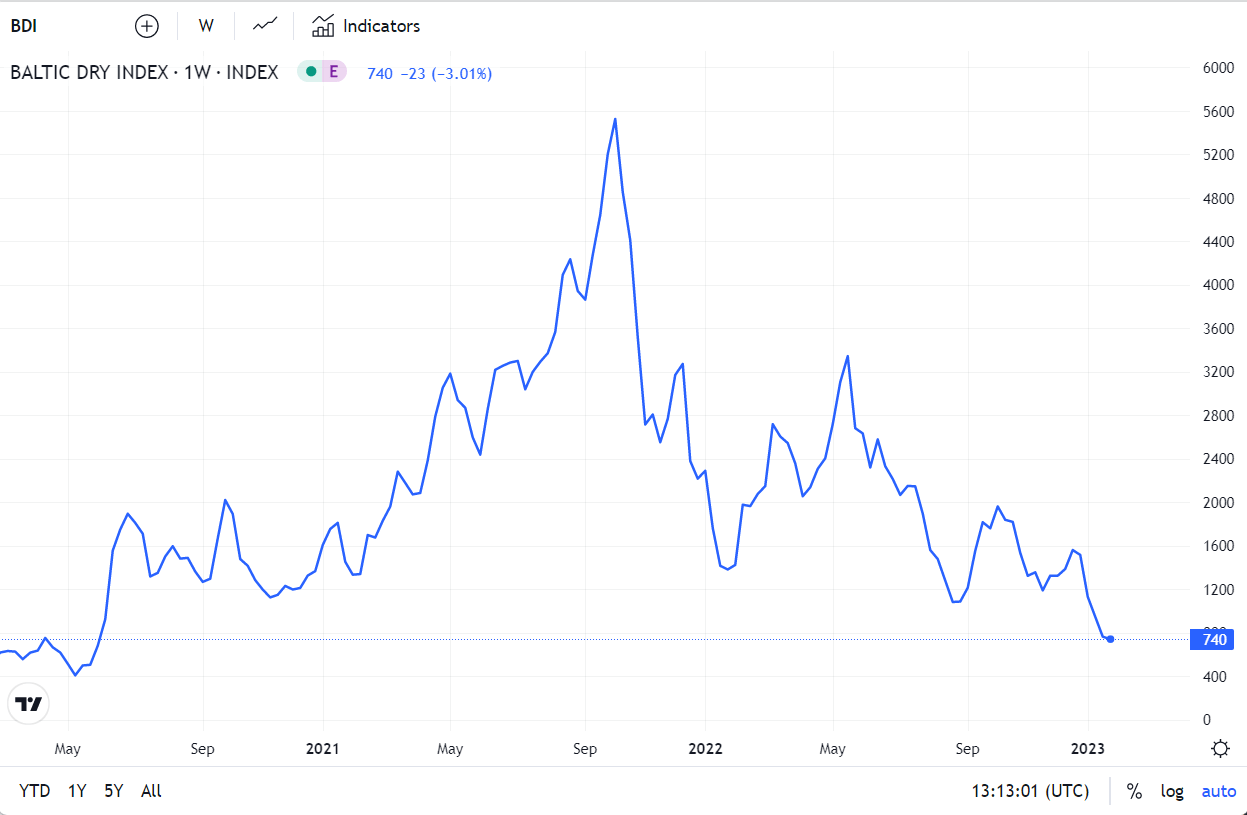

Dry bulk is heavily influenced by supply and demand, both of which are currently suppressed. The Baltic Dry Index, shown below, provides a benchmark of dry bulk prices that are at five-year lows, implying supply is stronger than demand.

Baltic dry index (Trading Economics)

Many people avoid investing in a commodity market when prices are downward trending and at lows. However, I believe this will create opportunities to pick up cheap stocks (especially after the next round or two of earnings calls) in dry bulk before the industry shifts once again toward prosperity.

My assumption that the industry will get better before it gets much worse depends predominantly on the fact that supply will be fixed for the next few years, but demand will rise in due course. I’ll explore both of these factors below.

Demand

As is generally the way in a recession, global demand for dry bulk is down. Not only is global demand down, but the biggest dry bulk consumer’s demand is way down. China accounts for one-third of the world’s dry bulk imports. Its demand remains low, with the effects of zero-COVID policies and lockdowns still being felt. Its economic recovery is slow so far, and its construction and real estate industry will take more time to bounce back.

That said, there are a few factors compensating a little right now, increasing demand. Container shipping delays have been up substantially, and so commodities such as rice and sugar have been increasingly transported via dry bulk instead for faster shipping times. Furthermore, geopolitical tensions cause countries to make decisions that are not economically efficient. For example, the Russia-Ukraine war triggered unexpected demand. Instead of Russian oil, Europe began importing plenty of coal from far afield.

In any case, all these factors are highly uncertain and could go one way or another. You will need to draw your conclusions on timeframes, and expect to be off by some margin. Dry bulk markets can be hard to predict. However, I believe we’ll see demand pick up in 2023 or 2024 as China slowly ramps up demand, and as recession fears or reality pass.

Supply is down, and will stay that way

Supply results from a combination of global capacity (the number and sizes of vessels), and the speed at which vessels deliver goods. Both factors are experiencing downward pressure, reducing overall supply.

Regarding capacity, the shipbuilders’ order book is a good indicator of how this volume will change over time. A large order book implies supply will increase, crowding the market and bringing down rates. The dry bulk sector’s order book is at historic lows. Only a 2.1% fleet size increase is expected in 2023, and a 1.8% increase in 2024. As we enter a period of high inflation and supply chain challenges, I doubt the order book volume will increase materially. Even if it does, ship lead times have increased from around two to over three years now, so the overall volume of operational ships will remain near current low levels for some time.

In addition, environmental regulations from the International Maritime Organization came into effect in January 2023 (specifically EEXI/EEDI). These regulations will reduce supply in two ways. First, they will reduce fleet transport speed, meaning fewer journeys and a diminished overall supply. Less supply leads to increased shipping rates. As a side note, companies will benefit from reduced fuel spending on each journey. Second, regulations strongly incentivize carriers to regularly scrap inefficient, older vessels. Since these take a long time to replace, supply will drop.

A competitive fleet

The dry bulk market is sensitive to price and so it is difficult for carriers to distinguish themselves based on quality or value-added. Economic moats like brands, switching costs and network effects don’t hold. Still, Safe Bulkers has some of the best margins in the sector, including top and bottom lines, which suggests some kind of competitive edge.

Margin comparison between SB and its peers (SeekingAlpha)

SB believes its advantage lies in its young and efficient fleet and is investing to improve the performance and longevity of its assets. A higher capex for fleet upgrades in the past two years made sense since margins were high. I’ll outline three focus areas for these upgrades (see a recent company presentation for more details) and why I believe they will be effective.

First, the company has been procuring new vessels in the highest category of efficiency. These vessels consume around 25% less fuel. They already have five new builds operational, with five more incoming next year. With 25% of the fleet achieving around 25% fuel savings, a total fuel saving of around 6% is expected. SB began ordering these vessels back in 2020, long before the competition. Ordering early and before supply chain issues secured lower build prices of ~$30m, whereas these now cost ~$40m.

Second, they have been selling their oldest vessels and buying ones ~10 years younger for a reasonable additional price. Its average fleet age is now 10 years old. This was excellent foresight, as older vessels are disproportionately affected by the regulations since they consume more fuel, hence will need to further limit their speed and therefore generate less revenue. This also shields the company from having to scrap ships once environmental regulations tighten further.

Third, by the end of 2023, almost all of SB’s ships will have scrubbers installed which remove harmful exhaust gases. Scrubbers legally enable ships to run on a relatively cheap fuel with high sulphur content, dramatically reducing costs. The value of the fuel saving (known as Hi5 spread) varies significantly but is expected to average around $190+ per tonne of fuel through 2023, which is significant (though less than the crazily high figures through 2022).

Incentivized and effective management

The management at SB says they see the shareholders as partners, and I believe their actions support this. Management currently owns 25% of SB’s shares, so I believe incentives are aligned.

Until recently SB paid no dividend, but now pays a $0.05/share (currently an 8.1% yield). This is well below some of its peers. Company management has clearly stated they don’t intend to pay a large dividend as they are prioritizing reinvesting for long-term gain for shareholders. Since I prioritize capital appreciation, this smaller but likely sustainable dividend works for me.

Their ROIC began to spike during the summer of 2021 and has since remained at around 18%-20%. This demonstrates the management’s strength in reinvesting capital and justifies the smaller dividend. They also have deleveraged somewhat recently, and plan to continue to do so gradually. SB has also recently bought back 2.8m shares, with another 2.2m authorized. This incoming buyback will represent a further ~2% reduction of the outstanding stock.

Reasonably priced

SB’s share price is cheap by every measure:

- P/E is currently 1.9, compared to its five-year average of 6.9. The sector average is currently 4.4.

- EV/EBITDA is currently 3.4, compared to its five-year average of 10.1. The sector average is currently 5.

- Analyst estimates of fair value range from $9 to $12.

Taking the metrics together, I believe undervaluation comfortably exceeds 50%. Overall, I believe sentiment in the dry bulk sector is very negative due to uncertainty surrounding 2023’s demand. However, while next year’s demand could go many ways, supply will remain. The low multiples of SB, or dry bulk carriers more generally, simply do not reflect either their current profitable state or the long-term prospects of the companies themselves. It appears that SB has been especially hard hit because it is a small-cap company with debt. Once sentiment improves, the upside potential is very large.

Financial health

During 2020 and 2021, long-term debt was cut almost in half to $316m. However, recently it has risen to $411m. While I have some reservations about the size of the debt, the company can afford to pay upcoming liabilities and is making efforts to bring down leverage. Its scrap value of $390m, cash of $120m, credit allowance of $350m, and contracted revenues of $390m should provide enough cover to weather any but the most serious of storms.

The average interest rate of debt is low, at less than 3%. Unfortunately, only 20% of this is a fixed bond, while 80% is floating, so the interest rate is subject to rise. It is also worth noting that inflation poses less of a risk to margins, as rates and vessel valuations rise approximately on par with inflation. Additionally, on the positive side, debt decreases in relative size during inflation.

Summary

In conclusion, I believe that economics will favor dry bulk. Demand in the short term will be volatile. However, even if it falls in the short term, sooner or later demand will return to normal levels, and the dry bulk sector will benefit tremendously.

SB is well positioned in this sector, being highly profitable and having already made substantial investments in its fleet. This fleet will enjoy significant efficiencies and is poised to impressively handle incoming environmental regulations that will become increasingly stringent.

The leverage is my only concern, though the risk is small in my opinion. The company has excellent management and the share price is very low. Although the share price might fall over the next year, I rate SB as a buy at this price and am confident in its prospects in the medium to long term.

Be the first to comment