JHVEPhoto

2022 was a wild ride for shareholders of Ross Stores (NASDAQ:ROST). Shares bottomed in late June at $70 before staging an impressive rally. In the end, Ross shares finished up 2% for 2022, significantly outperforming the broader market (S&P 500 was down 17%).

Fundamentally, 2022 was a tough year for Ross with same store sales, operating profit, and EPS all declining versus a difficult set of 2021 comparables. Looking ahead to 2023, the future appears brighter as many headwinds appear set to dissipate.

However, at nearly 24x 2023e EPS and 20x my estimate of normalized EPS, Ross shares appear to be fully pricing in the anticipated improvement in results. As such, I’m staying on the sidelines for now. As I discuss below, I’d be interested in buying the stock if it were to fall back below $85 per share.

2022 Was a Difficult Year

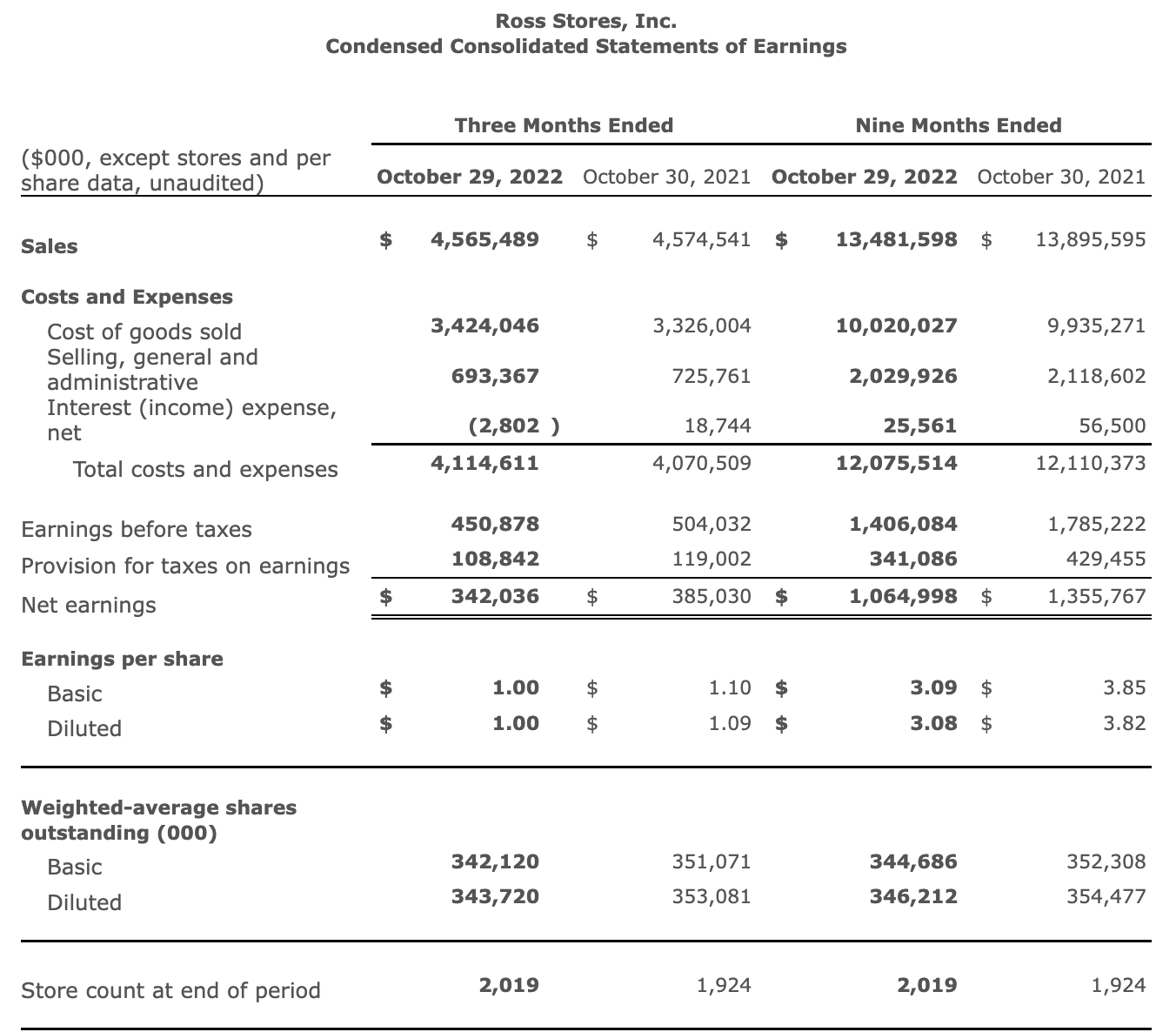

Ross Results 2022 vs. 2021 (Ross 3Q22 Quarterly Report)

As shown above, pretty much everything went in the wrong direction for Ross Stores in 2022. To be fair, the company was up against a very tough comp from 2021 when consumers were flush with cash following several rounds of pandemic-related government stimulus. Early in 2022, Ross suffered from limited merchandise availability due to supply chain constraints. Further, Ross customers were beset by the impact of inflationary pressure on household budgets. With customers spending more on food, rent, and gas there was simply less money left for discretionary purchases like apparel and household goods. With same-store sales down -7% in 2Q22 (and -3% in 3Q22) Ross underperformed off-price peer TJX Companies (TJX) which saw a -5% comp in 2Q22 (and -3% in 3Q22) owing to TJX’s more affluent customer base.

Beyond the top-line pressure, gross margins were compressed by higher international freight costs as well as a more promotional environment throughout retail as many retailers simply had too much inventory (had over-ordered expecting a stronger consumer spending environment). This was further compounded by inflationary pressure on operating expenses, most notably wages and utilities.

This combination of a difficult sales environment, shrinking gross margins and rising operating costs conspired to drive operating profit down -23% through the first 9 months of 2022.

Expected Improvement in 2023

Of the stock market is a forward looking machine – Ross shares rebounded after reporting 3Q numbers (which were better than feared) and guidance for improved same store sales in 4Q22 (expected 0-2% decline). Looking into 2023, investors take comfort from:

- A decline in inflation which should increase consumer confidence and spending on discretionary items. This also decreases upward pressure for Ross’s operating expenses (particularly labor).

- Broadly speaking, retailers are clearing their excess inventory position and should enter 2023 with more normalized inventory positions. This reduces the need for excessive discounts and should lead to a rebound in gross margins.

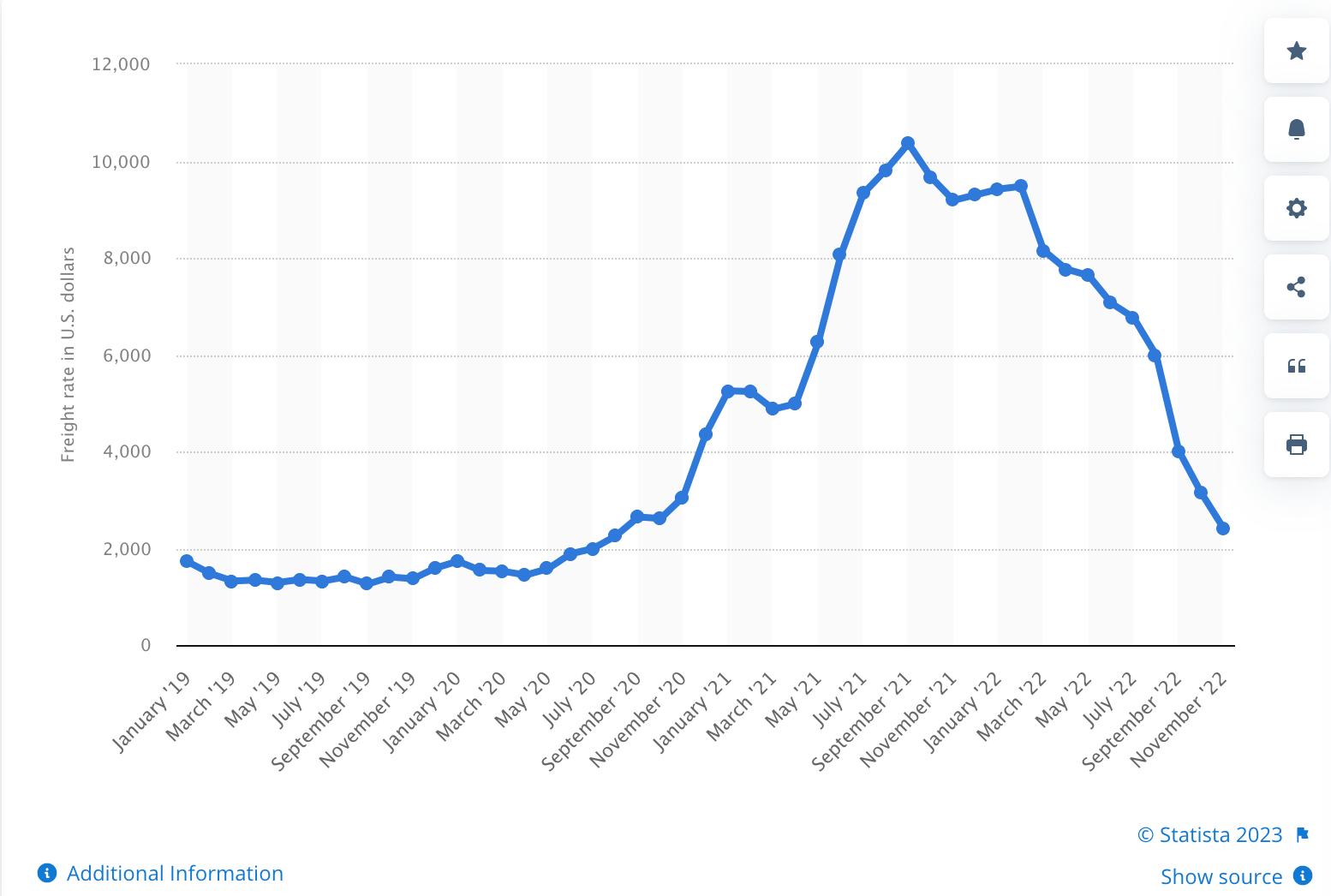

- As shown below, overseas freight costs were a significant margin headwind during 2022. After peaking in 3Q21, freight costs have plummeted by over 70%. This sets up a nice tailwind heading into 2023.

Global Freight costs 2019-22 (Statista)

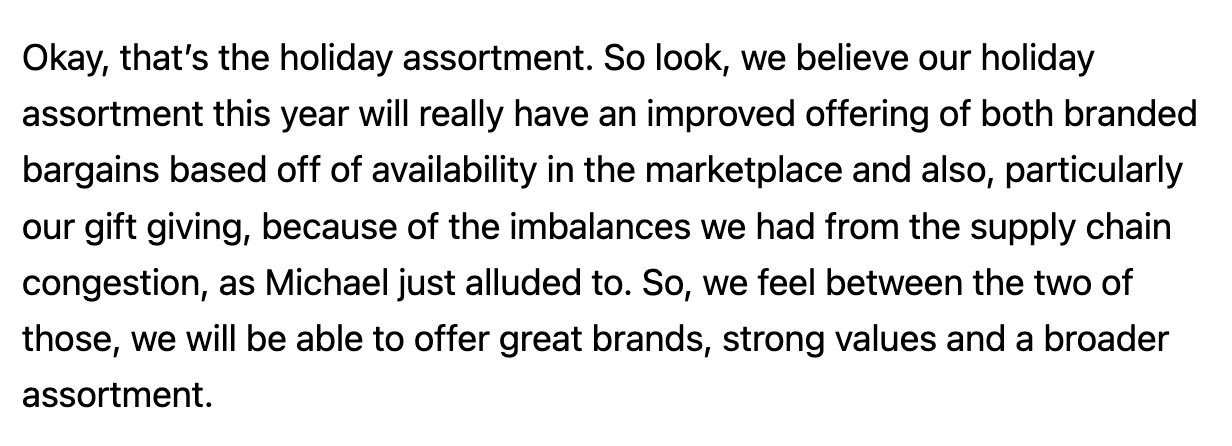

- In addition Ross management has cited excellent availability of merchandise from suppliers, which is in sharp contrast to the year earlier period when supply chain constraints left many shelves bare.

Commentary on Merchandise Availability (Ross 3Q22 Earnings Transcript from Seeking Alpha)

Valuation

While the fundamental outlook for Ross Stores has improved, I see this as being fully reflected in the stock. As we sit today, shares trade at nearly 24x 2023e EPS. This is near the high end of the company’s 10 year historical trading range of 16-25x EPS.

It is worth noting that the 2023 consensus EPS estimate of $5/share doesn’t appear to incorporate a full normalization of historical operating margins. Historically Ross has consistently earned operating margins of 13-14% over the past decade vs an expected ~10.5% in 2022 and 11.5% in 2023. Applying a 13.5% operating margin to the 2023 consensus revenue estimate (and adjusting for interest and taxes) gets me to normalized EPS of about $6 per share.

At $120/share Ross trades at 20x my estimate of normalized EPS which is in line with the midpoint of its historical range. As such, I see the company as fairly valued here.

Conclusion

While I expect Ross will show significant improvement in its financial results over the next year, at nearly 24x 2023e EPS (and 20x my estimate of normalized EPS), I see shares as being fairly valued.

As a leader in the attractive off-price retail space, Ross is a business I’d be interested in owning at the right price. As a value investor, I typically look to buy in at a 30% discount to my estimate of fair value. As such, I’d be interested in buying Ross shares should the stock trade back below $85/share.

Be the first to comment