Enes Evren

The market environment remains volatile despite the recent inflation lull. But Lakeland Bancorp, Inc. (NASDAQ:LBAI) demonstrates resilience. It continues to balance growth with fundamental soundness. Its robust performance, shown by revenues and margins, is a testament to its durability. Also, it keeps a stellar Balance Sheet, giving it more agility amidst macroeconomic changes. It may sustain its impeccable operations as growth prospects become more attractive. It only has to be more careful as interest and mortgage rates stay on the rise.

Even better, dividend payouts continue to increase with enticing yields. They remain well-covered as cash inflows remain steady and adequate. Moreover, the stock price stays in an upward movement but remains reasonably cheap.

Company Performance

Market rebound may still be uneven and incomplete, but there has been a notable improvement in recent months. Macroeconomic indicators may be mixed, but they appear more manageable today. Amidst all these changes, Lakeland Bancorp, Inc. maintains a solid growth while balancing it with fundamental stability. Its cope operations remain solid and impressive, showing it can withstand the blow of potential recession.

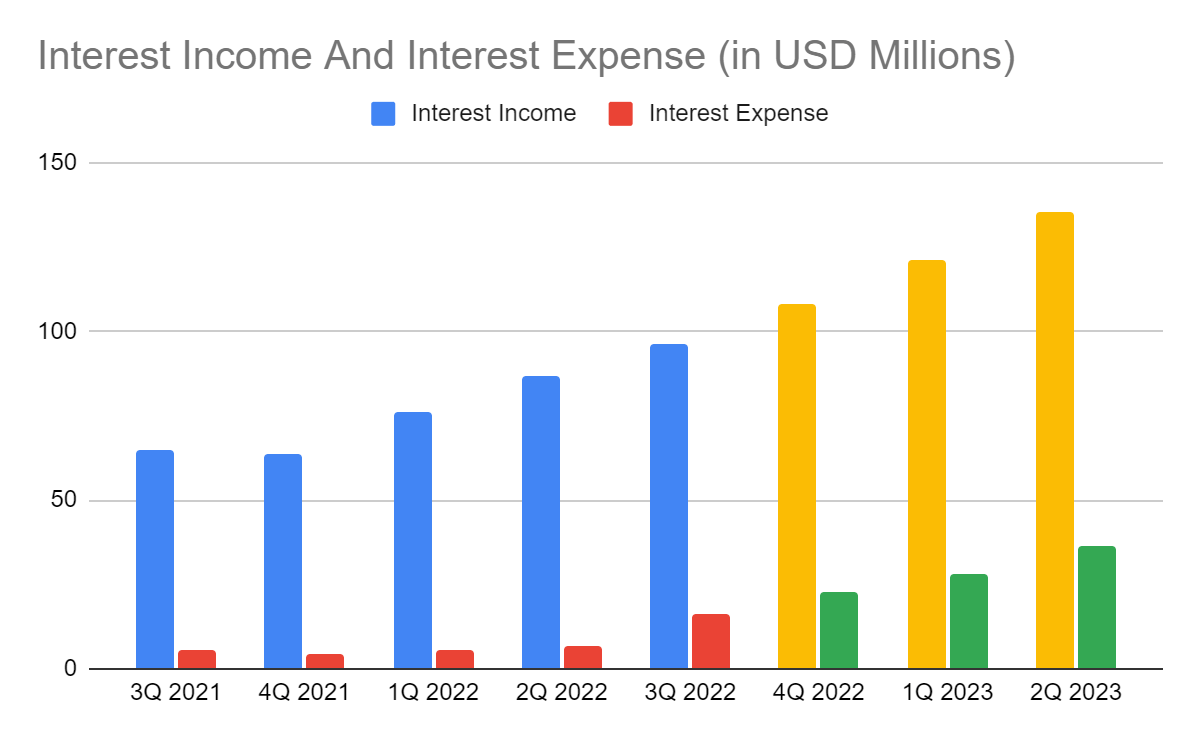

Its operating revenue in the form of interest income amounts to $96.43 million, a 48% year-over-year growth. With that, the company continues to move in line with interest and mortgage rate hikes. It has become more visible in the second half of 2022. Thanks to its interest-sensitive assets, generating higher yields. To be more specific, we will focus on various factors driving its massive revenue growth.

First, LBAI enjoys solid loan growth amidst interest and mortgage rate increases. It is no surprise as it keeps excellent credit quality to stabilize defaults and delinquencies. Loan components are more sensitive to interest rate increases, leading to higher yields. Even better, it has grown by 29% on an annualized basis.

Second, LBAI manages its investment portfolio with high prudence. If we check the balance sheet, a considerable portion of its securities are backed by the government. Its available-for-sale investment securities are composed of 33% treasury and municipal bonds. These investments are inflation-linked, which can hedge devaluation. Also, the remaining portion of investments are debt securities. These have a direct correlation with interest and mortgage rate changes. So their yields are about twice as much as they were in 3Q 2021.

Third, there is a noticeable improvement in the US economy. The lull continues despite the increased spending in the Holiday season. It is now only at 6.5%, the lowest in 2022. Even better, New Jersey and New York have a lower inflation rate of 6.2% and 6.3%. Individuals are more optimistic that rates may decrease further to 5.2% this year. Thanks to the effort of the Fed and the slight cooling of sales in the real estate sector.

Interest Income And Interest Expense (MarketWatch And Author Estimation)

Likewise, interest expenses continue to rise, reaching $16 million, almost thrice as much as it was in 3Q 2021. It also shows the largest sequential increase from only $7 million in 2Q 2022. Despite this, its year-over-year net interest income is a substantial increase from the comparative period. It shows that loans are more interest-sensitive than deposits. Also, nearly 30% of deposits do not bear interest. Meanwhile, operating expenses are manageable despite the higher prices. It is safe to say LBAI maintains efficient management in both interest and non-interest segments. So while margins are down, stability is evident in 2022 quarters.

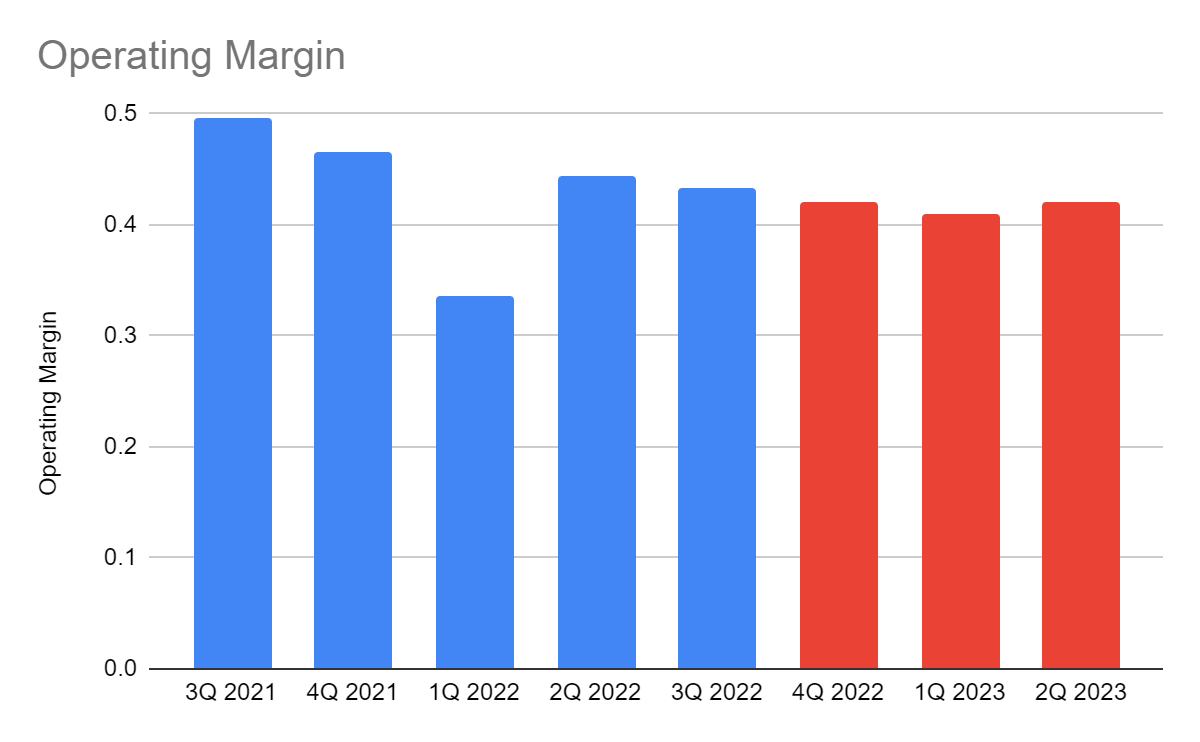

Operating Margin (MarketWatch And Author Estimation)

This year, I expect more enticing growth aspects as macroeconomic indicators become more predictable. Labor market conditions are stable, given the well-maintained unemployment rate. Interest rates may still increase, which is a sound choice to ensure inflation stability. There may be higher purchasing and borrowing capacity among buyers and borrowers. I expect interest income to increase faster, given the interest-sensitive loans and investments. Likewise, interest income may stay in its current trend. Meanwhile, the operating margin may become more stable. The impact of inflation on operating expenses can also help maintain the viability of the company.

How Lakeland Bancorp, Inc. May Fare This Year

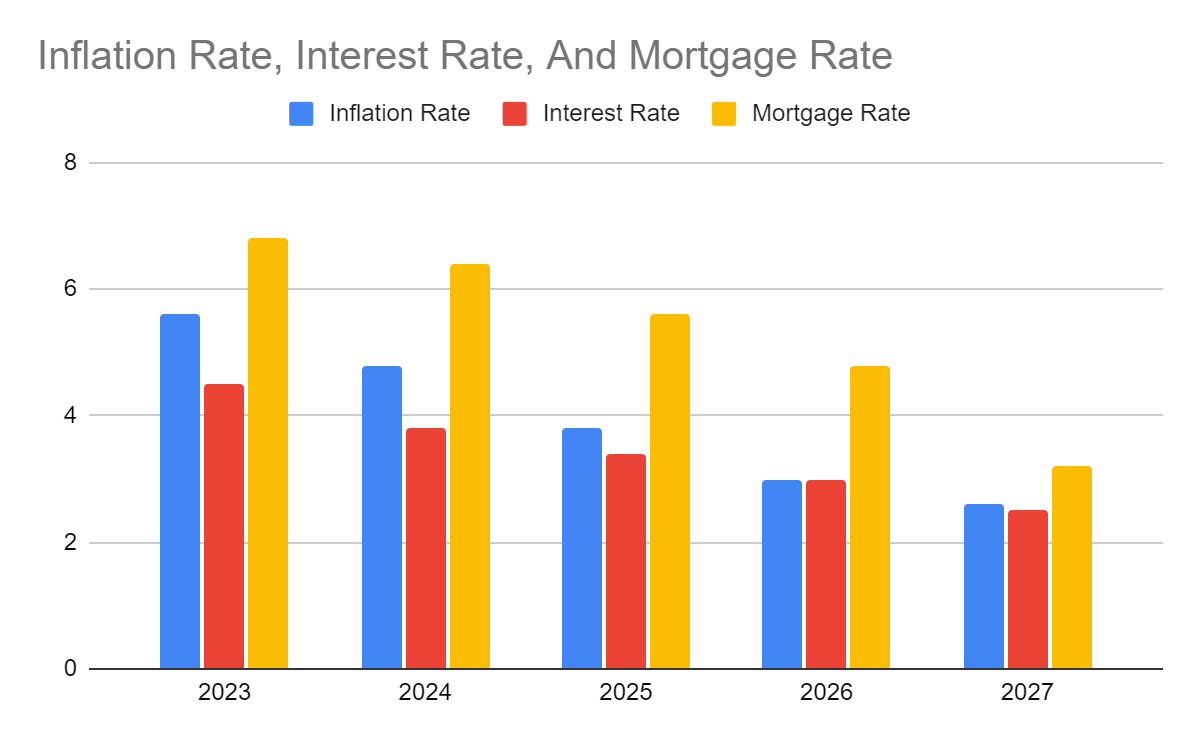

Market volatility remains evident and should not be discounted. But we must take a look at how inflation remains in a lull despite business reopenings, easing of restrictions, and holiday spendings. Despite this, the Fed must stick with its contractionary monetary policy. I expect interest rate hikes to continue, but increments may be more stable, reaching 4.5%. As such, I expect inflation to decrease further to 5.6%, a bit higher than 5.2% market expectation.

With regards to mortgage rates, I expect more stable values this year. But to be more conservative, I set it at 6.8% this year. House sales appear to have cooled down in recent months, but prices remain high. I attribute it to low property inventory that cannot suffice market demand. It is one of the reasons I don’t agree with the forecast of a massive real estate crash. Demographics are also changing, while income levels are increasing, raising purchasing power. Delinquencies must not be discounted, but I am more optimistic about the company performance.

Inflation Rate, Interest Rate, And Mortgage Rate (Author Estimation)

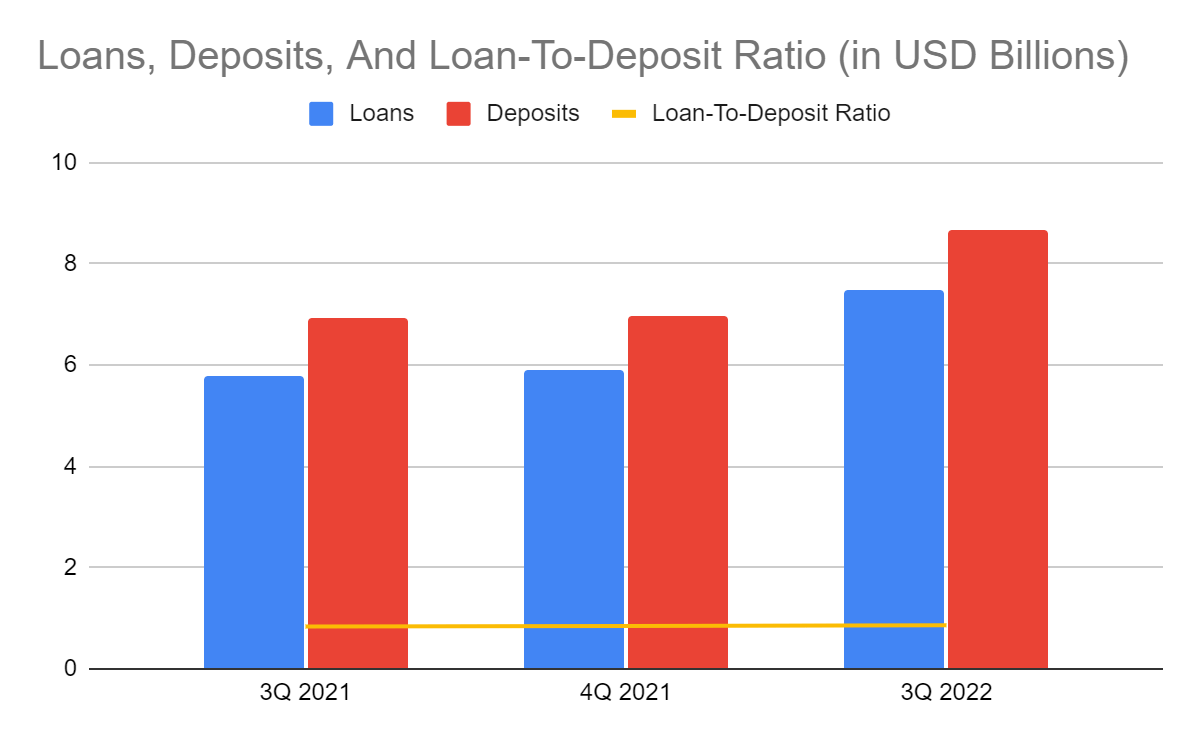

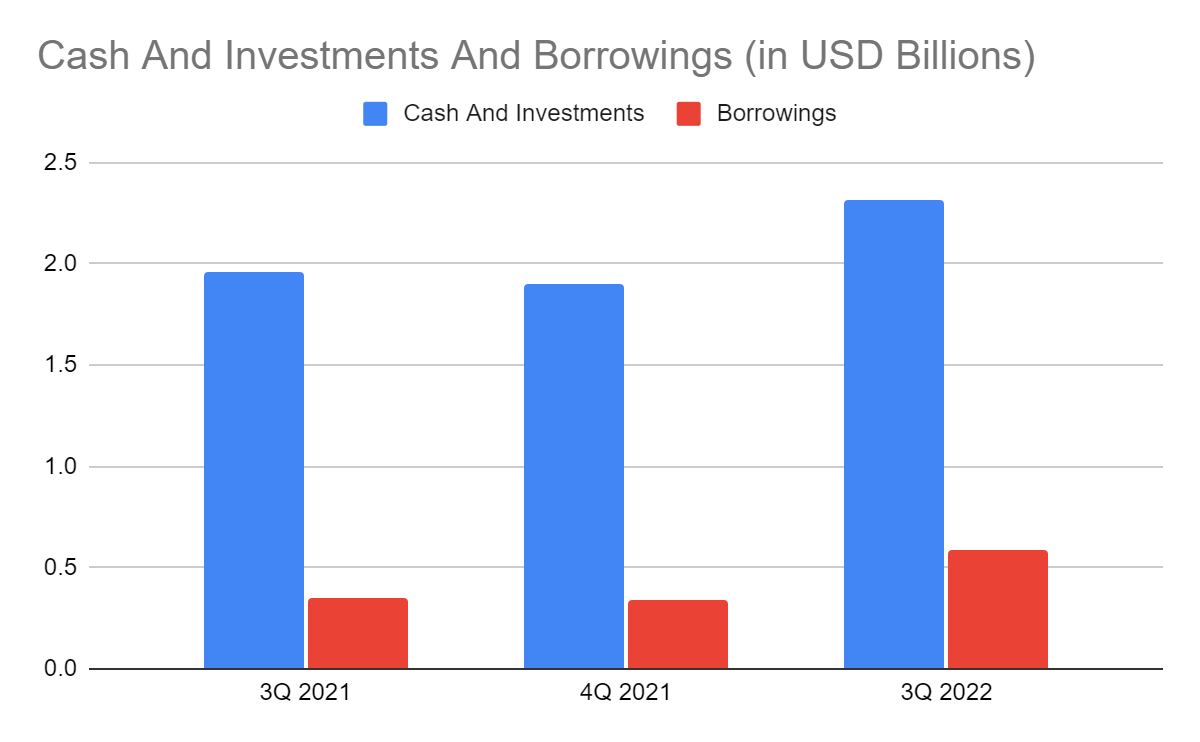

What makes it a solid company is its stellar Balance Sheet. LBAI maintains an excellent liquidity position as one of its strongholds. Aside from the ideal loan quality and growth, reserves are stable. Loan-to-deposit ratio remains acceptable at 86%. It is within the standard rate of 80-90%, so LBAI can make up for potential defaults. It also shows it has not unleashed its full potential yet. The thing is it can lend more to maximize revenue growth and margins. It can even maintain its liquidity by raising rates to attract more deposits. Instead, it stays conservative to balance between growth and stability. More importantly, cash and investments are increasing and comprising 24% of the total assets. These are enough to cover company liabilities aside from deposits. The company earns enough, given the Net Debt/EBITDA Ratio of 2.5x, proving its liquidity.

Loans, Deposits, And Loan-To-Deposit Ratio (MarketWatch)

Cash And Investments And Borrowings (MarketWatch)

Stock Price Assessment

The stock of Lakeland Bancorp, Inc. remains in an uptrend. After months of downtrend, the rebound continues, which is adherent to fundamentals. At $18.46, it remains 7% lower than its price last year. The stock price may not slow down soon as price metrics point out to potential undervaluation. The price-earnings multiple of 11.8x and my estimated EPS of $1.88, giving a target price of $22.24. NASDAQ remains optimistic with an EPS estimation of $2.01-2.1 or a target price of $23.74-24.76. Given this, there may be a 20-32% upside in the next 12-18 months.

Moreover, it maintains consistent and well-covered dividends. It has a dividend yield of 3.16%, which is way better than the S&P 600 and NASDAQ average of 1.24% and 1.26%. It has a dividend payout ratio of 51% so it has enough means to sustain dividends. To assess the stock price, we will use the DCF Model.

FCFF $98,200,000

Cash $232,000,000

Borrowings $604,000,000

Perpetual Growth Rate 4.8%

WACC 9.2%

Common Shares Outstanding 64,804,579

Stock Price $18.46

Derived Value $24.52

The derived value agrees with the optimistic view of the stock price, given the potential undervaluation. There may be a 32% upside in the next 12-18 months. Investors may also take this opportunity to consider buying stocks.

Bottom line

Lakeland Bancorp, Inc. balances growth and stability amidst macroeconomic volatility. It is poised for more opportunities as inflation cools down. It can sustain its potential expansion even without raising its financial leverage. As we can see, it remains conservative even with its robust performance. So dividends are consistent and realistic with better-than-average dividend yields. Even more exciting is its stock price, which adheres to fundamentals. It still shows undervaluation despite its continued rebound. The recommendation is that Lakeland Bancorp, Inc. is a buy.

Be the first to comment