Ian Tuttle

Thesis

Despite the selloff in Roblox (NYSE:RBLX) shares, we do not believe this is a moment to buy the dip. Roblox is financially deteriorating and should be avoided by investors until there is a significant improvement.

Accelerating Losses and Stagnating Revenues

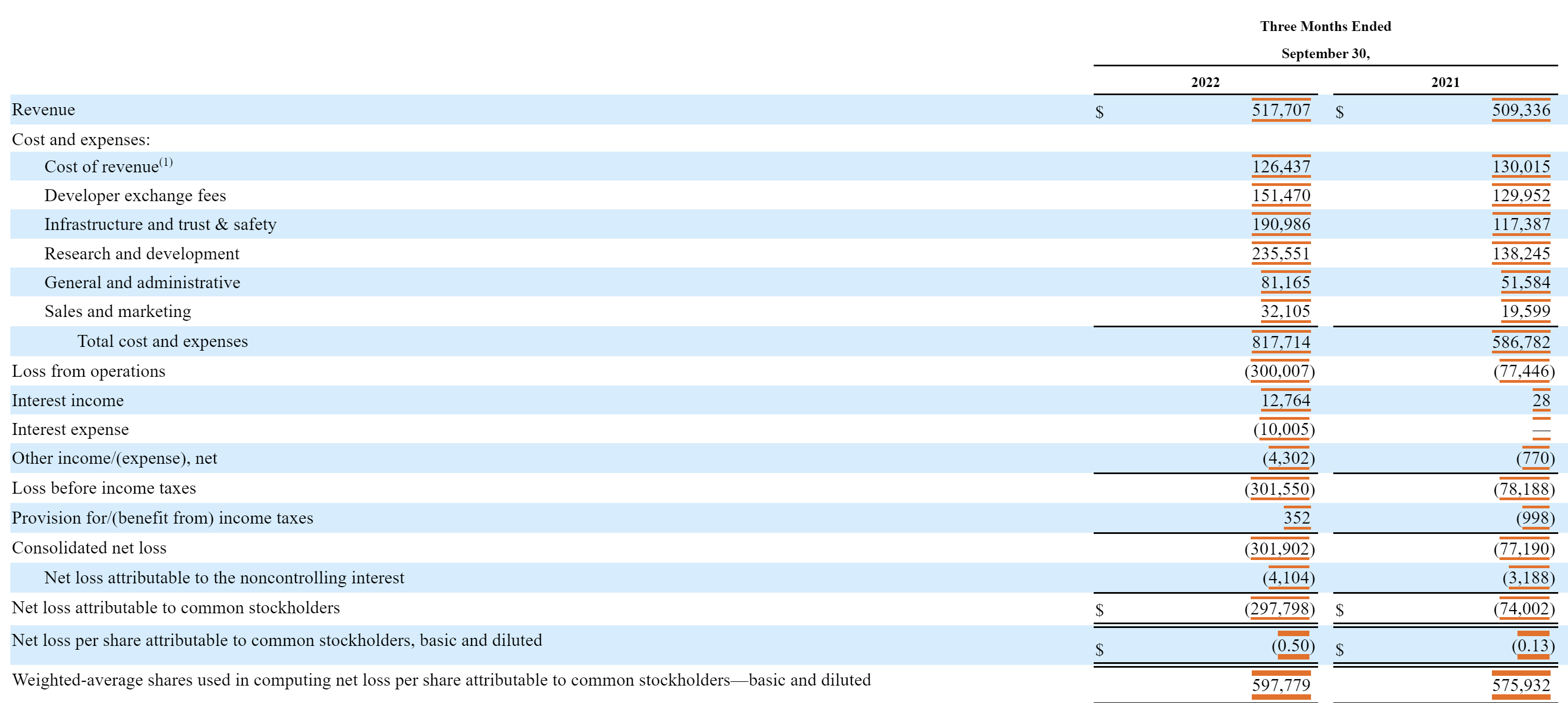

Roblox had a horrendous Q3, with net losses increasing to $297 million from $74 million a year earlier. These accelerating net losses were accompanied by a paltry 1.64% growth in revenue.

Income Statement (Roblox Q3 Earnings Report)

We can see that the bulk of the increase in expenses can be attributed to the “infrastructure and trust & safety” and “research and development” segments.

There has been a massive uptick in safety concerns regarding Roblox. I’ll leave readers to go search the internet for the numerous blog posts and articles about child safety on Roblox. Roblox has been heavily criticized for hosting content on the platform that isn’t child-friendly as well as there being interactions on and off platform that aren’t child-friendly. The moderation of user generated content can get pretty expensive. Roblox is taking necessary steps to combat concerns over child safety. A fair criticism to be had is why these expenses weren’t occurring in the past, when child safety was just as important.

As far as research and development is concerned, the company is seeking to improve and expand their platform. The main goal of research and development is to attract and retain users in the Roblox ecosystem through new and existing content. If the meager 1.64% growth in revenue is any indication, the company needs to do a better job at this.

At the end of the day the company operates a platform that hosts user generated content. This should be a high net margin business, and yet it is not even close to that. Investors should also consider the fact that the video game industry changes frequently and video game players can be fickle and often move on to the next “big thing”. This means that Roblox faces significant risk of their player base not being durable. When they can’t even make money with their current user base this does not bode well for the company.

The massive uptick in expenses without a corresponding increase in revenue should be a huge red flag to investors. Unfortunately, the financials only get worse, with a balance sheet that is less than ideal.

Balance Sheet Concerns

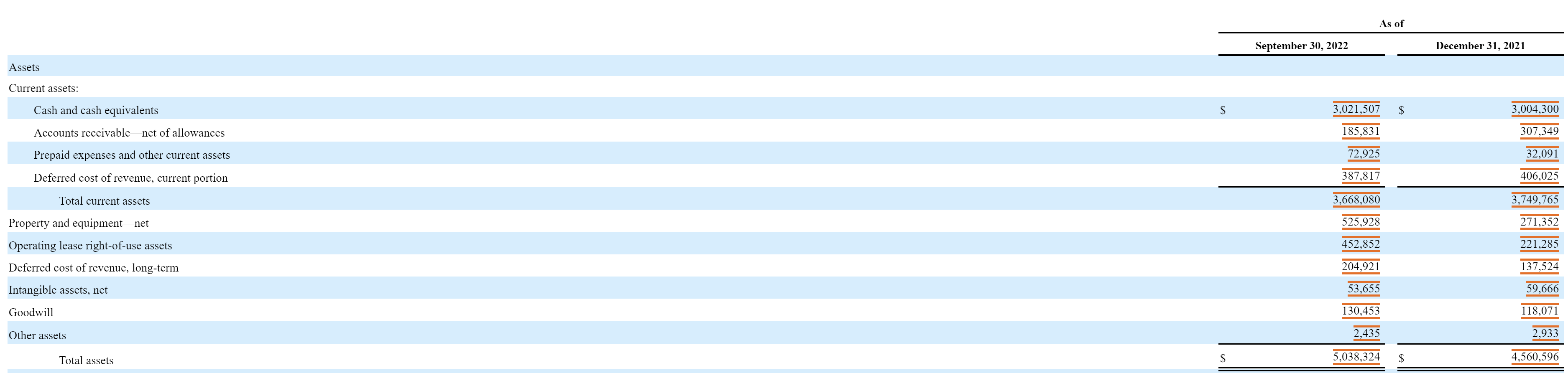

As far as the assets go there is a lot to like. The company has a large cash balance and a low amount of intangible assets and goodwill, which are both good things to see.

Assets (Roblox Q3 Earnings Report)

The liabilities side of the equation is where some problems arise. The company has nearly $1 billion in debt and a whopping $2.711 billion of deferred revenue. All of this deferred revenue is money received for goods or services which has not yet been earned, which means that much of the cash balance is questionable. If the higher operating costs are anything to go by, the amount it costs to actually earn this revenue may be more than the company initially expected.

Liabilities (Roblox Q3 Earnings Report)

As far as stockholders’ equity is concerned, we can see that the company has accumulated losses of $1.6 billion. Considering Roblox merely operates a platform and hosts user-generated content this does not reflect well on the company. It is possible that Roblox has a model which is fundamentally broken and has relied solely on investor funds and borrowed money to facilitate their operations. If this money evaporates and they are unable to fix their operations investors will see another leg lower in the stock as they tap the debt and equity markets once again.

Stockholders’ Equity (Roblox Q3 Earnings Report)

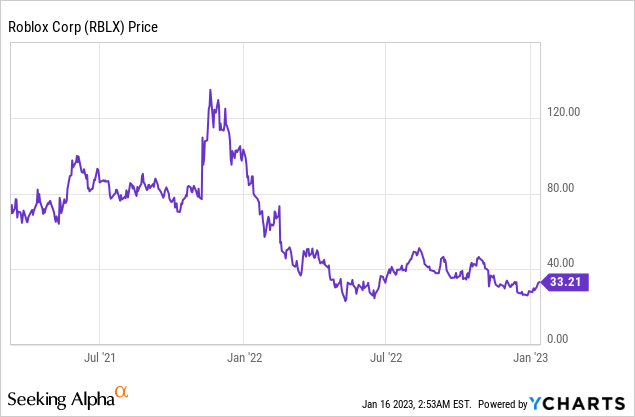

Price Action

Roblox stock was once a Wall Street darling, with many touting it as the next metaverse play. Despite the stock selling off quite dramatically we think investors should stay away and not buy the dip. There are too many questions regarding the business model and their execution has been poor.

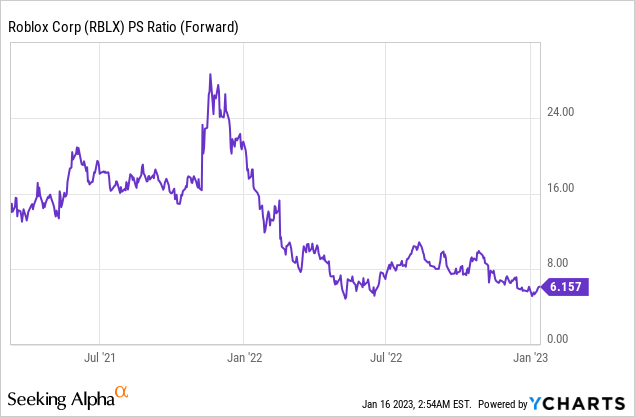

Valuation

Roblox has never made any real profits so valuing them on a PE basis is futile. When looking at price to sales the company does appear to be selling at a discount to its historical multiple. A price to sales multiple above 6 is still quite high, especially for a company with deeply negative net margins and essentially zero revenue growth.

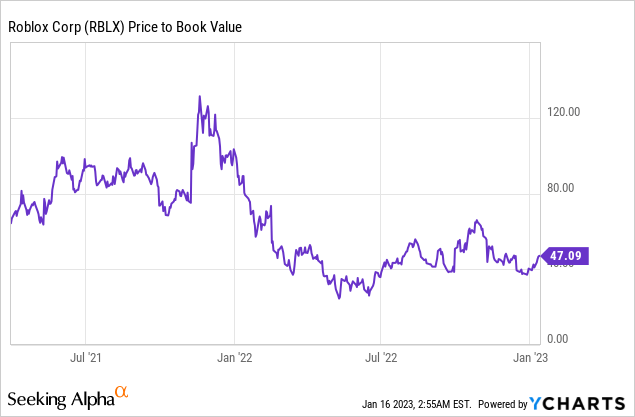

On a price to book value the company has always traded richly. We expect book value to go negative as the company continues to light money on fire.

Risks

Some risks to this bearish thesis are as follows:

Roblox is able to expand their user base through new product offerings.

Roblox becomes a metaverse platform and fulfills the metaverse bull case for the company.

Roblox is able to attract and retain users in a cost-effective manner.

Roblox is able to unlock operating leverage in their model and dramatically increase profitability.

Roblox is able to meaningfully improve the safety of their platform.

Roblox is able to moderate content and keep their platform safe in a more cost-effective manner without compromising quality.

Despite the things that could go right, we view the overall risk/reward as being simply terrible. Operations and finances are trending in the wrong direction and their business appears to be structurally flawed in an industry that is notorious for having player bases gradually move on.

Key Takeaway

We believe investors should stay away from Roblox until they show significant improvements. Amid accelerating losses, essentially zero growth, and a mediocre balance sheet there is not much to like about the company. The video game industry is not like traditional software yet the market seems to want to value Roblox as a software company. All we see are red flags and a dismal risk/reward.

Be the first to comment