enter89

Stocks opened higher yesterday on better-than-expected inflation news for producer prices, which offset concerns about a weaker-than-expected retail sales report. The tug of war between disinflation and a slowing rate of economic growth is likely to continue throughout this year until the consensus is confident that a recession is no longer on the horizon. It looked like the bulls had the upper hand yesterday until hawkish comments from two Fed officials drove stock prices sharply lower. James Bullard and Loretta Mester both asserted that short-term rates would need to be raised above 5% to bring inflation down to target. This runs counter to market expectations for a terminal rate of 4.88%. I trust the market more so than Fed rhetoric, as I think Fed officials are simply trying to jawbone the market lower to keep financial conditions from loosening.

Finviz

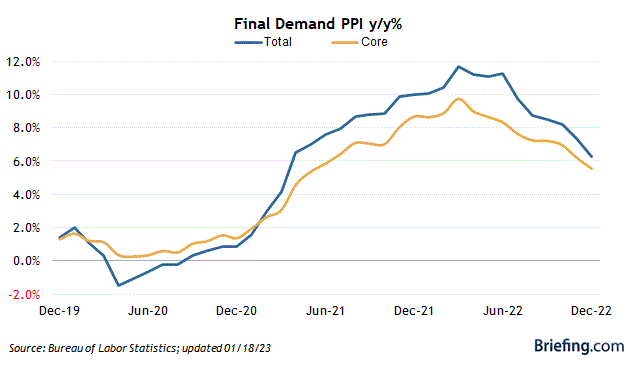

Continuing a disinflationary trend that started last spring, producer prices fell in December by the most in one month since the start of the pandemic. The Producer Price Index declined 0.5%, which was well below expectations for a 0.1% decline, and the previous month was revised lower from 0.3% to 0.2%. In particular, food prices fell 1.2%, which was the most in two years. The annual increase in the overall index fell from 7.3% in November to 6.2% in December. This should lead to a further decline in consumer prices, as supply chains normalize and supply and demand fall back into balance.

Briefing.com

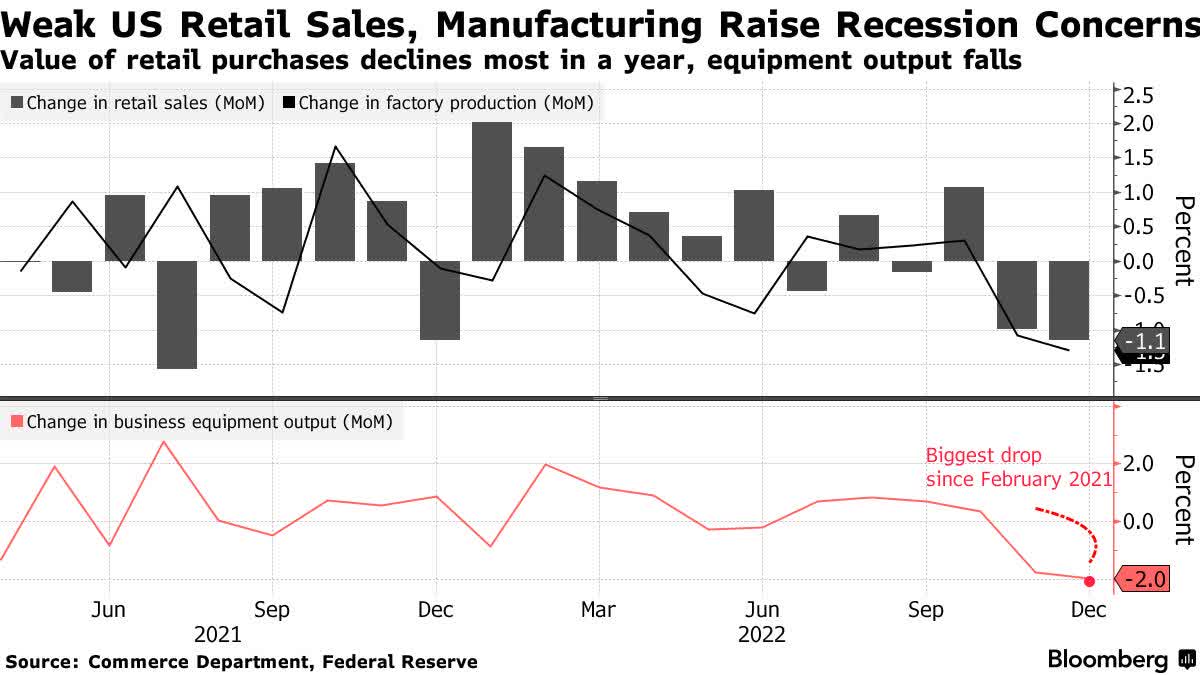

In the process of seeing supply and demand fall back into balance, demand must slow, which is what we saw in yesterday’s retail sales report. As consumers have continued to shift spending from goods to services, it comes as no surprise that the sale of “stuff” was down for a second month in a row. Sales fell 1.1% in December, which was below the estimate for a decline of 1%, and it is rare to see two back-to-back months of sales declines. One contributing factor, due to the fact that sales are not adjusted for inflation, is that excessive discounting at year end weakened the overall number. I saw several anecdotal signs of this in December. Still, we want to see weaker demand to bring price increases down further, as we can’t have one without the other.

Bloomberg

Although this decline in the sale of goods fuels recession concerns again, especially when Fed officials douse the flames with hawkish rhetoric, as they did yesterday. I am not yet concerned. The number to focus on with respect to retail sales is the year-over-year number that is inflation adjusted or real. Prior recessions did not begin until annualized real retail sales declined within a range of 1-3%. We had a bit of a scare last March when sales fell 1.4% by the metric, but we quickly recovered the following month.

FRED

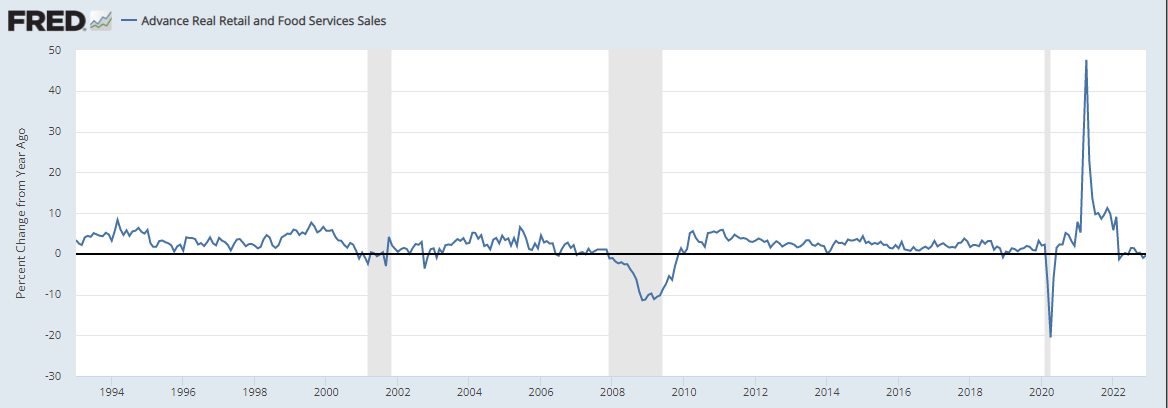

Last month there was a decline in real retail sales of 0.37%, which does not qualify, but this number requires continual monitoring. My outlook for a soft landing is conditioned on the rate of inflation falling at a faster pace than the rate of wage growth, which should restore real-income growth later this year. If we have growth in real income, that should support real retail sales growth. More importantly, it should support growth in real consumer spending, which includes spending on goods and services.

FRED

Therefore, this decline in stock prices yesterday and today looks more like a pause to refresh after we had a sizzling rally to start the year. The technical backdrop for the market continues to improve, as I have discussed over the past two days, but prices do not go straight up. These pullbacks will breathe life into the bearish narrative, but I am going to continue to focus on the rate of change in the data instead of Fed rhetoric and the emotional whims of the market from day to day.

Lots of services offer investment ideas, but few offer a comprehensive top-down investment strategy that helps you tactically shift your asset allocation between offense and defense. That is how The Portfolio Architect compliments other services that focus on the bottom-ups security analysis of REITs, CEFs, ETFs, dividend-paying stocks and other securities.

Be the first to comment