DNY59

I have long pondered the impact of rising rates on various parts of the market and particularly on REITs. My conclusion has consistently been that REITs are not any more susceptible to rising rates than the broader market.

On Monday, 9/26/22, the ten-year Treasury yield shot up to around 3.9% which sent REITs down about 3% intraday. Other major indices were only down about 1% at the same time in the middle of the trading day.

The market says I am wrong.

I don’t listen to market price to make conclusions about fundamentals. I firmly believe fundamentals drive market price and not the other way around. However, when the market so unanimously delivers a verdict that contradicts the fundamentals, it is worth taking the time to remeasure and see if I got something wrong. In this effort, I will examine the prevailing theories as to why REITs might take it on the chin in a rising interest rate environment.

I have made an honest attempt to look at each theory with an open mind. We will cover each theory in detail and show how we arrived at our conclusions.

Theory #1: REITs carry high debt loads, which will get more expensive as rates rise

Theory #2: REIT debt is going to get more expensive, which will drag down earnings

Theory #3: REITs are owned by those seeking income and thus lose part of that constituency as other fixed income assets become more viable

Each of these theories is discussed among financial professionals and frequently is brought up in financial media. I have personally witnessed all 3 discussed on CNBC, which is broadly considered a respectable source of financial news. Thus, I will give proper respect to the potential merits of these arguments, including the ones with which I disagree.

Theory #1: REITs carry high debt loads – Not valid due to factual error

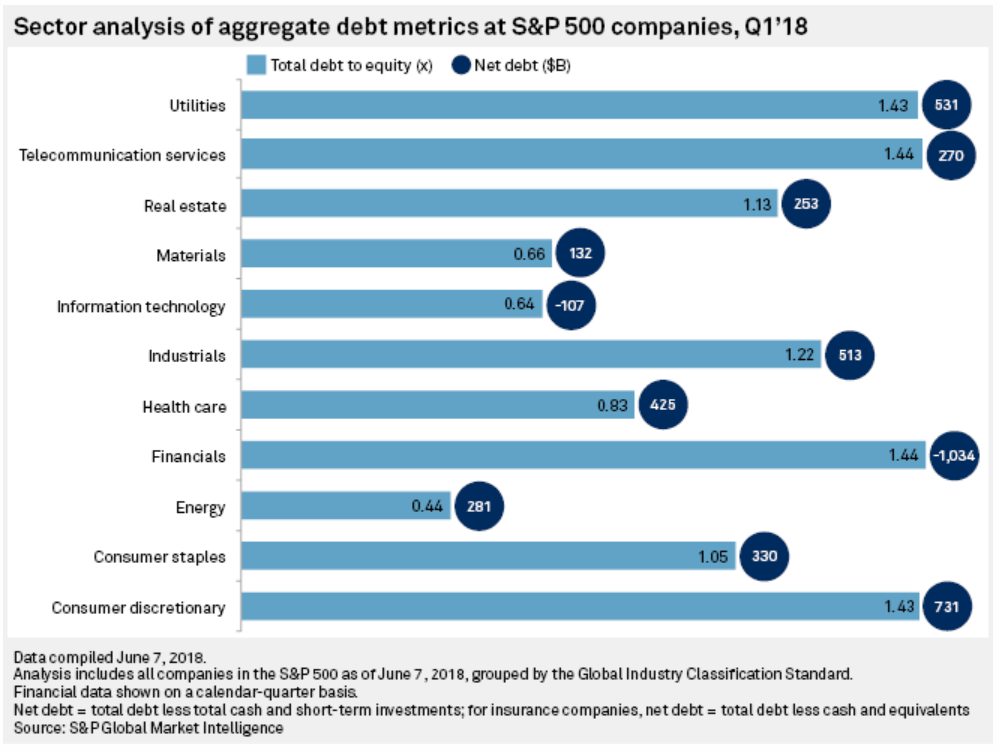

REITs do have debt, but the term high debt would indicate that their debt burden is high relative to something else, which would presumably be the broader market.

This is factually incorrect.

There are 11 GICS sectors. 5 of them have higher debt to equity than real estate, and the other 5 have less debt to equity than real estate.

S&P Global Market Intelligence

REITs are approximately in the middle of the pack in terms of absolute levels of debt.

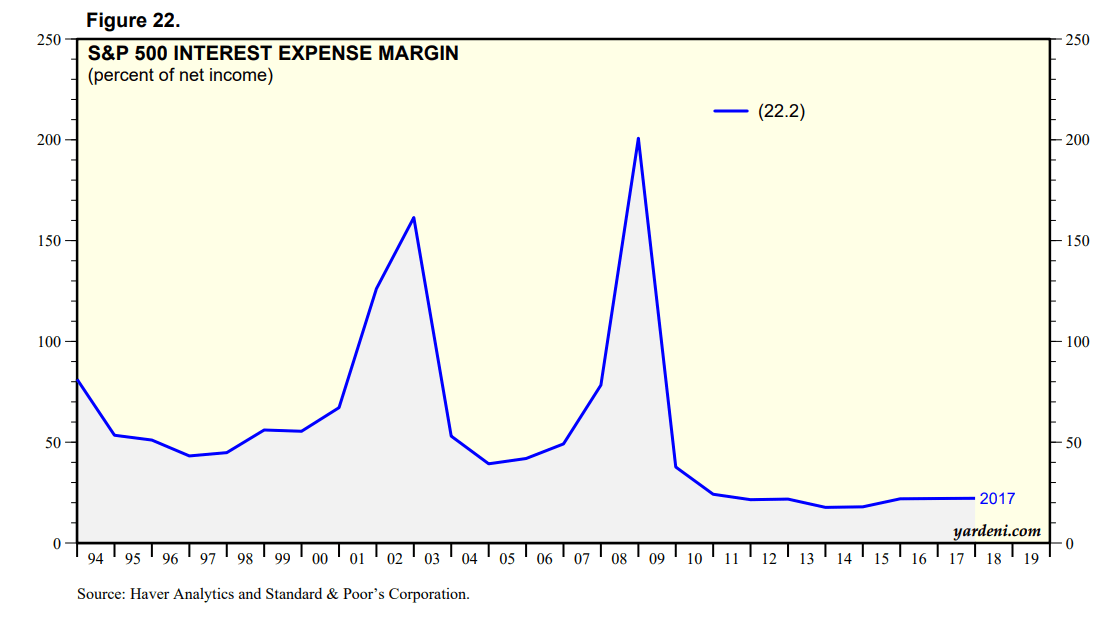

If one looks at debt expense relative to earnings, REITs are also at a fairly normal level. Yardeni data shows that S&P interest expense was about 22% of net income in 2017. It was significantly higher in previous years when interest rates were higher.

Yardeni

I was not able to find the same statistic for the REIT index, but looking at individual REITs it is roughly in line.

The largest REIT, American Tower (AMT) had 277 million of interest expense in 2Q22 and $1.649B of FFO (earnings) which equates to about 16.8% interest expense as a percentage of earnings. AMT’s debt to capital is 28% which is slightly lower than the REIT average, so one would expect the average REIT’s debt expense to be slightly higher than AMT’s

W. P. Carey (WPC) has an average level of debt and in 2Q22 it had 18.2% interest expense as a portion of FFO.

Small cap REITs are probably going to be a bit higher, just as the Russell 2000 would be a bit higher.

Given the similar magnitude of debt and debt expense, this should not cause REITs to underperform in a rising rate environment.

What about the nature of the debt?

Theory #2: Rising debt costs will hurt REITs – Disagree because offset by higher revenues

Sometimes I feel like the market views debt as the Sword of Damocles, ready to come crashing down at a moment’s notice, or in this case surging interest expenses.

The thing with debt though is that it is taken out to purchase assets or otherwise generate business. If one looks at the debt in isolation, rising rates are of course a bad thing as the debt becomes expensive, but the more realistic attribute to look at is the comparison between income streams and expense streams.

So yes, REIT debt will get more expensive, but the assets associated with that debt will also generate more revenues. See, the higher interest rates go, the more burdensome it is for potential tenants to buy a property. Now that mortgage rates are in the 6%+ range, homes are less affordable causing more to stay in the rental market. Thus, apartments can charge more rent.

It is the same in other sectors. Tenants don’t want to buy their own shopping centers, data centers, towers, etcetera, so they rent. Rental rates are positively correlated to interest rates and, in this case, the correlation is causal in nature.

Given higher rental revenues offsetting rising interest expense, the question becomes one of duration in the bond sense of the word. For those unfamiliar, duration is essentially a measure of how far in the future the weighted average remaining cash flow of a bond is.

Extrapolating that out to the company level, a company with asset duration longer than liability duration will be hurt by rising rates while a company with asset duration shorter than liability duration will generally be helped by rising rates.

In this regard, both REITs and the S&P have done a good job terming out their debt and locking it in at fixed rates.

As of August 2022, the weighted average term to maturity on REIT debt was 87 months and close to 90% of REIT debt is fixed rate.

That gives quite a large window for the revenue side of the equation to kick in. Real estate itself is a very long-term asset, with well-maintained buildings lasting centuries in some cases and at least 40 years for just about every kind of real estate. This long asset life is often mistaken as REITs having long-duration assets.

The duration of a REIT’s revenue is not the life of the asset, but rather the current lease term. Over the next 7 years, before REIT debt gets the chance to tick up, REITs will get to reset the majority of their revenues to the now significantly higher market rate.

REITs are a low duration asset with higher-duration debt. That is good for a rising rate environment in terms of the bottom line.

Theory #3: Capital flows will hurt REITs – Largely true and probably the reason REITs have fallen so much

There are significant differences between the investor bases of REITs and the S&P.

For starters, 80% of S&P is owned by institutions while REITs are closer to 60%.

Note that in both cases, the institutional ownership counts ETFs even though the end owners of those ETFs are at least partially retail investors. Thus, the number for both is significantly lower, but even after adjustment, REITs still have significantly more retail investors.

Retail investors are the most educated they have ever been about the market, but they still don’t have quite the level of knowledge and experience that the institutional investors have. As such, they are more prone to buy or sell for non-fundamental reasons. This could potentially explain why REITs have more volatility both to the upside and downside, despite REIT underlying cash flows being slightly steadier than those of the S&P.

Another big difference in investor base is a large portion of REIT investors are income investors. Since REITs have a significantly higher dividend yield at 3.77% vs. the S&P at 1.69% it makes sense as an income vehicle.

However, this also means that REITs compete more directly with bonds for the portion of investors that are looking primarily for investment income. Thus, as bonds get more attractive as a result of rising rates, it could cause capital flows from REITs into bonds.

I suspect it already has.

Investors of course have a variety of levels of risk tolerance. When interest rates were near zero, even some of the more risk averse were likely forced out of their comfort zone as Treasuries provided negative real returns. Many likely wound up in REITs as a higher yielding bond substitute, given the predictable nature of cash flows.

In 2022 as rates shot up, that trend has probably been reversing. On 9/22/22, about $60 million dollars flowed out of the Vanguard Real Estate ETF (VNQ)

ETF.com

The data for 9/26/22 is not yet available, but I suspect it is even worse.

I have summarized the 3 main theories for why REITs are suffering in this environment into a table.

|

Theory |

True/False |

Reasoning |

|

REITs are high debt |

False |

REIT debt levels are in-line with broader market |

|

Rising rates will hurt REIT earnings |

False |

Interest expense will be offset by rising rental revenues, which kick in sooner than debts roll off their fixed rates |

|

Capital is flowing out of REITs due to similar constituency to bonds |

True |

It makes sense rationally, and there is some preliminary data showing outflows from REIT ETFs. |

How I am playing it

Fully recognizing that fund flows could drive another leg lower, I think it is worth pointing out that fund flows are not a fundamental factor.

In other words, the market may continue selling REITs if rates continue to rise, but the rising rates are not actually hurting REIT earnings power. As such, the fundamental strength could cause REITs to rebound strongly from the artificially depressed level. I am not smart enough to time the bottom, so I am not going to attempt to.

Prices are well below fundamental values and rental rate outlook remains strong, so I am staying fully invested in REITs.

Be the first to comment