ablokhin

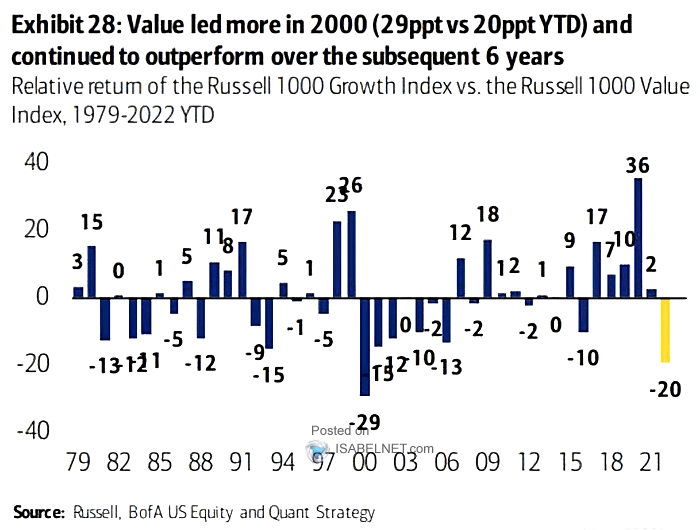

Value stocks finally had their day (or year) in the sun. In 2022, the value style beat growth by 20 percentage points, according to Bank of America. One group at the heart of the value trade is no doubt Financials. And within that sector, there are domestic regional banks that move in tandem with trends in the credit and broader economic cycle.

One stock has outperformed the S&P 500 in the last year, but earnings growth is a question mark. Are shares of Regions Financial (NYSE:RF) a buy here? Let’s check it out.

2022: A Banner Value Year

BofA Global Research

According to Bank of America Global Research, Regions Financial is a large-cap regional bank based in the Southeast with more than $160 billion in assets. Headquartered in Birmingham, Alabama, the company has over 1,800 branches and a leading market share in Alabama, Tennessee, and Mississippi. The company’s lending portfolio focuses primarily on C&I, residential mortgages, home equity, and commercial mortgage.

The Alabama-based $20.9 billion market cap Banks industry company within the Financials sector trades at a low 11.2 trailing 12-month GAAP price-to-earnings ratio and pays a 3.6% dividend yield, according to The Wall Street Journal. Back in October, RF missed earnings estimates while beating on the top line. Elevated expenses and a high amount of credit loss reserves were sore spots. Nevertheless, the stock has been a robust performer as it has beaten KRE by more than 10 percentage points since late October.

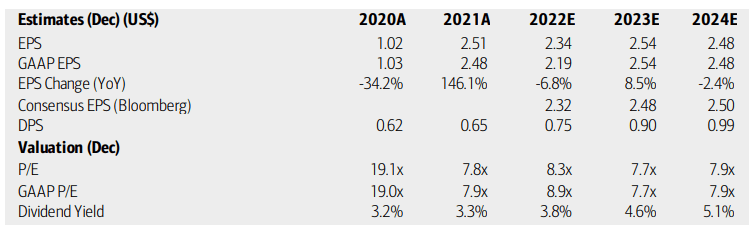

On valuation, analysts at BofA see earnings having fallen by nearly 7% in 2022, but a solid EPS recovery is expected this year. Per-share profits dip modestly in 2024 per BofA’s take, and the Bloomberg consensus forecast is about on par with that outlook. Dividends, meanwhile, are expected to increase despite ebbs and flows in EPS.

What’s ideal from the bulls’ perspective is that both RF’s operating and GAAP P/Es should continue to be low while the yield remains high. The stock has a forward PEG ratio of just 0.74, but its price-to-book ratio, important for banks, is above the sector median and RF’s 5-year average. Overall, the valuation is decent, but earnings growth might not be sustained for very long.

Regions: Earnings, Valuation, Dividend Forecasts

BofA Global Research

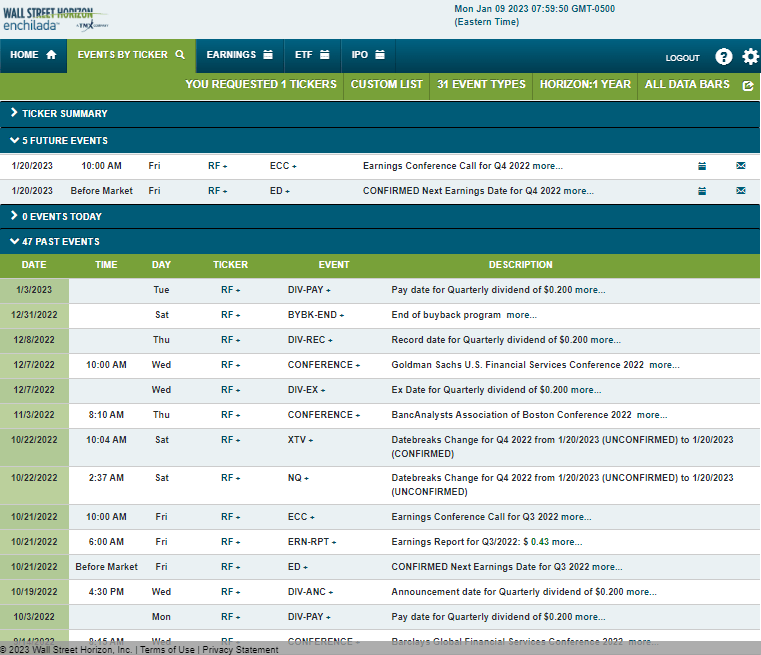

Looking ahead, corporate event data provided by Wall Street Horizon shows a confirmed Q4 2022 earnings date of Friday, January 20 before market open with a conference call later that morning. You can listen live here. The calendar is light on volatility catalysts aside from the reporting date next week.

Corporate Event Calendar

Wall Street Horizon

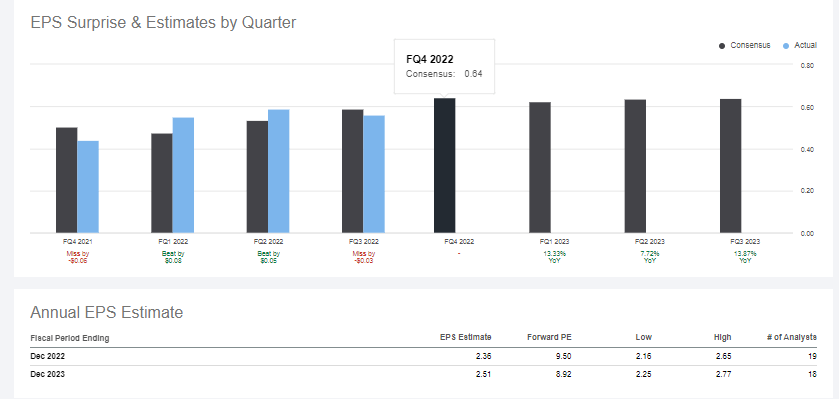

Looking ahead to the upcoming earnings report, Seeking Alpha reports that the consensus EPS forecast is $0.64 which would be a strong 45% increase from per-share profits earned in the same quarter a year ago.

Strong YoY EPS Growth Expected

Seeking Alpha

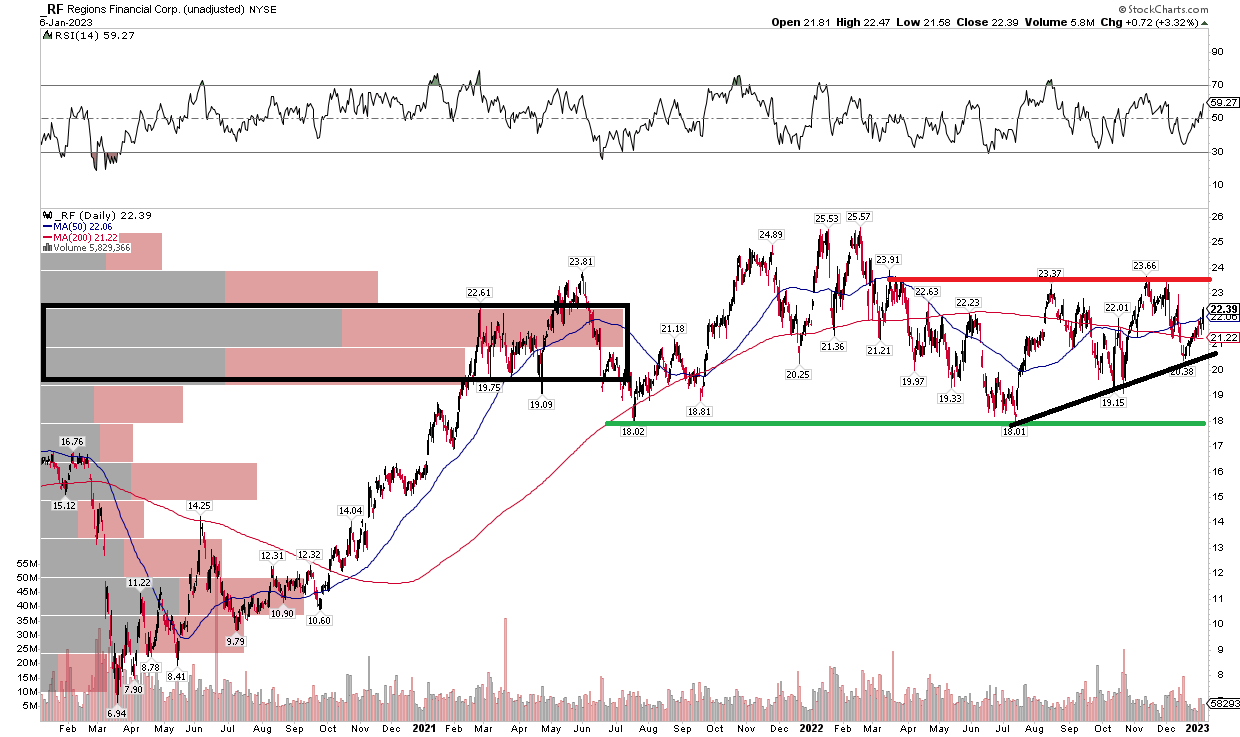

The Technical Take

RF has been simply trading sideways for the better part of the last two years. Shares peaked just above $25 in early 2022 as the value narrative that persisted throughout the year did not help the regional bank sustain upside for awfully long. Notice in the chart below that RF dipped from the mid-$20s to near $18 by July. Around that time, I noted that being long with a stop under $18 would be a favorable risk/reward play. While there has not been a big upside, support at $18 has indeed held, and I now see some resistance just below $24.

Should the stock break out above that level, a bullish measured move upside target to near $28 to $29 could be in play based on the pattern. I would like to see shares hold an uptrend support line from the mid-2022 bottom, too. Finally, this is a slushy spot for Regions as there is a high amount of volume by price in the $19 to $22 range – the good news there is that Friday’s close was above the upper end of that congestion zone. Overall, it is a wait-and-see approach, but I still lean bullish on the chart.

RF: Shares Consolidating Ahead of Earnings

StockCharts.com

The Bottom Line

Both the valuation and chart of Regions are lukewarm at the moment. There’s the potential for more gains off the October low, and I like the YoY relative strength, but the bulls have some work to do. I’d also like to see a more upbeat tone from the management team on the earnings call next week.

Be the first to comment