FinkAvenue

Thesis

Lululemon Athletica Inc. (NASDAQ:LULU) stock is down approximately 10% (pre-market trading reference) after the company updated its guidance for the December quarter and warned about a material drop in gross margin. Although a slightly stronger than expected topline growth is encouraging, investors should consider that the current market environment is all about profitability – and less about growth. Thus, in my opinion, the selloff is reasonable and will likely not result in a quick rebound.

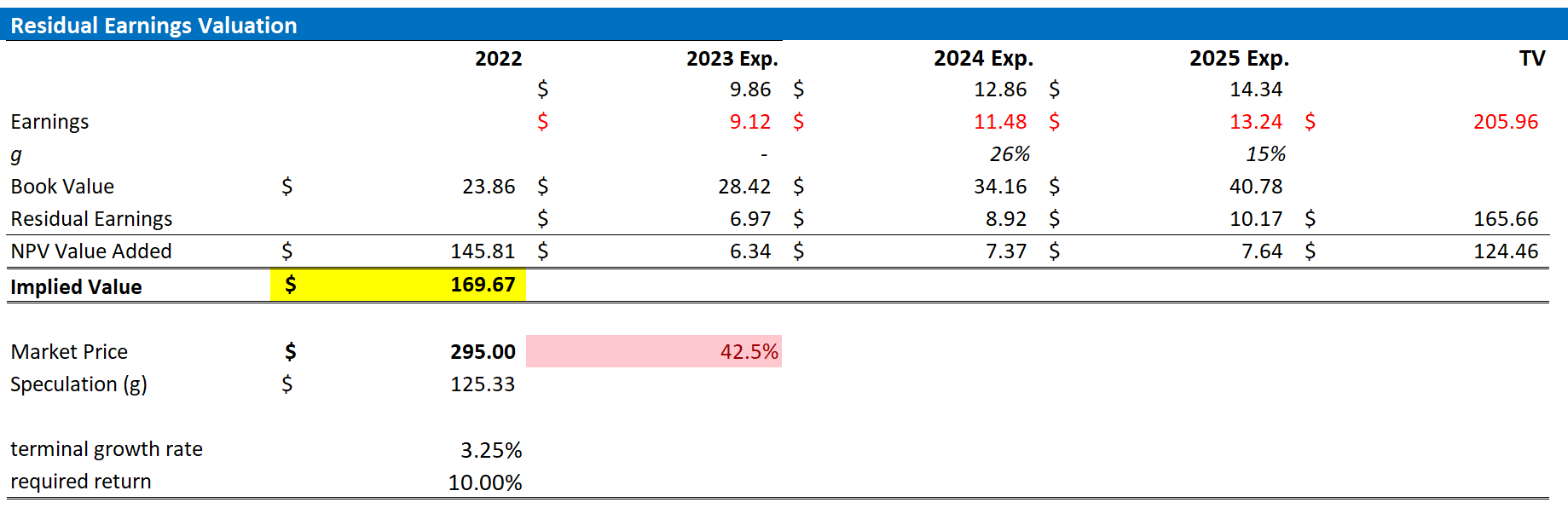

In context of a rich valuation – a FWD EV/EBIT of x24 – I remain unconvinced that LULU stock is a “Buy,” or even a “Hold.” In fact, reflecting on the margin compression, I lower my EPS outlook for Lululemon through 2025 and now calculate a fair implied share price of $169.67.

For reference, LULU stock is now a relative underperformer. Accounting for the latest selloff, LULU stock is down approximately 21% for the trailing twelve months, as compared to a loss of only 17% for the S&P 500 (SP500).

Seeking Alpha

Profit Warning Points To Margin Pressures

On January 9th pre-market, Lululemon issued a press release that can be defined as a profit warning. The athletic apparel company said that gross margin for the December quarter are likely to be between 90 and 110 basis points lower than in the same period of 2021. Without a doubt, this update is a strong disappointment for investors who trusted Lululemon’s previous expectation of a 20 to 30 basis point gross margin expansion.

On a more positive note, Lululemon also updated revenue expectations: as compared to the company’s previous guidance range of $2.605 billion to $2.655 billion, management now thinks that sales for the Holiday quarter will fall between $2.660 billion to $2.700 billion – a performance that would represent a 25% to 27% year-over-year growth as compared to the fourth quarter of fiscal 2021.

But the profitability headwind outweighs the sales expansion. And thus, as a consequence of the lower than expected profitability, LULU management reduced Q4 2022 EPS expectations down to between $4.22 and $4.27, as compared to the company’s previous guidance range of $4.20 to $4.30.

Poised For Lower EPS Consensus Expectations

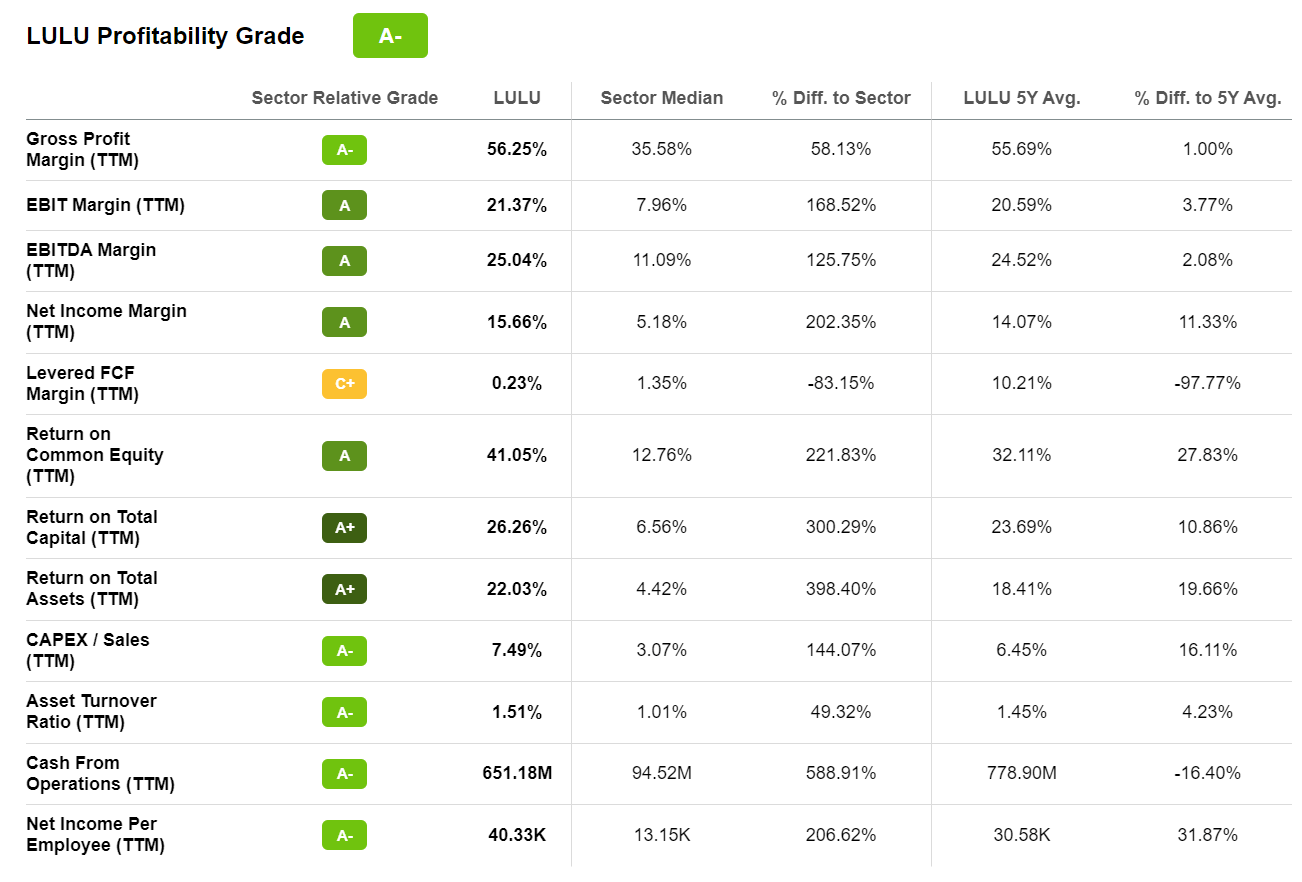

Strong profitability has likely been a key argument why investors have liked investing in LULU. Notably, Lululemon’s TTM gross profit margin is 56.25% and the TTM EBIT margin is 21.37%. According to data compiled by Seeking Alpha, these margins represent a premium to the relevant sector median of approximately 58% and 169%, respectively.

Seeking Alpha

Although, Lululemon’s strong brand equity will likely protect the company from a sharp profitability compression, it is highly likely that Lululemon’s rich margins will come down to some extend and trend closer to the industry norm.

However, analyst consensus EPS estimates must still adjust to reflect the profitability compression. In fact, current EPS estimates for 2023 and 2024 imply that Lululemon’s net profit margin expands to approximately 16.3% and 18.7% respectively. These numbers will likely need to come down, I argue.

Seeking Alpha

For reference, if we assume that the 100 to 130 basis point margin compression is structural, then Lululemon’s earnings for 2023 will likely need to be reduced by $105 – $135 million. Accordingly, earnings for 2024 will likely drop by $119 and $155 million. To put the magnitude of the profitability loss in perspective, an investor may apply LULU’s current P/E TTM multiple to the earnings loss and calculate that the impact on equity is likely to be close to $5 billion, which is about 12% of the company’s market capitalization.

Valuation Update: Lower TP

On the backdrop of a softer than expected profitability outlook, I lower my EPS expectations for LULU in 2023. I estimate that LULU’s EPS in 2023 will likely expand to somewhere between $8.9 and $9.3. Moreover, I also raise my EPS expectations for 2024 and 2025, to $11.48 and 13.24, respectively.

I continue to anchor on a 3.25% terminal growth rate (one percentage point higher than estimated nominal global GDP growth) and a 10% cost of equity requirement.

Given the EPS upgrades as highlighted below, I now calculate a fair implied share price for LULU of $169.67 as compared to $238.31 prior.

Author’s Estimates; Author’s Calculation

Below is also the updated sensitivity table.

Author’s Estimates; Author’s Calculation

Risks To My Bearish Thesis

Lululemon owns a strong brand – with global recognition. Thus, the company may indeed be able to defend abnormally high profit margins given the extra pricing power. Moreover, with year-over-year revenue growth rates of almost 30%, it is not unlikely that Lululemon will grow into its rich valuation within a reasonable period of time.

Conclusion

I like the Lululemon Athletica Inc. brand, and I strongly believe that the company can continue to grow, take market share and accumulate value. However, I argue that at EV/EBIT of x24, markets are pricing an excessive level of optimism. The vulnerabilities of this optimism have been highlighted today, as a profitability disappointment prompted a 10% selloff.

Reflecting on the margin compression, I lower my EPS outlook for Lululemon Athletica Inc. through 2025 and now calculate a fair implied share price of $169.67.

Be the first to comment