hapabapa/iStock Editorial via Getty Images

Despite US markets having a bad day on Monday, one stock bucking the trend was Redbox Entertainment (NASDAQ:RDBX). The video kiosk operator seems to be rallying as the next major hit in the meme stock craziness. However, there are multiple reasons to be very negative on the stock, which we believe could lead to almost 100% downside under multiple scenarios.

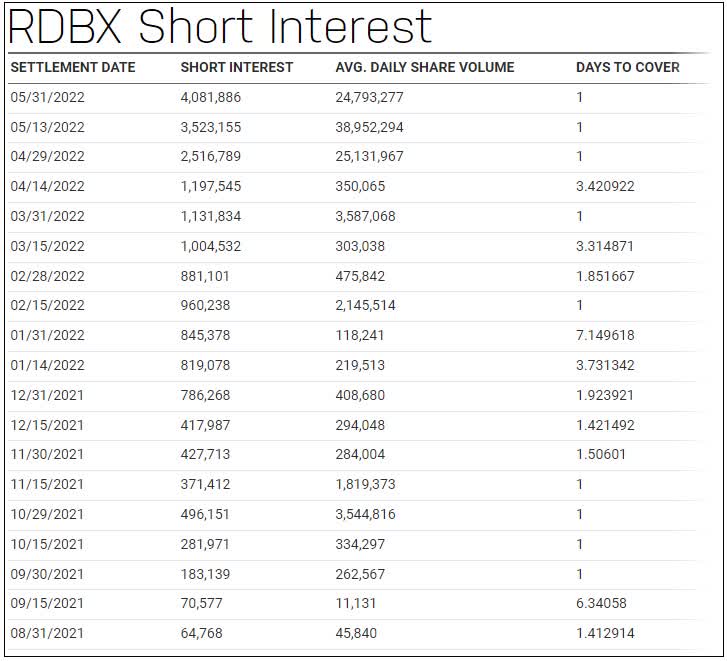

Shares closed Friday at $13.20, but rallied $5 to more than $18 before pulling back a bit on Monday. It appears to be a move based on a short squeeze, with the stock having made the rounds on Reddit among the WallStreetBets crowd. As the graphic below shows, short interest in the name has soared throughout 2022 so far, with more than 37.5% of the float short at the end of May according to Morningstar data.

Redbox Short Interest (NASDAQ)

One of the main reasons why short interest has been surging this year is that the company has agreed to merge with Chicken Soup for the Soul Entertainment (CSSE). Normally, investors might think that’s a good thing, as most of the time it means they can sell shares to another party at a higher price. However, that is definitely not the case here. As the article linked above details, Redbox’s pending deal is worth a significantly lower price than shares currently trade for in the market:

Pursuant to the all-stock deal, Redbox stockholders will receive a fixed exchange ratio of 0.087 of a share of CSSE class A common stock per Redbox share.

But CSSE is down 2.2% Monday to $8.57; its share price implies acquiring Redbox for about 75 cents a share.

There probably are a lot of merger arbitrage folks here shorting the name at these levels in the teens, hoping that the stock eventually falls to the less than dollar per share implied deal price. Maybe a revised deal happens at some point, but even if it comes at say triple the current share exchange rate, that’s only a bit over $2 per share. However, even if the deal does not go through, this is not a business that’s in good shape currently. Take a look at the key financials table below.

Redbox Key Financials (Company Filings)

Movie rentals were a great business a decade ago, when it was the bulk of business for a name like Netflix (NFLX). Since then however, Netflix has pivoted to streaming, and the likes of Amazon (AMZN), Apple (AAPL), and others have poured billions into new and old content. Every month that goes by just adds more consumers to the overall streaming space, with the number of people out there relying on DVD and Blu-Ray disc rentals heading lower.

If the large losses and cash burn weren’t enough to get you worried, perhaps the balance sheet at Redbox will. According to the most recent 10-Q filing, total assets were a little more than $361 million as of March 31st. However, just over 70% of that was actually in either the goodwill or intangible asset categories. The company reported cash of less than $14 million, while total debt was almost $343 million. As the financial situation continues to weaken and global interest rates rise, borrowing costs will only increase, further hurting the bottom line and cash flow situation. Bankruptcy may be an option in the long run if the merger doesn’t go through.

In the end, investors in Redbox Entertainment should use rallies like the one seen on Monday to sell the stock. The company is currently under a merger agreement that values the stock at less than $1 per share, implying massive downside from here. Even if the deal doesn’t go through, however, this is a business showing huge revenue declines, large losses, and significant cash burn. Redbox may be a favorite of the Reddit crowd currently, but like AMC (AMC), GameStop (GME), and others before it, shares will likely return to a more appropriate valuation that’s well below where we are today.

Be the first to comment