RISK OF RECESSION IN 2020 EXACERBATED BY CRUDE OIL PRICE CRASH & CREDIT CRUNCH AS CORONAVIRUS CONCERNS BUILD

- Recession risk could be ratcheting even higher after the price of crude oil crashed over 20% in a single day

- Odds of a recession this year have likely risen again amid another spike in credit default risk on high-yield corporate bonds

- The novel coronavirus outbreak has wreaked havoc on the global supply chain and contributed to a contraction in US business activity

What Markets are Rising as the Dow Jones and Oil Collapse?

Panic-struck stock market investors seem to have taken notice of the rising likelihood that we are going into a recession in the not-too-distant future. A staggering selloff across global equities over recent weeks, driven initially by expected economic fallout from the coronavirus, has gained pace after the latest destabilizing black-swan event: a crash in crude oil prices.

RECESSION RISK BACK ON THE RISE – PROBABILITY OF US RECESSION PREDICTED BY TREASURY YIELD CURVE SPREAD

{kind=link}

According to the Federal Reserve, the probability of a US recession occurring over the next 12-months, as predicted by the Treasury yield curve spread, was clocked at 31% on February 28. Although distressed credit markets caught a breather following an emergency Fed rate cut last week, its first since the global financial crisis and collapse of Lehman Brothers, the 10-year and three-month interest rate spread (3m10s) on US Treasuries took a 20-basis point tumble in response to the latest crude oil price crash.

US TREASURY YIELD CURVE HEADED BACK TOWARD INVERSION TERRITORY ON TEN-YEAR LESS THREE-MONTH SPREAD

Chart created by @RichDvorakFX with TradingView

The 3m10s US Treasury yield curve spread now stands at a positive 18-bps, but this popular recession gauge appears to be headed back toward inversion territory. This might follow rising default risk on high-yield US corporate debt, which presents contagion risk to the broader financial system and economy.

Why Does the US Yield Curve Inversion Matter?

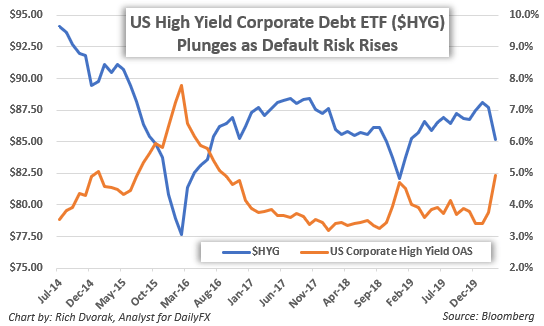

CRUDE OIL PRICE CRASH ADDS TO STRAIN ON CREDIT MARKETS & RAISES DEFAULT RISKFOR HIGH-YIELD CORPORATE DEBT

In fact, the options-adjusted spread (OAS)above the risk-free rate of return for high-yield corporate debt exploded higher to 5.5 percentage points as of March 06 – prior to the 30% gap lower in crude oil just witnessed. With crude now trading around $30.00/bbl, far below the approximate $50.00/bbl break-even price for US shale oil producers, fund outflows have soared from the iShares High Yield Corporate Bond ETF (Ticker symbol: HYG), which has over 10% of its market value exposed to poor credit quality energy companies.

Recommended by Rich Dvorak

Uncover our Top Trading Opportunities for 2020

Likewise, countries heavily dependent on oil exports like Canada or Mexico have seen their currencies plummet relative to safe-haven currencies like the US Dollar and Japanese Yen. At the same time, the broader US Dollar Index (Ticker symbol: DXY), which is heavily weighted to EUR/USD performance, has cratered to an 18-month low as the Euro gains ground against the Greenback.

Recommended by Rich Dvorak

Forex for Beginners

Selling pressure in the USD was sparked amid rekindled recession odds following the IHS Markit PMI report for February that detailed a contraction in US business activity, and notably the services sector, to a 76-month low. As such, it seems likely that recession risk has intensified alongside growing coronavirus concerns and adverse effects from a crash in crude oil.

Keep Reading: Gold Nears Record High as Yields Collapse & Volatility Rages

— Written by Rich Dvorak, Junior Analyst for DailyFX.com

Connect with @RichDvorakFX on Twitter for real-time market insight

Be the first to comment