Richard Drury/DigitalVision via Getty Images

The idea of rebalancing your portfolio has been around for decades. It comes in two basic forms:

- Choosing the best performing stocks with the best diversification, called the “efficient frontier.”

- Keeping the same stocks but changing their size so your portfolio continues to have the same original risk.

The questions we need to ask are “How often should you rebalance?” and “How should you do it?” Some say to rebalance monthly, others quarterly. Does any of this improve your profits or reduce your risk?

What the Academics Say

Although I have worked with stock portfolios for many years, I reviewed the latest “scholarly” and “practitioner” articles about rebalancing. The best explanation was on Investopedia.com (search “Types of Rebalancing Strategies”):

Portfolio rebalancing is intended to reflect an investor’s risk preference. There are three types of rebalancing: calendar, percentage-of-portfolio, and constant-proportion portfolio insurance. To bring you up to speed, the following is a summary:

Calendar rebalancing

Typically, rebalancing is done monthly or quarterly to avoid “portfolio drift,” where the current risk or exposure of your portfolio is significantly different from your intended risk. The frequency of rebalancing can be a combination of time, cost, and drift. Researchers at Vanguard (as noted in Wikipedia) found no significant difference between rebalancing done monthly, annually, or not at all.

Does that seem strange? If I bought stocks in the year 2000 and still held them without rebalancing, I would think that the risk would be far different now than in 2000. But then, why would you still be holding the same stocks? What if one no longer traded?

Percentage-of-Portfolio Rebalancing

This is essentially sector, or asset class, rebalancing. Instead of balancing each stock, the method looks to balance the sectors risk. Rebalancing can include volatility adjustments to keep the more volatile sectors from overwhelming the returns, either positively or negatively. Rebalancing can also include correlations between sectors. This sounds like “portfolio optimization,” but using different words.

Constant Proportion Portfolio Insurance

As returns increase, so does risk tolerance. This simply maintains a constant cash reserve, a percentage of your total funds available for trading. For example, if you started with 80% in stocks and 20% in cash, ($80K and $20K) and stocks gained 20%, you would have $96K in stocks and $20K in cash, a total value of $116K. 80% of that is $92.80. You need to reduce your exposure by $3,200 and move that to cash. If the value of your portfolio declines to $60K you would have a total of $80K. 80% of $80K that is $64K, so you would need to move $4,000 from cash to your trading. You always restore the 80-20 relationship when you rebalance.

What They Have in Common

These methods essentially take from the good and give to the bad. They are effectively selling winners and increasing positions in losers. There is no discussion that rebalancing improves returns. It only rebalances the risk so you might continue to lose money at the same rate or make money at a slower rate.

In our current bear market, you might have all losing positions. Even then, your risk, based on current volatility, might be smaller than your initial risk. You will need to add to your positions. Where would you get the money? Why would you do that?

The Elephant in the Room

What is the elephant in the room? Returns. None of these methods address stock selection or whether your portfolio is making or losing money. If we want portfolio risk management, we need to discuss stocks that are losing money.

I can’t tell you which stocks to buy, but I can tell you that a stock that is going down is not a good choice. Advisors tell you to buy a stock with good “value,” or one with large cash reserves, low debt, good management, or a good price/earnings ratio. Most do not suggest a stock because it is going up. It’s too simple. You can do that yourself. And there is a cost to rebalancing.

High Volatility Versus Low Volatility

The idea of rebalancing based on volatility is good. When a stock is very volatile the risk is usually higher than the reward. When the volatility is low, your risk is low, but your returns are also low. Too low.

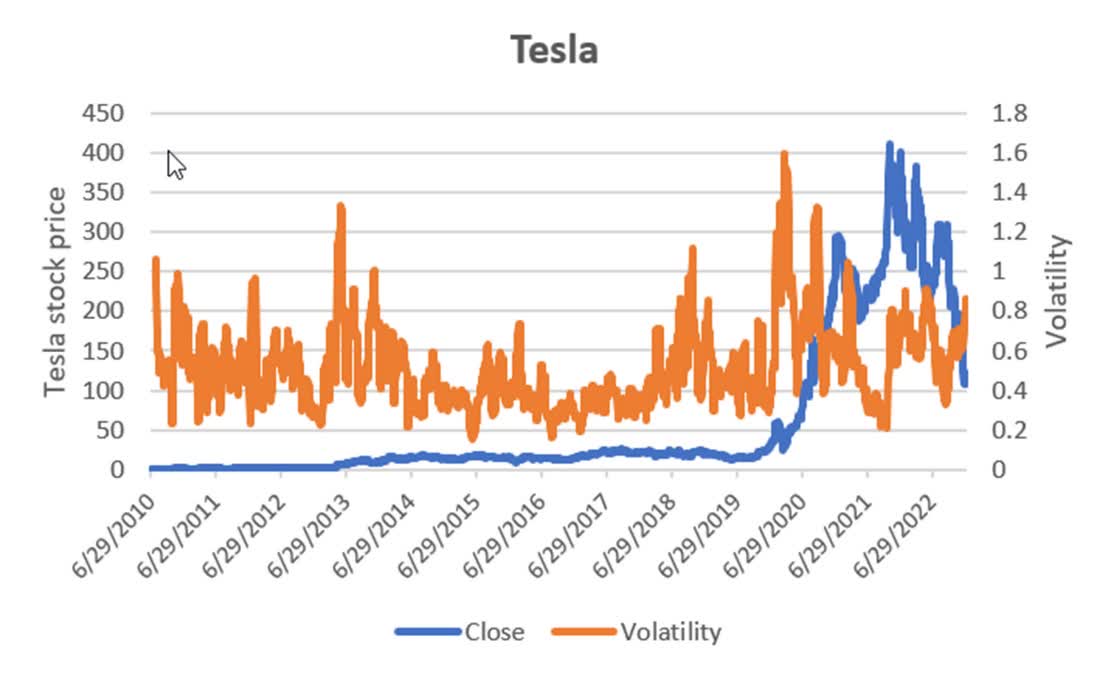

High volatility in individual stocks is different from portfolio volatility. Chart 1 shows that Tesla (TSLA) can often reach a 20-day annualized volatility of 100%. The daily price moves can be very large.

Chart 1. Tesla share price and volatility

Data source: CSI

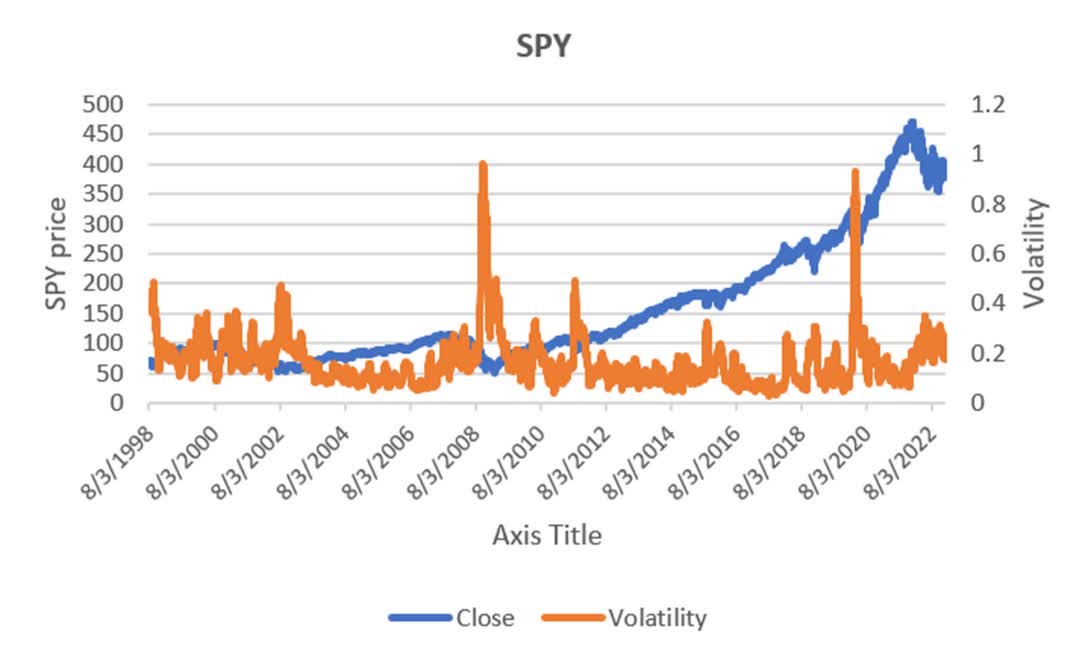

If we look at the ETF SPY (Chart 2), which has the diversification of 500 stocks, we see that the volatility is much lower. The average TSLA volatility was 52% while the SPY volatility averaged 17%. Typically, the volatility index, VIX, based on the S&P, is considered extreme at 30%. I have found that same number true for a typical diversified portfolio.

Chart 2. SPY price and volatility

Data source:CSI

Some forms of rebalancing would not apply if all stocks increased volatility at the same rate, yet your risk would be very high. Risk-adjusted rebalancing, to bring your portfolio down to your volatility risk target, is the best choice. Unfortunately, this doesn’t work when volatility is low unless you have set aside reserves. Low volatility is often the case with trending markets, so being able to restore your risk level should lead to better returns.

Doubling Down on a Losing Stock Makes No Sense

What if you have a J.C. Penney, Bed Bath & Beyond (BBBY), even Tesla or Bitcoin (BTC-USD)? Yes, you can make a lot of money if you keep buying lower prices, and if don’t go broke first. It’s a high-risk strategy that you should avoid.

There is a certain amount of “persistence” in stock moves. They most often continue to move in one direction, sometimes higher, sometimes lower. That’s what we call “trends.” Buying when the trend is up has been a successful strategy for funds for many decades.

Here’s What I Do

Stock prices tend to jump around so judging performance by their recent returns is not the best way of assessing what to buy. Using a simple moving average of the stock works much better. It smooths out the price moves, making it easier to see what is doing best.

I use a combination of trends and breakouts to decide the strength of a stock, but any long-term moving average will work. Try 100 days. Then look at the returns of the past 3 months based on that moving average. Every trading platform provides moving average indicators and may also give you the periodic returns using a trend.

Don’t optimize the moving averages. Use the same one for all stocks. It gives you a better comparison, avoids overfitting, and adds to the robustness of your choices.

Some Simple Rules to Follow

These are rules that I would follow. I cannot know your finances or your risk tolerance, so you will need to apply these rules in the best way that satisfies your goals.

- Let the profitable stocks be profitable. Don’t reduce their size just because they have made money. Base your risk measure on your entire portfolio. There is always an exception. You can reduce the exposure in any stock with volatility over 50%.

- The best returns come when volatility is low and the market is trending. You may need to have reserves to restore your risk to the original target. That will be easy to do with futures, but you need to plan ahead to do that with stocks.

- Don’t rebalance a losing stock. Remove it. Is that so bad? During this bear market you may end up with only a few stocks, or none. You can be earning interest on your cash. That seems like a good plan.

- Scale down your total portfolio, or exit everything, when your portfolio volatility exceeds 30%. Reenter when if falls back below 30%. You might want to have a small buffer, exiting at 32% and reentering at 28%, but I have not had a problem of jumping in and out.

Be the first to comment