peepo

By Antoine Bouvet, Benjamin Schroeder, Padhraic Garvey, CFA

Expect volatile markets in the run-up to central bank meetings

The closer markets get to this week’s central bank events, the more unpredictable day-to-day price movements will get. That said, we stick to our view that the next couple of days are likely to be dominated by profit-taking on longs and, in the case of euro markets, by the realisation that pricing rate cuts in 2024 is premature. However, 5Y swaps, the sector of the curve most at risk in case of a hawkish push back from the European Central Bank, has already moved 30bp higher since its mid-January low. We think higher euro rates and yields are the right macro move, but the scope for more movement before the ECB meeting is now reduced.

One potential driver of short-term rate moves is today’s long list of economic releases (see events section below). A surprise jump in core Spanish inflation has proved a warning shot to investors too complacent in their view that inflation is on the decline. The magnitude of the sell-off means that it would take at least as large an upside surprise in the French inflation release today to push rates much higher. This is not excluded, however, and the eurozone-wide print tomorrow will feature an estimated German component, as the national statistics office has delayed its own inflation report until the end of the month.

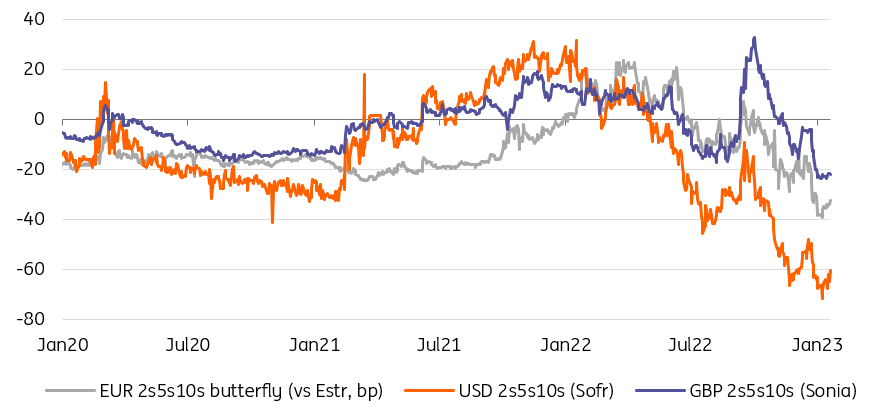

2s5s10s Butterflies Show Curves Geared Towards Rate Cuts, Prematurely In The Case Of The Euro Curve (Refinitiv, ING)

ECB tightening is working its way through, but euro-dollar rates differentials should shrink

So far, so hawkish for the European Central Bank, but investors might find solace in the fact that policy tightening already implemented is working its way through the economy. If the ECB lending survey confirms the picture painted by December credit growth numbers, it will at least reassure the governing council on that front. This is also an important piece of the jigsaw for central bankers and investors trying to anticipate the path for core inflation. Lower energy costs have shielded growth from the worst of the energy crisis, but also mean less of a drag on demand and non-energy inflation.

One has to acknowledge that for all the too-optimistic inflation view priced by euro rates, this will most likely affect markets on a relative basis. Our US economics team thinks the Fed is winning its fight against inflation, a slowdown in today’s Employment Cost Index would be a further evidence of this, and the economy is heading into a recession. Although this will likely not be on a linear path, this means dollar rates are right to decline, and we think they should reach a trough of 3% later this year in the case of 10Y Treasuries. As result, one of the most notable trend this and next quarters should be the convergence between euro and dollar rates.

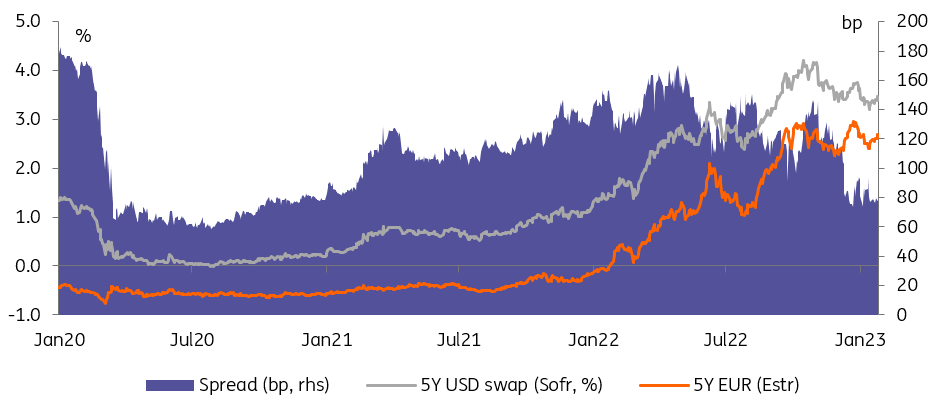

5Y EUR Swaps Are Off Their January Lows But Should Climb Further, Especially Relative To Other Currencies (Refinitiv, ING)

Today’s events and market view

In the run-up to tomorrow’s eurozone-wide HICP (inflation) release, today brings France’s CPI print. Yesterday’s surprise surge in Spanish core inflation proved two things: that markets are leaning towards an inflation view that may be correct for the US but is too dovish for the eurozone. It also proved that releases can be volatile, especially around changes in the weighting of price indices.

Away from inflation, German unemployment data will be closely scrutinised for signs of a turn in a still-tight labour market, and the ECB lending survey will be a key indicator for the central bank to assess how quickly its tighter monetary stance is transmitting to the economy. Finally, we will get a first look at eurozone and Italy fourth-quarter GDP after German and French growth surprised to the downside.

Bond supply will consist of German 2Y and Italian 5Y and 10Y debt.

US releases will be no less relevant for rates markets. The employment cost index for the fourth quarter isn’t a very timely indicator, but it is a well-regarded gauge of underlying wage pressure. One day before the Fed meeting concludes, and at a time its focus is increasingly shifting to non-housing core services, this is an important data point. Consensus is for a slowdown to 1.1% quarterly from 1.2% previously.

Other US release include house price index, Chicago PMI, and conference board consumer confidence. The latter is geared towards the labour market, so any dip in the job-related sub-indices will be another clue about a potential turn in the labour market.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user’s means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Be the first to comment