Sakorn Sukkasemsakorn

In 2023, I am still purchasing the Global X NASDAQ 100 Covered Call ETF (NASDAQ:QYLD) for my income-producing portfolio. QYLD is an income-focused ETF that distributes large amounts of income by selling covered calls against its portfolio, which caps most of the upside potential. Prior to investing in QYLD, define what your investment goals are and conduct a fair amount of due diligence to determine if QYLD meets your needs. For me, QYLD fits into an overall income-producing strategy I have built. I plan on holding my shares of QYLD for decades and reinvesting each distribution to benefit from the powers of compounding. Some people would disagree with this premise, but the fluctuating share price or the upside potential being capped doesn’t concern me. Investing doesn’t have to be an all-or-nothing premise; not every dollar needs to be invested in a maximum-return vehicle. Some investors build hybrid strategies, and my personal strategy has an income component. I recognize the limitations of QYLD and accept that it will not generate comparable capital appreciation to an index fund. The capital I am putting to work in QYLD I am never planning on pulling out unless my investment thesis changes, and I will continue to compound the distributions into an ever-growing income stream.

My mindset on QYLD as an investment

Every day, when you log into your brokerage account, you see an account value. Individual positions fluctuate, and at any given moment, an investment can be in the black or in the red. When you own a business, you don’t have the value of the business flashing in front of you each day; all that matters is the net profit and cash being distributed to your pocket. Everyone’s definition of a good investment is an opinion that can vary from person to person. Hypothetically, picture investing $25,000 into a business just over 9 years ago. Over this period, it generated $21,440 in personal income and was projected to generate $2,150 throughout 2023. Someone contacted you and offered you $16,999 for this business today. Would it be a good investment? This answer will be different for each person, but for me, I would consider this a good investment because I still own the income-producing asset, and if I sell, I generated 85.76% of my initial investment in distributed income over this period, and the combination of income and the sale would net me 53.72%. If I didn’t sell, I would continue to collect the income, and the price of the asset would fluctuate, but the income would continue to flow into my account, and there could be a chance the asset is worth more in the future.

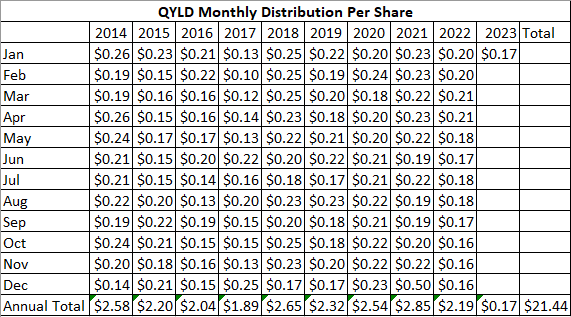

The hypothetical situation I described above is based on looking at and treating QYLD as a business. QYLD’s inception date was 12/11/13, and it hit the market at $25 per share. If you review QYLD’s distribution history, which can be found on the Global X site (click here), you will see that since its inception, QYLD has generated $21.44 of dividend income. QYLD has never missed a monthly payment over the previous 109 months and solidified an impressive track record that validates its income generation method in my opinion. Below is a chart I constructed based on the monthly dividends.

Steven Fiorillo, Global X

Hypothetically, if you had purchased 1,000 shares of QYLD at inception, it would have been a $25,000 investment. If you had taken the dividends as cash, QYLD would have paid $21,440 in dividends, which is 85.76% of the initial investment. You could sell the investment right now for $16,999, which would be $38,430 in total investment value. When the initial $25,000 is deducted, you would be left with a profit of $13,430 or 53.72%. Over the past 9 years, the average annual income has been $2.36 per share, which means that this investment would have generated, on average, $2,363.26 per year. The past is not a guaranteed indication of what will occur in the future, but if QYLD did continue to average $2,363.26 per year in income, you would generate another $21,269.35 in income over the next 9 years. Even if shares went to $14 and your initial base was worth $14,000 in 9 years, you would have collected $42,538.71 in total income over the 18-year period.

If your objective is allocating capital to generate income, in my opinion, this would be a strong investment. The biggest thing with QYLD is recognizing it for what it is, an income-generating machine. There has been a minimal period since its inception where QYLD has exceeded its inception price of $25, but that doesn’t mean it can’t fulfill its main objective of generating income and becoming a net positive investment over time.

Dividend Channel

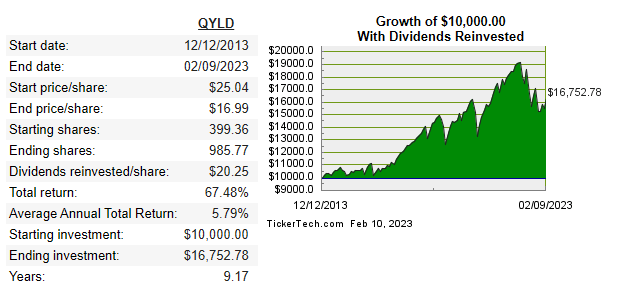

My examples were if you had taken the dividends as cash instead of reinvesting them. What would have occurred if you had reinvested the dividends instead of taking them? Based on a tool that shows the growth of $10,000 with dividends being reinvested, the initial investment of $10,000 would have purchased 399.36 shares. Over the years, reinvesting the dividends would have increased the share base by 586.41 shares for a total of 985.77 shares. Today, the total investment would be worth $16,752.78 for a total return of 67.48%. While an average rate of return of 5.79% over 9.17 years is significantly under the average yield of an S&P index fund, look at how the projected annual income going forward would have changed. The average annual dividend per share over the past 9 years for QYLD has been $2.36. The projected income on the initial batch of 399.36 shares would have been $942.50. Today the 985.77 shares would be projected to produce $2,326 of annual dividend income as the additional 586.41 shares collected added $1,384 in annual projected dividend income. If you wanted to, you could sell off your initial investment of $10,000 today, which would be 588.58 shares and still be left with 397.2 shares producing $937.40 in projected annual income. You could also continue benefiting from the powers of compounding by reinvesting the dividends and growing your annualized stream of income.

Conclusion

I would speculate that many investors who dislike QYLD base their opinion on capital erosion. QYLD needs to be looked through a different lens and accepted for what it is, a covered call fund that may never trade above $25 but generates large amounts of continuous income, in my opinion. On the income side of my portfolio, I am completely content with allocating capital with the premise of never touching it. QYLD has delivered 109 months of continuous dividends and has established a track record I am comfortable with. I would have been content with the results over the previous 9 years, regardless if I took the income as cash along the way or reinvested the dividends. Since QYLD is predicated on selling covered calls, this is a strategy that can work indefinitely, and it has already proven itself throughout difficult economic conditions. I plan on adding to my position, reinvesting the dividends, and compounding my way into a gigantic stream of income down the road. This strategy may not be right for everyone, and it is one portion of my overall investment mix. I personally want a stream of income offsetting or paying for my lifestyle in the future prior to drawing down on any assets in retirement.

Be the first to comment