Just_Super

Recommendation

Investing in QuantumScape (NYSE:QS) is difficult because the entire investment case hinges on whether QS can execute as promised, which can only be validated after several years. To achieve a larger margin of safety (from a business standpoint), my advice is to keep a level head until we have hard evidence that the road to commercialization is clear. As a result, this post will focus on long-term trends, recent updates, and valuation rather than technical granularities, which readers can learn more about in the S-1.

Overall, despite my optimism about the battery industry’s long-term viability and QS’s position as the industry leader in solid-state battery R&D, I am concerned about the company’s slow pace of product development. Although the company claims to have a narrow margin for error in meeting its year-end target, a delay in the A-sample could cause the company to miss its first revenue target.

Business

QuantumScape is developing prototypes of sold-state batteries for use in automobiles, and its contributions to the field are widely anticipated to have a significant impact on the evolution of SSB technology worldwide.

Trend towards EV

I believe the transition away from internal combustion engine (ICE) vehicles is gaining momentum around the world thanks to supportive government incentives and regulations. Concerns about the environment and public health have been exacerbated by the widespread use of gasoline-powered ICE vehicles. AWS encouraging or requiring the use of low- and zero-emission vehicles have been passed by numerous national and regional regulatory bodies.

Moreover, consumers are showing a growing interest in EVs due to their enhanced performance, growing EV charging network, reduced adverse impact to the environment, and reduced total cost of ownership. For instance, Tesla, Inc. (TSLA) has shown that electric vehicles can be a viable alternative to conventional gasoline and diesel vehicles. I think EVs will increasingly gain share from ICE vehicles as they grow more competitive and reasonably priced. I anticipate this trend appearing across all categories of automobiles and markets. However, EV competitiveness and cost reductions remain stunted by the limitations of lithium-ion battery technology.

Solid-state lithium-metal battery is the way to go

In my opinion, a lithium-metal anode is the approach to overcoming the limitations of traditional batteries and facilitating considerable advancements in energy density.

Without getting too technical, in short, according to the S-1 description, a lithium-metal battery anode is made of metallic lithium; there is no host material. With the host material gone, the battery cell is smaller, lighter, and cheaper to produce. Because of this, lithium-metal batteries may be able to pack a lot more power into a given size. In addition, lithium-metal anodes may make way for the next generation of higher energy cathodes, that might not be capable of achieving huge improvements in energy density when used in conjunction with lithium-ion anodes.

Also, charging times are cut down drastically when solid-state batteries are used. In my opinion, potential EV drivers still worry about charging times, and shorter charging times could increase EV adoption. QS claims that its lithium-metal solid-state batteries can be charged from empty to 80 percent capacity in just 15 minutes, which is a significant improvement over the standard charge time for lithium-ion batteries, according to the prospectus.

The latest engineering update from QS reveals that the company has made significant improvements to their films, including the elimination of contaminants and the introduction of new procedures that should improve their performance. This is great as the team can now concentrate on constructing 24-layer test cells after finalizing the design of the films and cells. Samples will be put through a multi-stage production and data-gathering campaign before being sent out to customers. It’s worth noting that QS recognizes there is little wiggle room if they are to achieve their objectives. The goal for the end of the year is significant, and it will be important to keep this in mind, as it will affect how quickly the product can be brought to market.

Partnership with Volkswagen

QS has been working with Volkswagen (OTCPK:VWAGY), a global automotive giant, since 2012. QS and Volkswagen have worked together to set up an industrial-scale production line for solid-state batteries used in Volkswagen vehicles.

Personally, I think this is a really smart move for QS. For one thing, they’ve got a guaranteed buyer for their products, which means they’ll know when they can expect to get paid as long as they follow through with their end of the deal. And if they need to, they can use Volkswagen’s expertise to help them out.

QS growth runway could be further extended by partnering with other OEMs

While I anticipate Volkswagen to be the first automaker to commercialize QS battery-equipped vehicles, I think QS should keep working with other automakers to spread the use of solid-state battery cells. Its joint venture agreement specifies that the QS-1 facility will be the first commercial-scale factory to produce its automotive-grade battery technology. However, QS may also seek out partnerships with other automobile ODMs in order to bring its technology to market.

I see the value in QS collaborating with other OEMs because it broadens the company’s potential market beyond automobiles and reduces the risk associated with taking the company commercial.

Scorpion Capital short report

Basically, this short seller called Scorpion Capital put out a report questioning QuantumScape’s technical abilities. QuantumScape’s management has since tried to address some of the concerns raised in the report and shared more information about their technology. The thing is, QuantumScape’s whole business is riding on the success of this solid-state battery they’re working on, which is kind of a make-or-break situation. Because of this, I expect them to continue being a target for short sellers. And until they finally deliver this solid-state battery, the share price could be all over the place. QuantumScape has been pretty open about things and I do give QS the benefit of doubt that they are not lying since Volkswagen’s name is also on the line.

Valuation & model

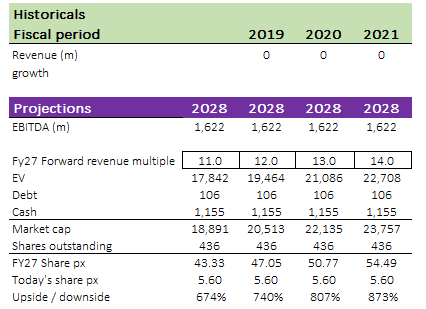

My model is built based on management’s FY28 projections. Assuming QS is able to deliver as promised in FY28, it should generate $1.6 billion in EBITDA. The question is what multiple should QS trade at that point, which I expect to be in the range of low-teens, using the current Tesla forward EBITDA valuation as a ceiling.

The truth is any reasonable multiple will suggest a significant upside for QS as the stock does not seem to be pricing QS to deliver as promised. I would say a severe discount is warranted given the long time to market and significant execution risk that is visible today. That said, if an investor has patience and QS delivers as promised, the upside could be significant.

Author’s own calculations

Risks

Execution

The primary concern is whether or not QS will be able to achieve the desired battery specifications. The company’s leadership is confident that their solid-state battery will be a significant improvement over the lithium-ion batteries currently available. The stock price may be negatively affected if the company is unable to achieve these goals.

In addition, QS may face significant delays in the production of its solid-state battery cells, which could impede its ability to bring to market any products it decides to develop on time, if at all. The stock price would likely drop as a result.

Relationship with Volkswagen

QS’s business and long-term prospects are vulnerable due to the risks inherent in its partnership with Volkswagen. QS’s joint development partnership with Volkswagen does not guarantee that the company will be able to bring solid-state batteries to market.

Competition

QS faces competition from companies that were once its customers because some of those businesses may decide to set up their own battery production facilities. Moreover, it appears that the number of new businesses operating in the area of solid-state batteries is on the rise. QS could face risk in meeting its projections, which would have an effect on the stock, if its competitors succeed in producing a commercially viable solid-state battery before QS.

Summary

I have faith in the battery industry’s long-term viability, and I think QS is at the forefront of solid-state battery R&D, but I am concerned about the company’s lack of forward momentum in bringing its products to market. A delay in the A-sample could delay the date when they start making money, and they have said they don’t have much wiggle room in meeting their end-of-year goal.

Be the first to comment