HT Ganzo/iStock via Getty Images

Investment Thesis

Plug Power (NASDAQ:PLUG), is a publicly-traded company that designs and manufactures hydrogen fuel cell systems for use in a variety of applications, including material handling equipment, forklifts, and airport ground support vehicles. The company’s technology is aimed at providing a clean, efficient, and reliable source of power for commercial and industrial customers.

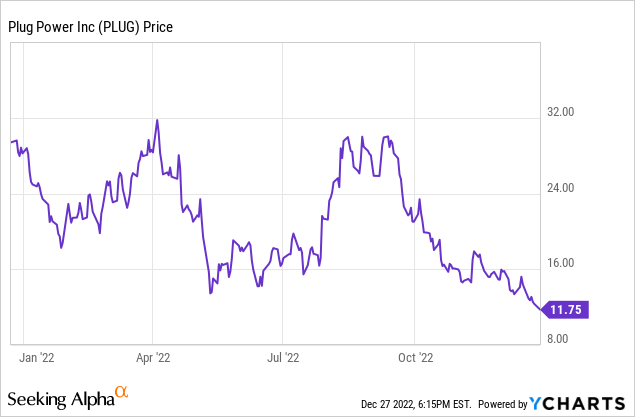

When it comes to the company’s stock performance, it has experienced many intense fluctuations during the past year going from around $30 to $12, back to $30, and then back to $12 again, where it is currently trading at. This has made many investors wonder if it is going to bounce back to $30 once again, yielding them an almost 250% return.

PLUG’s Financials

Seeking Alpha

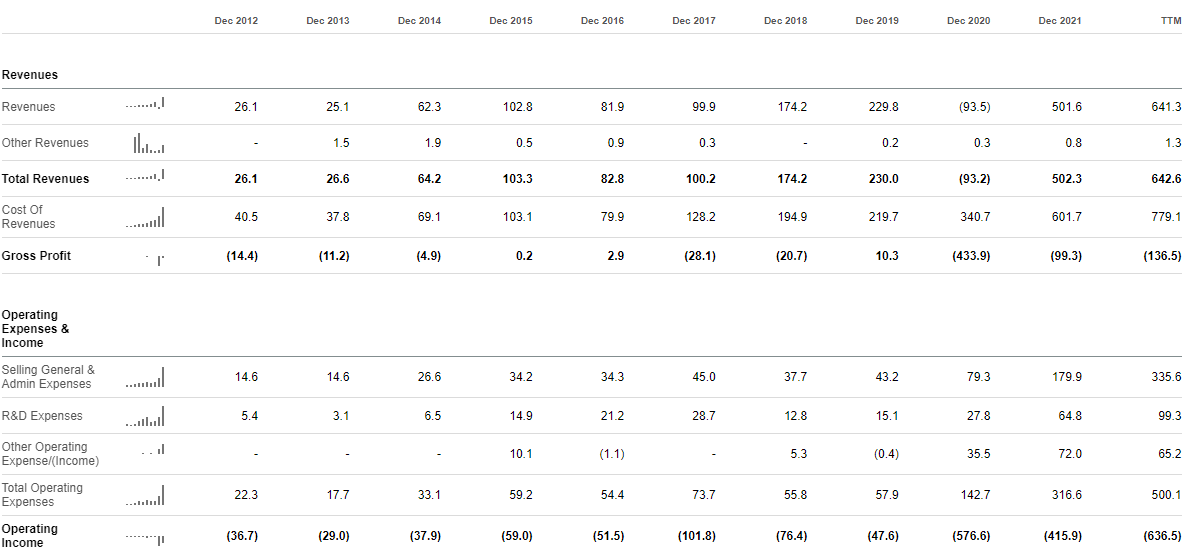

Looking at Plug Power’s income statement, we can see that the company has experienced significant revenue growth in recent years, with revenues increasing from $100 million in 2017 to $641 million in the TTM of 2022. However, the company has also reported net losses in each of these years, with a net loss of $136.5 million this year.

Seeking Alpha

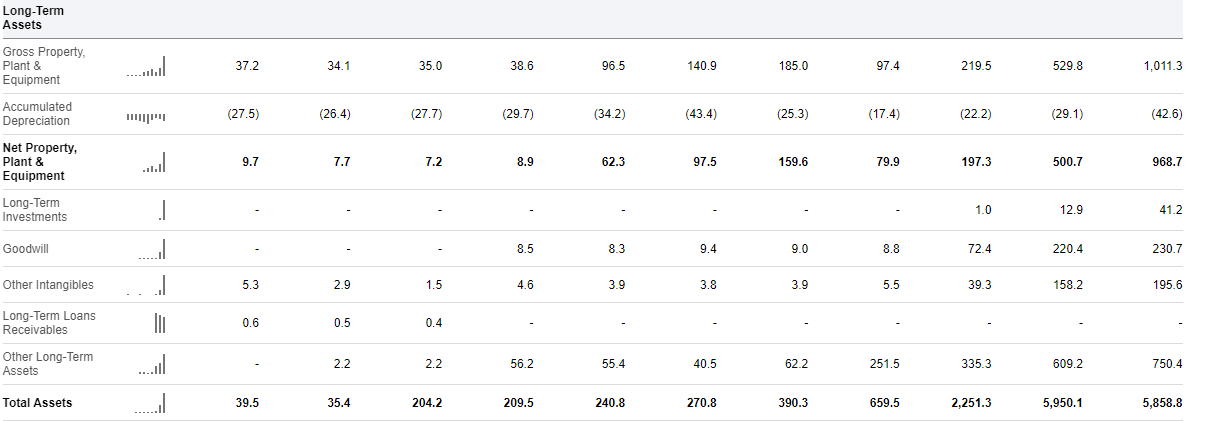

Examining Plug Power’s balance sheet, we can see that the company has a relatively high level of debt, with total liabilities of $1.635 billion as of Q3, 2022. This is more than offset by the company’s total assets of $5.858 billion and shareholder equity of $4.223 billion.

Seeking Alpha

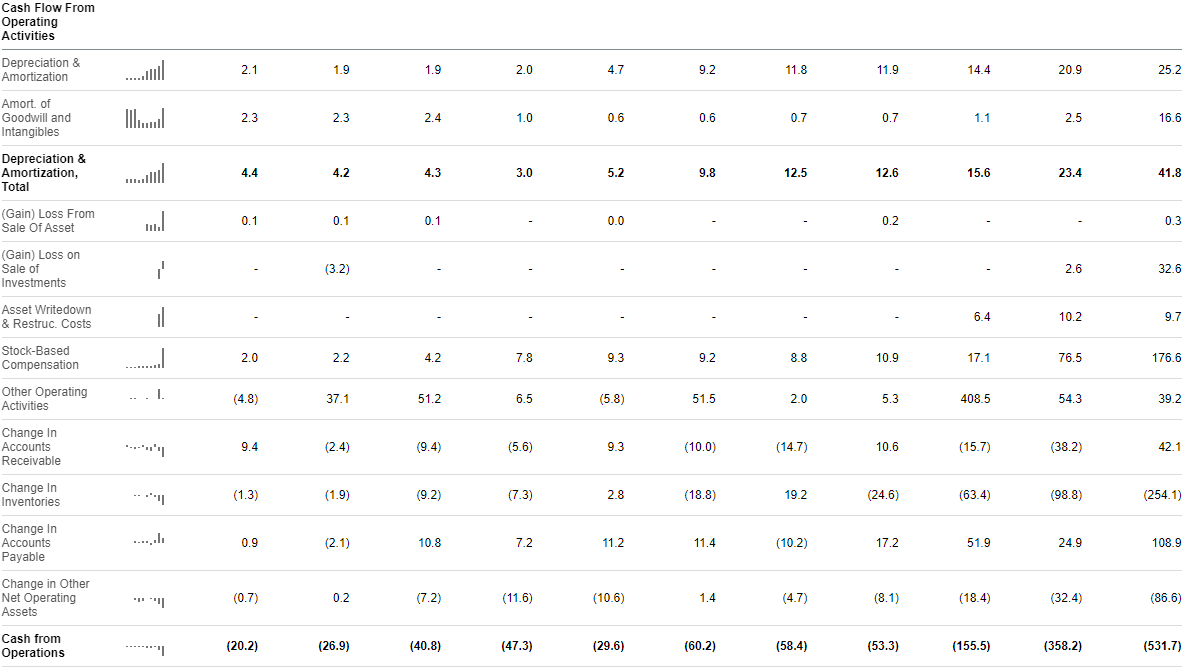

Lastly, reviewing Plug Power’s cash flow statement, we can see that the company had an operating cash outflow of $531.7 million in 2022, primarily due to investing activities such as capital expenditures and acquisitions. The company also had a net cash outflow from financing activities, primarily due to the repayment of debt.

Overall, Plug Power’s financial statements suggest that the company is experiencing strong revenue growth but has yet to consistently turn a profit. The company’s high level of debt and net cash outflow from investing and financing activities are also potential concerns for investors.

Future

There are a number of factors that could impact the future of the company’s stock, including demand for hydrogen fuel cell technology, the competitive landscape, the company’s financial performance, and other market conditions.

One factor to consider is the demand for hydrogen fuel cell technology. Plug Power is a leader in this industry, and the increasing demand for clean energy solutions, particularly in the transportation and logistics sectors, could drive further growth for the company and potentially lead to an increase in the stock price. On the other hand, if demand for hydrogen fuel cell technology decreases or the competitive landscape becomes more challenging, it could negatively impact the company’s stock price.

It is also important to consider the company’s financial performance. If the company is able to consistently turn a profit and generate strong cash flow, it could be seen as a more attractive investment and potentially lead to an increase in the stock price. On the other hand, if the company continues to report losses or experiences financial difficulties, it could negatively impact the stock price. At the end of the day, revenue without profit is useless and according to analysts, the company is going to stay unprofitable for at least the next two years.

Company’s Focus On Material-Handling Equipment

plugpower.com

One aspect of Plug Power’s business that may not be well-known to many investors is the company’s focus on hydrogen fuel cell technology for material handling equipment and forklifts. While hydrogen fuel cells are often associated with transportation applications, such as cars and buses, Plug Power has built a significant portion of its business around providing fuel cell systems for material handling equipment in warehouses and distribution centers.

In recent years, the company has signed a number of significant contracts with major customers, including Amazon (AMZN) and Walmart (WMT), to provide fuel cell systems for their fleets of material handling equipment. This has contributed to the company’s strong revenue growth in recent years and could be a key driver of future growth.

Another aspect of Plug Power’s business that may not be well-known to many investors is the company’s focus on the development of hydrogen infrastructure. In addition to providing fuel cell systems, the company is also working on developing hydrogen fueling stations and other infrastructure to support the growth of hydrogen fuel cell technology. This includes the previous 9 partnerships with companies like Air Liquide and Linde to develop and operate hydrogen fueling stations.

Overall, while Plug Power is well known in the hydrogen fuel cell industry, some investors may not be aware of the company’s focus on material handling equipment and the development of hydrogen infrastructure. These aspects of the company’s business could be important drivers of future growth and could be worth considering for investors.

Risks

As with any investment, there are risks and challenges to consider when buying Plug Power stock.

Plug Power has a history of losses and has yet to consistently turn a profit, which could be a concern for investors. This suggests that the company may not be generating enough revenue or may be incurring too many expenses to be financially viable in the long term. It is important for investors to carefully consider the company’s financial performance when evaluating its potential as an investment.

Also, the hydrogen fuel cell industry is highly competitive, with major players like Toyota and Ballard Power Systems vying for market share. This could make it difficult for Plug Power to sustain its growth and maintain its market position. Investors should consider the competitive landscape when evaluating the company’s future prospects.

Another important issue is the company’s debt. Plug Power has a relatively high level of debt, with total liabilities of $1.635 billion as of Q3, 2022. This could be a risk for investors, as the company may need to devote a significant portion of its future earnings to debt repayment.

Lastly, it is important to mention that the adoption of hydrogen fuel cell technology is still in the early stages and could be impacted by a variety of factors, such as the availability of alternative technologies, changes in government regulations, and shifts in consumer preferences. This could present challenges for Plug Power’s growth and profitability.

Conclusion

Overall, Plug Power appears to be a risky but potentially lucrative investment opportunity. The company’s strong growth and expanding customer base suggest that demand for its products will continue to grow. However, the company’s history of losses and the competitive nature of the industry make it a risky choice for some investors. Personally, although I would rather wait for the company to become profitable and then reevaluate it, I can understand that many investors might see a clearer path to profitability for the company and therefore are willing to take the risk right now and start a position. For me, right now, Plug Power falls into the hold area.

Be the first to comment