KanawatTH/iStock via Getty Images

The case for Investment

When investing in a growth stock, an investor is expected to make multiple compromises. Growing losses, increased debt levels, non-existent cash flows, dilutive shareholder actions are some of the most common compromises expected of the investors. How else is a company supposed to grow is the most common way investors rationalize this. But Qualys (NASDAQ:QLYS) stands in contrast to many of the growth stocks seen out there and everything I see in Qualys makes me want to invest in the company. In my write-up below I will attempt to elaborate further on why this is the case.

Company and Macro Take

Qualys is a leading provider of cloud-based IT, security, and compliance solutions. Its platform, Qualys Cloud, offers an integrated suite of solutions that enables customers to efficiently manage their IT assets (endpoints, cloud, containers and mobile environments) and secure their systems from cyber-attacks. Their platform helps organizations to gather and examine a significant volume of IT security information, identify vulnerabilities, prioritize, advise and carry out corrective measures, and achieve compliance with both internal policies and external regulations.

Broadly speaking, Cybersecurity industry has grown greatly since its inception in the late 1980s. It has paralleled the development of computing devices and has been separated into 5 generations. The first two generations focused on securing standalone PCs and protecting businesses in the early internet era, leading to the creation of firewalls. Later generations became more complex with threats exploiting application vulnerabilities and massive, rapidly spreading attacks affecting mobile and cloud environments. Mega attacks have become frequent, causing small businesses to fail and large businesses to suffer major reputation damage and business disruptions. Regardless of economic conditions, cybersecurity is not an area companies typically cut back on.

- Revenue in the Cybersecurity market is projected to reach US$173B in 2023 and expected to have a CAGR of 10.9% till 2027

- There is a significant incentive for companies to protect themselves from a cyberattack and this is not just connected to reputational damage.

- There was a study conducted on how the data breaches affect the stock market share prices. In the long run, firms impacted by breaches underperformed in the market. On average, their share price dropped by 8.6% after one year, lagging behind NASDAQ by 8.6%. Over two years, the average share price decreased by 11.3%, with an 11.9% underperformance compared to NASDAQ. After three years, the average share price decline reached 15.6%, with a 15.6% deficit compared to NASDAQ

-

Below is an insight into the average costs of data breaches that is borne in the event of a cyber attack

|

Average cost for US |

$9.4M |

|

Average cost seen on a Global Level |

$4.3M |

|

Average cost seen for a Healthcare Industry |

$10.1M |

|

Average cost of Ransomware attack |

$4.5M |

|

Average cost of Destructive attack |

$5.1M |

|

Average cost for organizations with Private Cloud |

$4.2M |

|

Average cost for organizations with Public Cloud |

$5M |

Clearly the macro conditions for Cybersecurity have never been better.

Captivating tale of growth

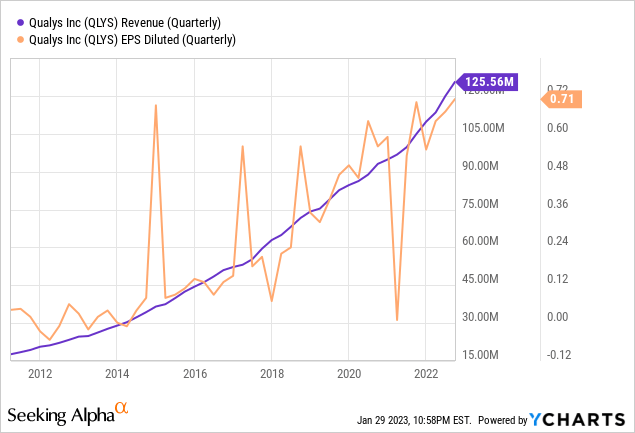

Now let’s dive into Qualys’s growth story and how it looks different from many of the growth stocks. Revenues have been growing at least 10% every year and the best part about the growth is that its profitable! For many growth stocks, profitability is almost non-existent, so this growth story is in sharp contrast. Part of the reason could be that the company was founded more than 20 years ago and has been able to find a firm footing since then.

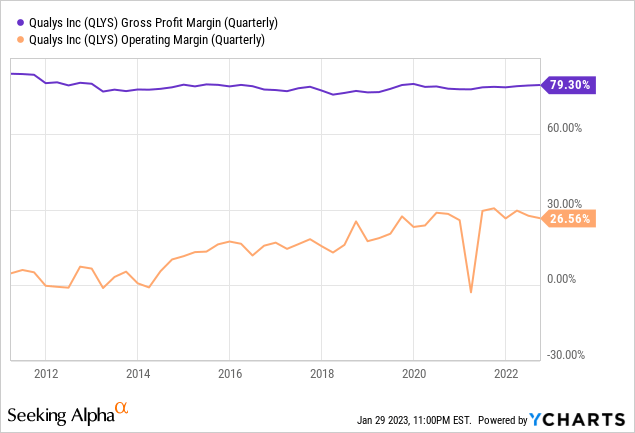

Another reason is that the company has a tight grip on its Gross margins and Operating margins. Gross margin has been consistently above 75% and operation margin has steadily climbed over the years.

Company is also growing its cash flows year after year and the best part about this growth is that you can account for its stock based compensation and its satisfactory. There have been many times where I see that a growth stock utterly fails in this regard and operational cash flow even goes negative when you account for its SBC. As an exercise, I wanted to check how well this looks at least with respect to cyber Security companies and was proven right!

| Symbol | SBC ($M) – TTM | OCF ($M) |

| QLYS | 49 | 195 |

| CRWD | 466 | 827 |

| PANW | 1018 | 2632 |

| RPD | 121 | 43 |

| TENB | 111 | 121 |

| ZS | 424 | 357 |

| S | 144 | -177 |

| FTNT | 215 | 1569 |

| CHKP | 120 | 1203 |

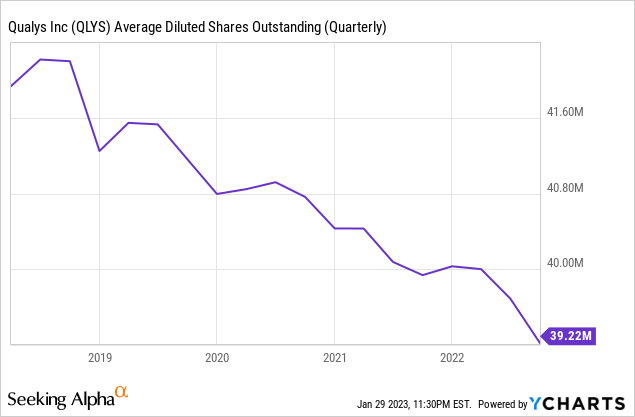

Another test in the same vein is seeing how much of the SBC is affecting the shareholders. Here also the company has a tight grip and any dilution is well addressed through stock buybacks as evidenced below in the last five years.

What about debt? This is another area which can get quite concerning for companies. Debt fueled growth can only be sustainable for so long. But here too we have a winner! The company has no long term debt, its current assets alone cover all of its liabilities and in fact, its cash ($385M) itself covers almost all of its liabilities ($392M)!

Valuation

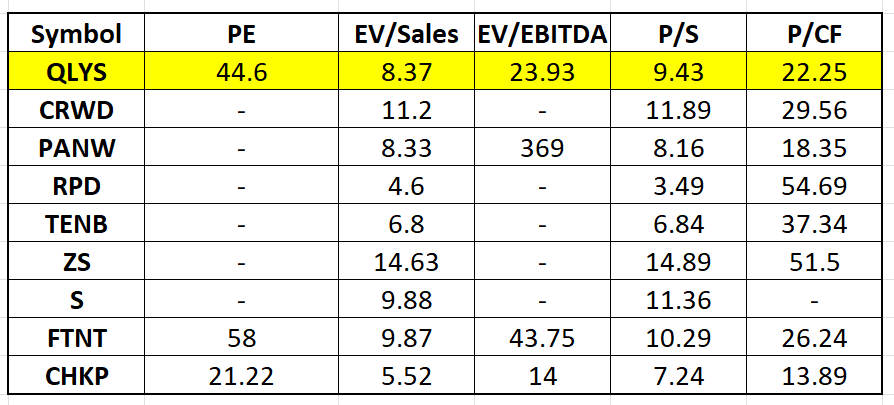

From its most recent 10-K, the company lists multiple public and private firms as its competitors. Let us see how well it fares from the information that is available to us for the public companies (CrowdStrike, Palo Alto Networks, Rapid7, Tenable Holdings, Zscaler, SentinelOne, Fortinet, CheckPoint Software)

Valuation Multiples (Seeking Alpha)

As you can see most of the companies are unprofitable so let us ignore the earnings multiple. Situation gets slightly better on an EV to EBITDA basis and Qualys places second here. On Price to Sales basis, Qualys ranks fifth and when you consider the cash flow multiple it ranks third (and we already saw how well the cash flows are inflated in most instances due to high SBC)

All things considered (including profitability), I would say its valuation looks fair in comparison to its peers (Checkpoint is the only company that places ahead but its growth has slowed down in the recent years). If Qualys can maintain the same level of growth that we saw in the last decade, the stock is a bargain when compared to its peers in the industry.

Action

To summarize, at this moment I will be making Qualys the biggest holding in my growth portfolio for the following reasons –

- Cybersecurity Industry conditions are ripe for continued future growth and Qualys growth tells me that its products are well viewed by the market

- Unlike many growth stocks, its growth is not coming at the cost of profitability, debt or shareholder dilution and it places well among its peers in all the categories

- If one needs exposure to the Cybersecurity industry and is concerned about the valuation of companies, Qualys seems to be a great option

Be the first to comment