Marc Bruxelle/iStock Editorial via Getty Images

Introduction

Caterpillar Inc. (NYSE:CAT) is a Texas-based construction and mining equipment manufacturer that operates globally known for its bright yellow construction vehicles. Caterpillar’s products range from small backhoe loaders to giant mining trucks which serve a critical function in construction and demolition projects.

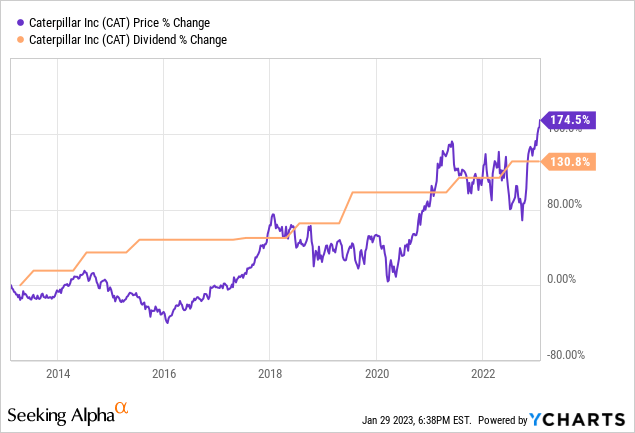

For a relatively boring company, their share price and returns have been anything but!

Despite the cyclical nature of the construction industry, Caterpillar has been a strong compounder, offering shareholders a growing share price and a growing dividend! Over the past decade, if you held CAT, your share price would have nearly tripled, and your dividend would have more than doubled.

Not too shabby…

But the past is the past, and with a potential recession looming, the real question worth asking is if now is still a good time to buy Caterpillar stock.

Within this article I’ll:

- Provide an update on Caterpillar’s performance

- Compare Caterpillar’s financial performance versus its peers

- Provide a price target relative to its future earnings and peers

Caterpillar’s Performance and Future Prospects

Let’s start with this: there may be some challenges ahead for the industry… Given the real chance of a recession companies and governments are likely starting to curtail spending on new investments in infrastructure. Such bearishness is a negative for Caterpillar, which is reliant on infrastructure spending to drive sales for its products.

Further supporting the expectation of a recession is the fact that this recent survey found that nearly all CEOs are expecting some sort of recession in 2023.

As bearish managers expect weak growth in the first half of the year I think it is likely that Caterpillar’s backlog of orders may fall in the short term, which may hurt their performance this quarter.

Because of that, it’ll be important to pay close attention to what management reveals in their first quarterly earnings report of the year, which is expected on 1/31/2023 before the market opens. Guidance will be especially important to pay attention to in order to gain a better understanding of just how much investment may be slowing.

In its last earnings report, it was revealed Caterpillar crushed revenue growth estimates, coming in at 21% revenue growth YoY. It’ll be interesting to see if they can continue to buck the trend and beat growth despite the headwinds.

However, there are some positive indicators that suggest Caterpillar’s prospects may actually improve in the second half of the year.

I believe that the largest headwind facing Caterpillar is the fear of a recession. If recessionary fears can be calmed it may bode well for Caterpillar. One feared driver for this expected recession is the federal reserve and whether or not they will be able to navigate us towards a so-called “soft landing” by taking inflation back down to its historical ~2% range while maintaining strong employment and avoiding a recession.

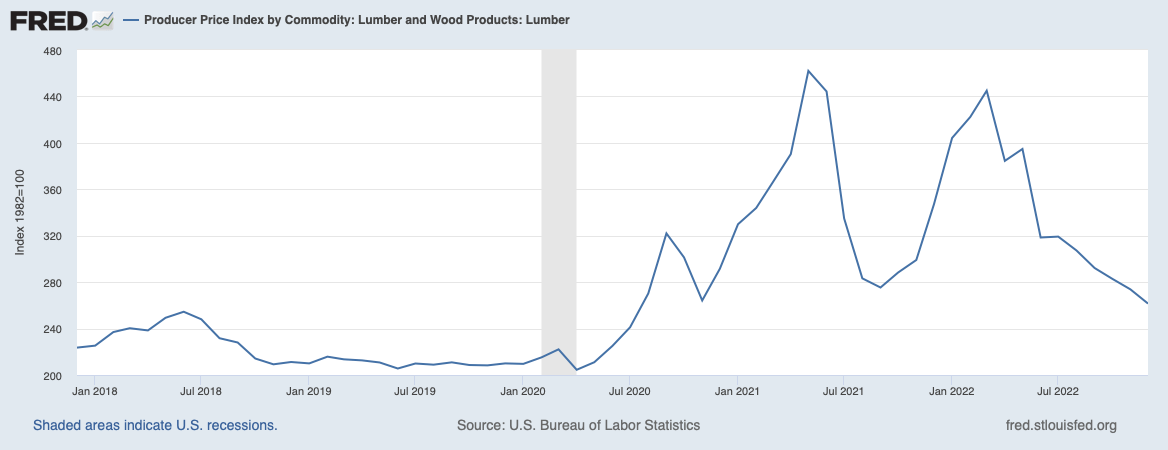

Luckily, signs, thus far, look optimistic. Many laid-off tech workers are quickly finding new jobs, and commodity prices like lumber and steel have begun to stabilize.

FRED

If the US can navigate can nail this “soft landing” it may help ramp up economic (& construction) activity.

If these macroeconomic headwinds ease over the next six to nine months and investors start looking toward a new economic cycle. If everything continues to stabilize, I speculate that we could see orders begin to pick up in Q2/Q3, which could bode very well for Caterpillar.

Additional Growth Opportunities

Caterpillar’s strong presence in emerging markets and exposure to continued infrastructure development projects there position them for significant growth opportunities.

In emerging markets such as those in Africa and Southeast Asia, there is a growing demand for construction and mining equipment, driven by the continued urbanization and development of these countries.

One headwind facing those economies has been the strong US dollar, which, oh by the way, has recently begun a trend of weakening.

US Dollar Index (MarketWatch)

A soft landing should benefit these developing nations as it could dampen the strength of the US dollar which has been buoyed by relatively high-interest rates.

It’s worth noting that a large amount of emerging market debts are denominated in US dollars. Therefore, it stands to reason that less money spent on servicing debt may lead to increased spending on local infrastructure and other local projects.

Financial Performance

Now that we’ve discussed the macro environment let’s take a look at Caterpillar’s financial performance versus some of its peers.

Today I’d like to highlight 3 important metrics: revenue growth, cash flow per share, and returns on invested capital.

Revenue growth shows us if the company is still able to grow the top line, while cash flow per share shows us if that growth is turning into incremental cashflows, and ROIC helps us understand how effective management has been at deploying capital for future growth.

CAT Peers (Seeking Alpha)

For this analysis, I will be comparing Caterpillar against its peers selected by Seeking Alpha: AB Volvo (OTCPK:VLVLY), PACCAR Inc (PCAR), and Cummins (CMI) (I am excluding Daimler Truck Holding AG (OTCPK:DTRUY) and Epiroc AB (OTCPK:EPOKY) due to their shorter trading history on YCharts).

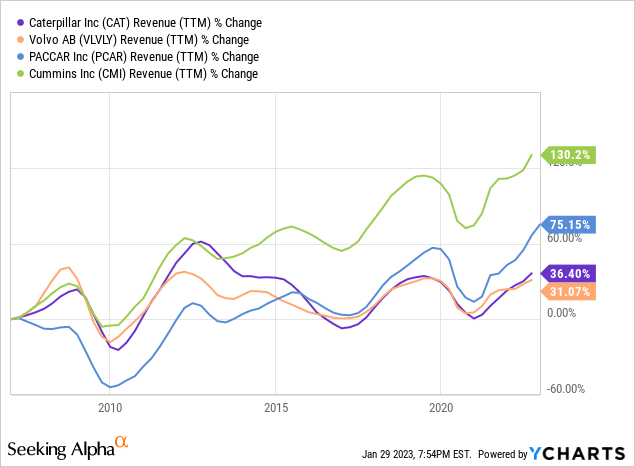

Revenue Growth

Looking first at revenue growth since 2007, we can see that Cummins takes the lead, having grown revenues by 130%. Caterpillar, perhaps due to its large size, was only able to eke out growth of 36.4% during this time period, just slightly better than Volvo.

While positive, this level of revenue growth doesn’t get me excited… For now, let’s shift our perspective to cash flow to see if they can help make up for weak revenue growth with stronger cash flow growth.

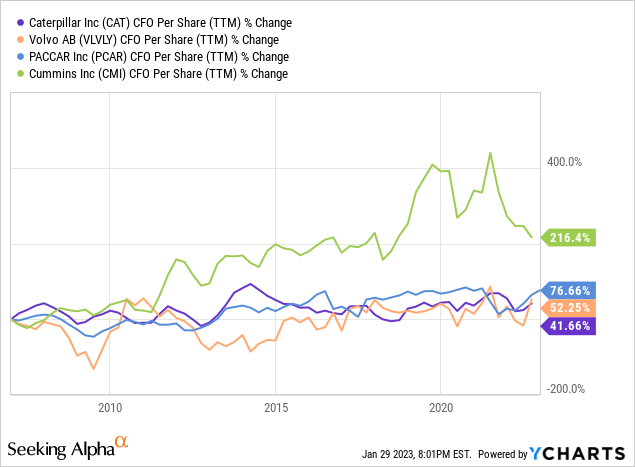

CFO Per Share

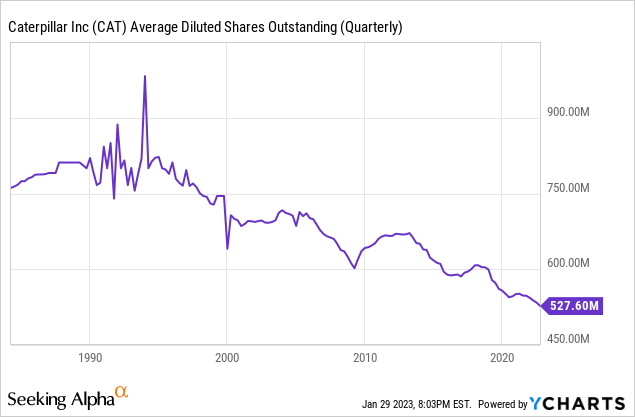

Based on the chart above we can see that Caterpillar has made some progress in growing their CFO per share, growing it by roughly 42% over the same time period where revenues grew 36.4%. Again, not particularly exciting. And what’s more, it looks like much of this growth was driven by buybacks.

Buybacks

Looking at the chart above, it appears that the reason cash flow grew is because of the substantial degree of buybacks that Caterpillar has executed over the past few decades, NOT because the business has become more profitable or cash generative.

I have mixed feelings about this chart, on one hand, it’s nice to see your ownership stake grow in businesses you’re invested in. On the other hand, it signals to me that management may be running out of internal projects for growth.

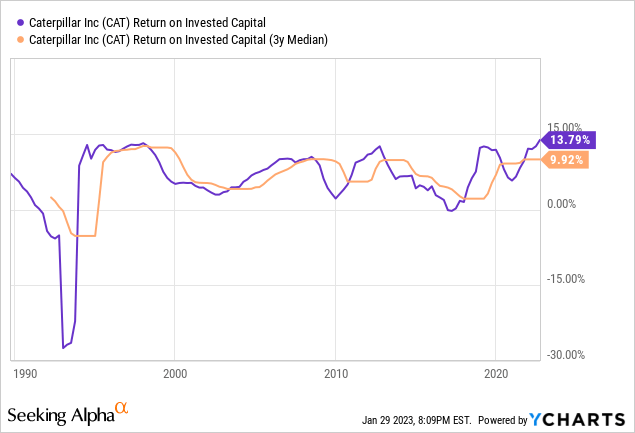

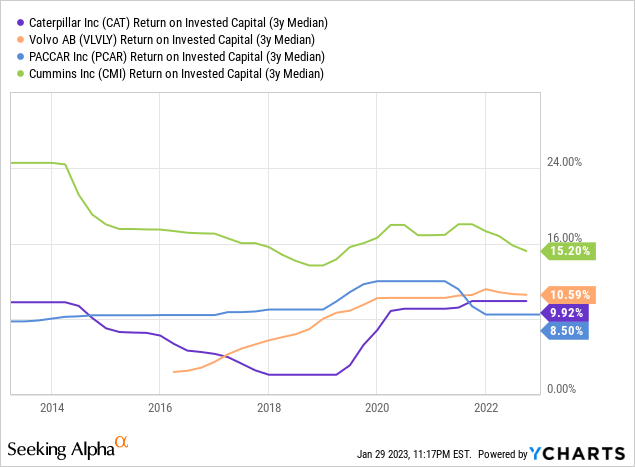

Return on Invested Capital

Finally, let’s look at Returns on Invested Capital. Depending on the cycle, Caterpillar’s returns on invested capital appear to cycle between low single digits and high single digits/low teens most recently coming in at 13.79%. With a long-term average under 10%, I would classify the management as merely average capital allocators.

Compared to its peers, Caterpillar’s ROIC appears to be relatively average. Only Cummins has been able to sustain above-average ROIC, but even they have seen a downward trend over the past few years.

Price Target and Conclusion

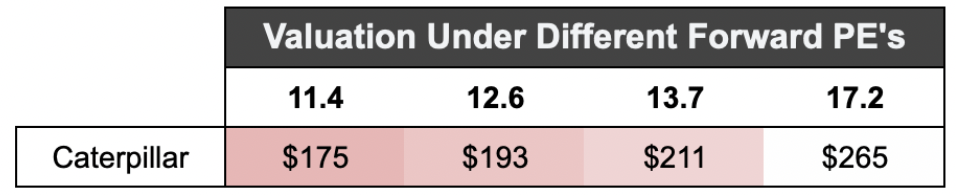

Let’s wrap things up by comparing Caterpillar’s valuation versus its peers and summing things up. For this exercise, I calculated the average analyst expectation for forward earnings and compared it to Caterpillar’s. Interestingly, despite its average financial performance, Caterpillar shares actually trade at a premium compared to their peers.

| Company | Current Stock Price | EPS 2023 Est. | 2023 P/E |

| CAT | $265 | $15.36 | 17.2 |

| VLVLY | $20 | $1.74 | 11.4 |

| PCAR | $111 | $8.05 | 13.7 |

| CMI | $249 | $19.72 | 12.6 |

| Average PE (excl. CAT) | 12.6 |

Caterpillar’s PE of 17.2 is ~37% higher than the average PE for this group (12.6)! This is somewhat puzzling to me as we saw earlier that Caterpillar’s ROIC and revenue growth are relatively in line with peers, if not slightly worse.

Applying Caterpillar’s peers’ PE ratios to Caterpillar earnings implies that shares may be overvalued at 17.2x.

Yahoo Finance Analyst Expectations and Authors Calculations

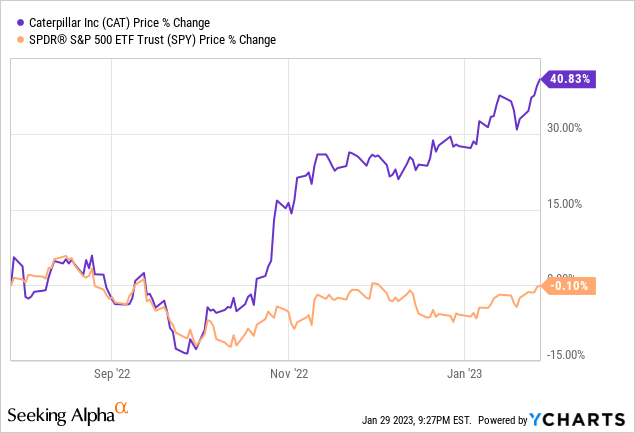

This is somewhat concerning given the huge runup shares have had over the past few months…

Given Caterpillar’s extreme outperformance against the S&P 500, I believe shares may have overheated and could be due for a reset, or at least a rethink.

There is a lot to like about Caterpillar, they have entrenched themselves as a near-necessity within the construction industry and would be a key beneficiary if we witness a soft landing. On the other hand, the valuation is just too high compared to its peers and returns on capital are merely average.

Because of those factors, I rate Caterpillar a Sell, and I am setting my 1-yr price target to $211.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment