B4LLS

Investment Thesis

PubMatic (NASDAQ:PUBM) is a supply-side platform. Companies with digital assets and online content seeking to monetize their inventory adopt PubMatic’s independent platform. A website or app can monetize its ad space through PubMatic’s fully scalable platform.

The issue with PubMatic is that the advertising sector is on its knees. Well, that’s what many investors believe. However, I contend that insight may have been exaggerated.

Indeed, this is my investment thesis, that PUBM’s risk-reward is now more compelling than it seems at first sight. Here’s why.

Left For Dead?

PubMatic has a lot of issues. So, let’s discuss them.

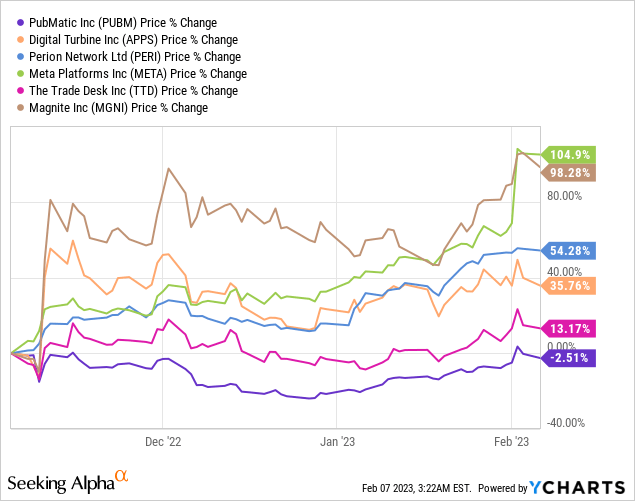

Compared with many of its peers, PubMatic’s share price is the worst performer.

The list above is not an exhaustive list. But it does give one the sense that for all the worries about the economy, it appears that the advertising sector is looking beyond this.

Put simply, I argue that the advertising sector may be showing more promise than many investors are being led to believe, at least on the surface.

Recent results from Meta (META) and Pinterest (PINS) echo my argument. It’s not so much that the results coming out of adtech companies this quarter are any good. I am absolutely not the person to make this claim.

What I am declaring is that there’s an argument to be made to look ahead. We know that the economy is fairing particularly poorly. We also know that interest rates are likely to continue increasing for a while longer.

But what insight has not already been priced into PUBM? That’s my question to readers.

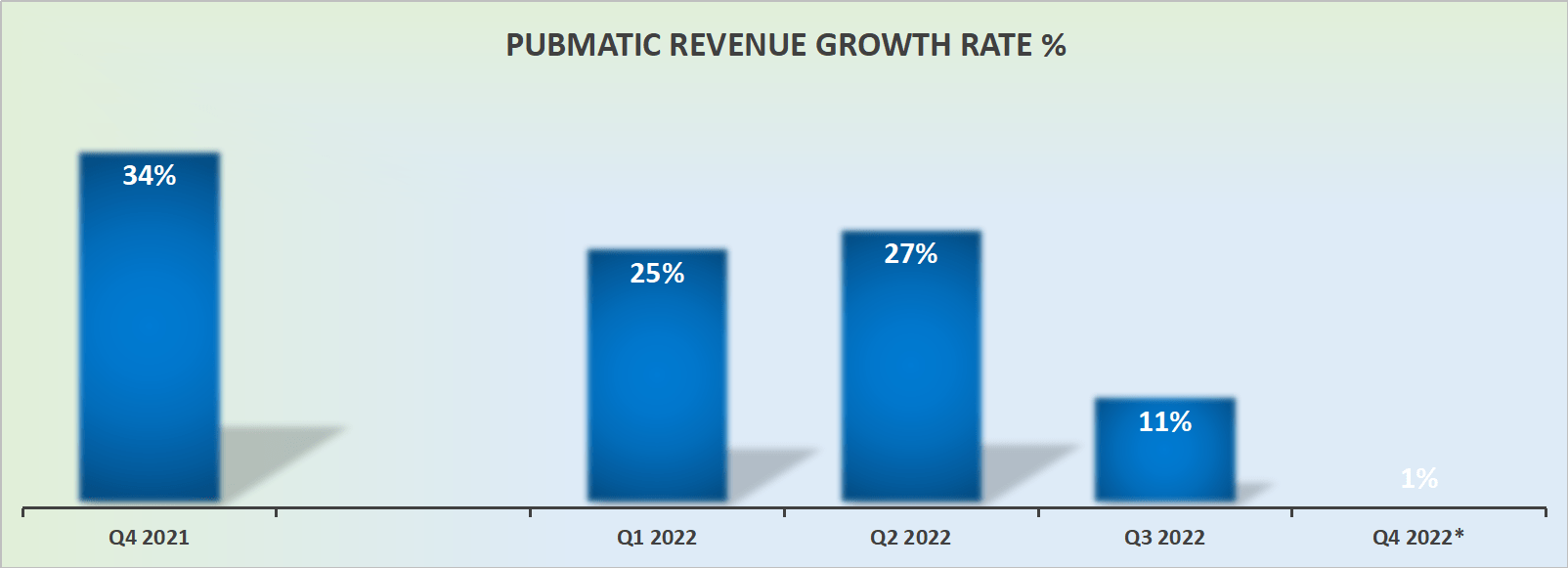

Revenue Growth Rates Died Down

PUBM revenue growth rates

Here’s some more bad news that everyone knows.

When PubMatic guided for Q4 revenues, back in Q3. Everywhere we looked there was plenty of uncertainty everywhere. This saw PUBM guide towards a deceleration in global advertising spend.

Obviously, PubMatic would have guided for Q4 revenues with a margin of safety.

Furthermore, keep in mind, that the need to guide low together with the macro environment at that particular time being painfully unclear, together drove PubMatic to guide for its revenues to be only up 1% y/y in Q4.

But What’s Changed Now?

Habits. Companies have by now steadied their footing. Most companies would have had time to learn to deal with the present environment.

PubMatic’s customers, the advertisers that want to get their message out there to connect with their own potential customers, recognize that to drive customers towards their business they must spend.

Furthermore, one thing is abundantly clear, with PUBM’s stock down more than 70% from its highs, PubMatic has had to revise its operations.

PubMatic will undoubtedly recognize that it must double down on its higher ROE ventures. Particularly in the post-cookie environment, what advertisers crave is control and analytics to measure the success of their advertising campaign.

Consequently, the combination of PubMatic going back to the drawing board and its customers feeling slightly more confident, I believe this bodes well for PubMatic in 2023.

In the next section we’ll turn our focus to discussing PubMatic’s valuation.

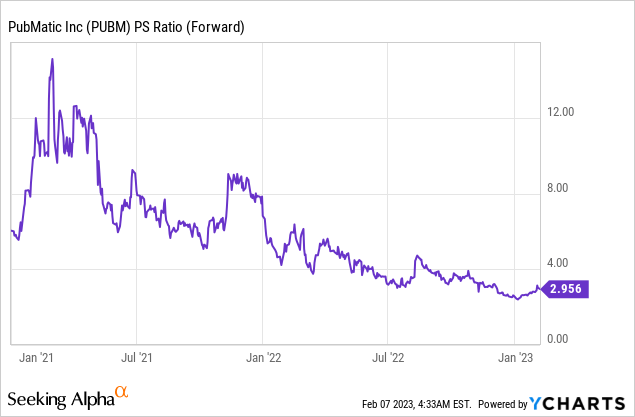

How to Think About PUBM’s Valuation?

Therein lies the critical inquiry.

I recognize that in hindsight it was wrong of me to believe that paying the high multiples PubMatic traded for last year made sense. But that’s done and dusted.

However, this insight doesn’t preclude me from stating that right now enthusiasm for this company has fully washed out. Yes, the outlook is far from great, but isn’t that already factored into its valuation?

Put more simply, hasn’t PubMatic’s valuation multiple already washed out?

The Bottom Line

PubMatic is a free cash flow-producing business with zero debt. Yes, the business has no moat to speak of. And yes, its growth rates are fully compressed. And yes, the very term prospects leave a lot to be desired. And yes, there are much bigger peers with meaningfully more wherewithal.

But I still believe that when everything is said and done, the risk-reward is now more favorable than it has been for a long while.

Be the first to comment