Olivier Le Moal/iStock via Getty Images

Investment Strategy

The portfolios that I own or help to manage have different risk profiles, but I have found that using a covered call strategy can enhance the returns on nearly all of them. I think it is fair to say that most investors do not utilize covered calls, and many of those who do seem to only write them against fairly conservative stocks, often to enhance dividend income. While I do this as well, I also use covered calls to generate income from riskier growth stocks which may not ever pay a dividend. To illustrate, below are some trades I entered into just today and the reasoning I used.

Mainstream Stocks

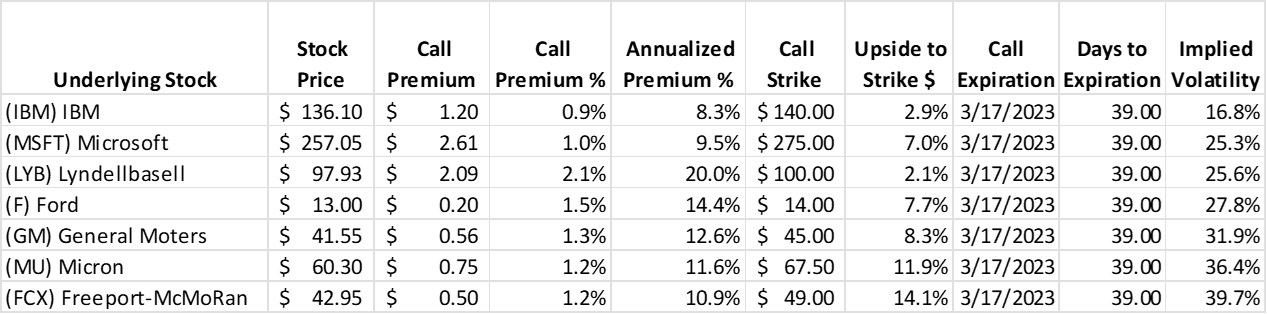

First, I’ll cover the better known stocks I sold calls against today. (These are just some of my “core position” stocks, so please don’t think I am overly concentrated in auto and tech stocks). The seven calls I wrote today were as follow:

Author

As the table shows, these options have just over one month to expiration. For more liquid names such as these, I usually pick the regular monthly expiration dates (as opposed to the weekly expirations) because the options tend to have better liquidity as well. The exception is if my strategy on a particular option is to avoid an anticipated earnings release, ex-dividend date, or other corporate event.

The premiums I collected were between 0.9% and 2.1% of the underlying stock price, which on an annualized basis would net between 8.3% and 20.0% if nothing else changed. All of the strike prices selected also have between 2.1% and 14.1% upside to the strike prices, which is potentially incremental to the option premiums collected and the common stock dividends I can still collect on these stocks. Going down the list, here was my thought process on each stock:

IBM (IBM) has been somewhat rangebound for both the past one and five year periods. They recently reported results with lackluster revenue growth prospects, but they remain a solid company overall. I picked the $140 strike price, which represents a modest 2.9% upside because I don’t see an upside catalyst for the next 39 days that would return it to the pre-earnings level before the next report expected in April. So I’ll take the annualized 8.3% call premium on top of the 4.8% dividend and re-evaluate the position in March.

Microsoft (MSFT) has also reported already, but received a better reception than IBM’s results. The stock has also received some positive sentiment from its investments in ChatGPT developer OpenAI (enthusiasm in the AI space has led to a doubling of C3.ai (AI) stock in the past few trading sessions), but it will still take a lot to move Microsoft’s $1.9 trillion market cap in a significant way in just over a month. The $275 strike price represents a 7% upside, the annualized call premium comes to 9.5%, and there’s a modest 1.05% dividend for my beer money.

LyondellBasell (LYB) is very cyclical and has already enjoyed a 38% run off of its 52 week low. It already reported solid results, but it remains a commodity company. Still, I was able to collect a premium that, annualized, would return 20% on top of the 4.85% dividend yield. The strike upside is only 2.1% higher than the current stock price, but I have over a month to see what develops in the economy that could affect the commodity markets. In a month, I could decide to roll the call options to a higher strike and/or longer duration if the stock continues to move higher.

Ford (F) and GM (GM) are both part of my value portfolio. I don’t consider them exactly equal, but they trade pretty much in tandem over time. I also believe that there is pent-up demand from recent supply shortages that will benefit both companies in a relatively shallow recession scenario (not that I’m predicting anything about the economy). So I opted for similar call options on each at 14.4% and 12.6% annualized premiums on 7.7% and 8.3% upside strikes, respectively. Ford has the higher dividend at 4.54% versus 0.88% at GM, but has not executed as well lately.

Micron (MU) is a commodity producer, but in an industry which has long term secular growth. Call it a cyclical grower, with wide fluctuations in profitability. Having said that, it appears cheap and I like that the industry itself has consolidated and has very large barriers to entry. I was able to collect an annualized 11.6% dividend and not worry about being called away for another 11.9% upside in the stock – again for just 39 more days to go. The 0.74% dividend is not enough to sway my decisions on this one, though.

Freeport-McMoRan (FCX) combines some of the attributes of both LyondellBasell and Micron discussed above. It is a cyclical commodity producer, but it is hard to imagine that there won’t be long term secular growth for copper. Copper prices have recovered nicely, but not to previous highs. Meanwhile, Freeport-McMoRan’s stock has run up nicely, aided by the impressive reduction of $4.5 billion of net debt in the past 3-4 years. After this move from below $25 to $43 today, I was able to collect an annualized 10.9% premium while leaving room for another 14.1% near-term upside for the stock price. Plus a 1.39% dividend.

Slightly Riskier Stocks

Next were a couple of covered calls on what I consider solid, but lesser known and sometimes more volatile names:

Author

Marvell (MRVL) has underperformed the broader semiconductor sector in recent months, which leads me to believe that they might be facing issues of their own. I don’t know if this is true or not, but I was hesitant to wait for earnings in early March to find out. So I wrote the February 24 calls and collected a 25.5% annualized premium with only 18 days to expiration. I still have 10.3% upside to the strike price if there is a runup into earnings. I will have to re-evaluate the position after they report.

Hillman (HLMN) is a smaller company, but an important supplier to the likes of Home Depot (HD) and Lowe’s (LOW) which I have written about in the past. I like the company’s long term outlook and hope to keep it as a core position for many years to come. But because it is little known and thinly traded, I had to go out 165 days to get a decent bid on an upside strike. Still, this gives me an annualized 9.4% premium income and a possible 28.9% upside to the strike. The company is coming out from a period of increased supply chain costs from the pandemic, but should see a lower cost of goods in the second half of 2023.

My Flyer Stocks

Then there are some stocks that haven’t worked well for me (at least not yet!). These are, perhaps not coincidentally, all de-SPACS. At this point, they are such small positions that I view them as options themselves, but I can still get them to pay for themselves through covered calls.

Author

Archer Aviation (ACHR) is one of many eVTOL (electric vertical take-off and landing) companies which went public through the SPAC craze. I liked that they had partnered with United Airlines (UAL) and Stellantis (STLA), which continues to show support for the company. Still, developing, certifying, and manufacturing an eVTOL is a daunting task with many competitors trying different approaches. The call premium gives me 10.1% annualized income while still allowing 71.2% potential upside if they make a significant announcement in the next 74 days. Otherwise, I’ll just sell the next call.

(EQRX) is a biotech startup trying to develop a number of drugs. They have $1.4 billion in net cash and an equity valuation of $1.2 billion. No, I did the math right – they have a negative enterprise valuation! Of course, they will be spending the cash in hopes of developing at least one big drug, which could take years. I view this as an option / lottery ticket stock. Still, I collected 9.8% of the stock price to wait 221 days for a potential 97.6% upside.

Wejo (WEJO) might be the future of big data for automobiles, traffic efficiency, vehicle communications, and insurance. But right now they just need cash to make that long road happen. So 12.7% annualized and I don’t get called away IF the stock goes up by less than 87.4% in less than half a year. Obviously, a long shot.

I like Fisker Inc (FSR) as a dark horse contender. There are as many new EV makers as there are eVTOL entrants, plus Tesla (TSLA) and the legacy car makers with deep pockets, all struggling for future market share. The difference is that FSR is taking an Apple (AAPL) like strategy of designing cars and letting others build them for them. They have begun production of the Ocean compact SUV with Magna (MGA) and are planning to start production of their second vehicle with Apple supplier Hon Hai Precision Industry Co. (OTCPK:HNHPF), a.k.a. Foxconn, by the end of the year. Despite this asset-light operating model, the company is currently under-capitalized. Meanwhile, the financial markets have either been burnt by and/or are shying away from EV startups. Even industry leader Tesla has had a significant reduction in its valuation.

Still, I’m rooting for FSR. I just collected a 33.4% annualized premium and left myself 44.7% potential upside with a call expiring in only 11 days! It is possible that this is because there is some chatter about the company among the meme stock investors lately. If they do push up the price, I would advise management to follow AMC‘s footsteps and sell as much equity as they can.

Takeaways

I have gone over the actual trades that I made today as part of my covered call investing strategy. I wanted to demonstrate in this article that covered call writing can be used to enhance all parts of a well-diversified portfolio, not just conservative dividend stocks.

When I write calls, and when I write about covered calls, I discuss the premiums that I collect and get to keep without any risk – they are immediately credited to my account. I also discuss the relationship of the current stock price, which is a known amount, to the potential future price, which no one in the world knows for certain. I call this the “potential upside to the strike” of the call. There is no guarantee that it will reach or exceed the strike price. That’s why I call it potential upside. Of course, the stock can also go down, but it will do so whether or not you’ve written calls against it.

Please note that I have not mentioned tax consequences in any of these articles. I am not a tax expert. Please consult your own tax adviser, as well as a qualified financial planner or advisor who knows your unique situation and goals.

Be the first to comment