Melena-Nsk

Investment thesis

Timberland and wood production REITs could be a great way to hedge against inflation as the land holdings steadily appreciate over time. However, the appreciation will be likely slower in the next year than the actual CPI numbers and it will only catch up later. PotlatchDeltic Corporation (NASDAQ:PCH) could be one of the choices for timberland REIT investors; however, the next 12-15 months are not going to be easy for the company. I believe that there is a lot of value underneath the surface and over the long term PCH is a good choice but I am currently neutral on the stock. It is because the valuation is fair maybe a bit above fair, I cannot see the shareholder-friendly CAD outcome of the recent merger yet and the external trends are against the company in the short term.

Business Model

PCH is a major timberland real estate investment company that owns more than 1.8 million acres of land at the moment before the completion of the CatchMark Timber Trust Inc. (CTT) acquisition. The company also operates sawmills to capitalize on the higher profit margin of lumber. The company works with great net profit margins which grew in the last 2-3 years. PCH’s revenue comes from 3 major sources. Approximately four-tenths of the company’s income comes from timberland itself, real estate, and land sales but the lion’s share comes from wood products.

The chart is created by the author. All the figures are from the company’s financial statements.

External trends

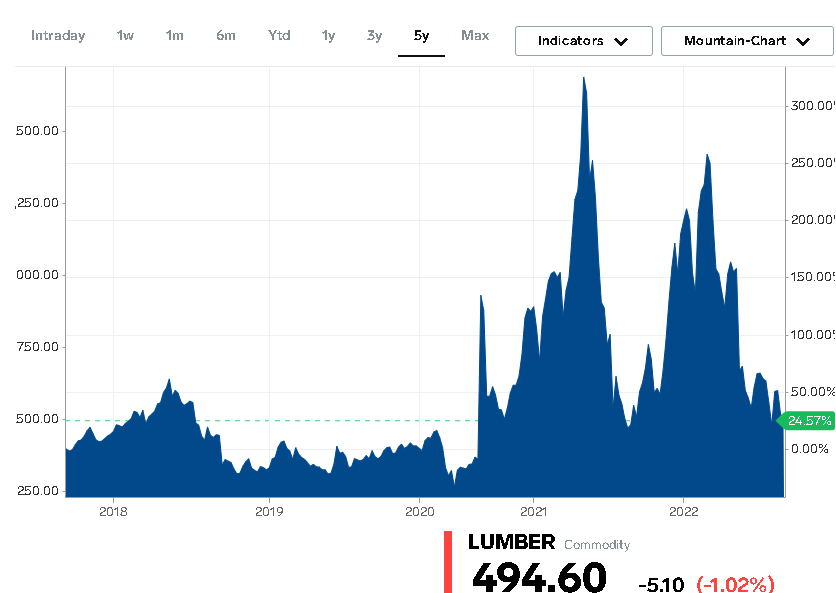

To have a better understanding of PCH and its future we need to have a look at the external timberland and lumber trends. What can we expect in the next 12-15 months? The past 2 years were great for timberland companies especially due to elevated lumber prices and because of high housing demand. The new “normal” won’t be that simple: timber and lumber prices are at 52-week lows and there is a reason behind that. The housing market is gradually slowing down, new construction projects are battling supply chain issues and high labor costs which causes less demand for lumber. This is likely to remain for the rest of 2022 and possibly for the first half of 2023 as well.

markets.businessinsider.com

At the same time, sawmill costs are also rising which will hurt Potlatch’s CAD in the next 12 months. A tight supply of labor and inflation is likely to push labor costs up by 5-10% in 2022 and in addition, energy prices could remain elevated. Power is used to represent 2% of sawmills’ turnover. This could rise by 2%, 3%, or even 5% depending on the deal PCH mills could strike with providers. This means the overall cost structure might change and the energy costs could surpass labor costs. In addition, the elevated costs combined with lower demand and lower lumber prices mean less cash coming into PCH. This situation is combined with a very overvalued acquisition of CatchMark.

This might look scary for PCH investors but the good news is that the company is stable and still a good choice for the longer term. Next year is not going to be great for the company, but after the consolidation of the newly acquired timber company and the renewal demand of the housing market will play in their hand in the long term. Lumber prices might seem low at the moment but investors need to know that these prices are very hectic. It is not uncommon that within 2-3 months’ prices jump or fall by 30-40%. Analysts indicate that lumber prices will be between $550 – $1500 in the next 12 months which is good news for PCH.

Valuation

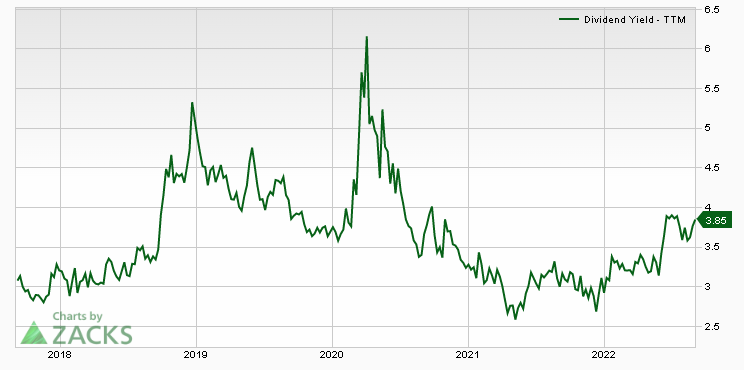

Taking into consideration all of the above-mentioned trends, the CatchMark merger, and PCH’s current valuation we can safely say that the company is anything but cheap despite the -22% drop year-to-date. Short interest of 1.16% went up to almost 5% by the end of August 2022 which suggests large hedge funds also see the risks associated with PCH in the short term. Unfortunately, the dividend yield is not good enough for income investors just yet, but above 4-4.2% I would buy the stock for income purposes. However, PCH still has the highest forward dividend yield among its peers but the valuation is fair or even a bit overvalued at the moment.

Zacks.com

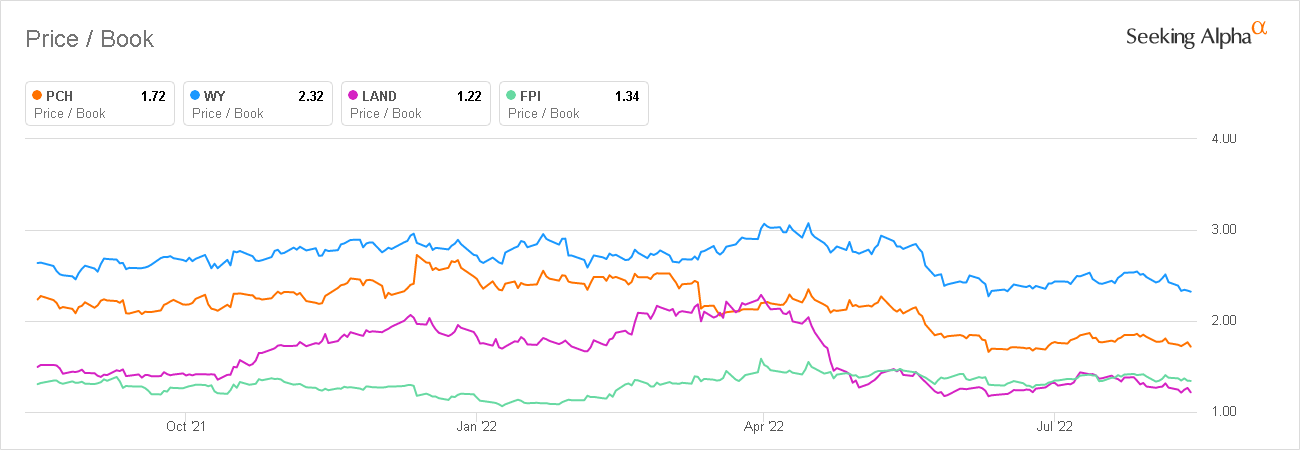

The price-to-book ratio of 1.72x might look very overvalued among REITs but timberland and farmland REITs usually trade well above their book value. Compared to its peers the company is relatively fairly valued but we can only have a vague idea of how this might change after the close of the acquisition by the end of the third quarter.

Seeking Alpha

Company-specific Risks

Surprisingly, I only see one major risk factor for PCH. This is because they cannot change the external trends of timber or lumber prices, and the management cannot change the housing market demand. The only part they can improve or mess up is the consolidation of CTT. PCH’s management is overpaying for the land owned by CTT by approximately 25%. PCH pays roughly $2600 per CTT-owned acre. This figure is 25-30% higher than the approximately $1900 – $2100 per acre of south-eastern timberland transactions. If the management can consolidate the newly formed company and use the local leverage of CatchMark to boost sales and production within the next 12-15 months, I will say the management made a fair decision to acquire the company. But if the consolidation fails or does not produce actual CAD results for shareholders then it will only be an overpaid transaction and wrongly allocated capital.

My take on PCH’s dividend

PotlatchDeltic is a reliable dividend payer timberland REIT. It has been paying dividends consecutively since 2006 and has a 2-year consecutive dividend raising streak. In addition, from time to time the management pays special dividends which are usually 2-3x of the yearly dividend. The company’s payout ratio is in the safe zone and the AFFO payout ratio is fine for now. Analysts estimate a 2.2% dividend increase for 2023. The management usually announces dividend increases in the fourth quarter and I expect that they will increase the dividend to approximately $0.45 per share from the current $0.44. This is far from the current U.S. inflation numbers but 2021’s special dividend compensated this for shareholders.

Final thoughts

There is no doubt in my mind that PCH is a good company with a decent management team. I am also sure that over the long term the company is a fair choice for income investors that want to get exposure to timberland or farmland REITs. My concerns are for the next 12-15 months where external trends are against the company while the management has to consolidate the newly bought company as well. That is why I am neutral on PCH at the moment.

Be the first to comment