WendellandCarolyn/iStock Editorial via Getty Images

After immense gains in 2020, the US logistics and transportation industry is facing growing strain. Last month, FedEx (FDX) rapidly lost around a third of its value after it pulled its annual outlook and substantially revised its growth forecast. United Parcel Service (NYSE:UPS) has similarly struggled but is generally faring far better. The company posted its Q3 earnings report on Tuesday, posting annual revenue and operating profit growth, with material sales declines in its supply chains solutions segment. The company reaffirmed its financial targets of sales of around $102B, a target operating margin of 13.7%, and an ROIC of 30%. Though its earnings report was mixed compared to expectations, investors took the news well, with the stock rising over 2% at market open, though reversing considerably after that.

On the one hand, United Parcel Service appears stronger than FedEx amid a general decline in e-commerce sales growth and other adverse economic trends. The company has seemingly taken an active approach to maintain profit margins by increasing ship rate prices more rapidly to keep up with rising costs. The stock is also not very expensive, with a “P/E” of 13.1X, a dividend yield of 3.6%, and decent historical earnings and sales growth.

That said, in today’s market with rising interest rates, I do not believe UPS is a “cheap” or “discounted” stock and may face some overvaluation. The logistics and transportation industry may face peak earnings. As noted by Jefferies analysts, the negative economic trend does not bode well for spot truck rates, which are closely correlated to UPS’s sales and income. Indeed, I believe UPS is overly optimistic regarding the macroeconomic landscape. In its earnings call, the firm noted the “macro environment remained dynamic” and avoided negatively revising its outlook despite the clear and growing indications of a negative macroeconomic trend. I believe UPS is likely to decline over the coming months as its earnings outlook declines.

Macro Headwinds Loom Large

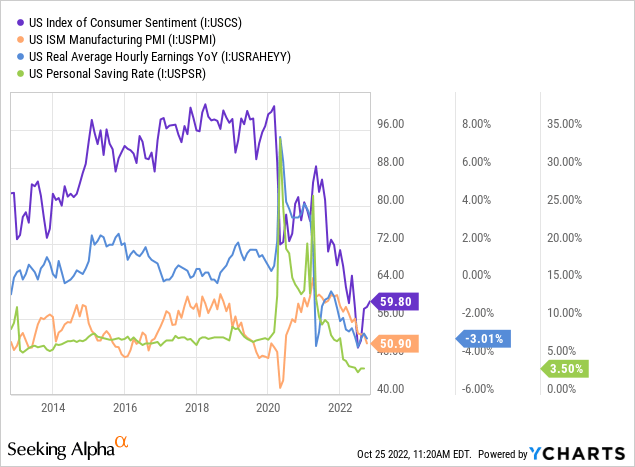

Ultimately, UPS is a macro-driven company and its strong historical growth in recent years is attributable primarily to the lockdown’s effect of increasing e-commerce sales volumes at the expense of in-store. Today, gasoline costs are generally high and may soon rise much higher, while inflation has led to moderate declines in real wages. Mixed with falling labor productivity and increasing interest rates, the demand for discretionary goods will likely decline over the coming year. See below:

Over the past two years, consumer confidence has shuttered amid declines in real hourly earnings. This trend has more recently led to sharp declines in personal savings levels and, most recently, business activity. Altogether, these data show a clear trend against discretionary personal spending, particularly on goods facing the most significant price growth. As there has not been an improvement in productivity and interest rates and inflation remain high, there are no signs that this trend will reverse any time soon.

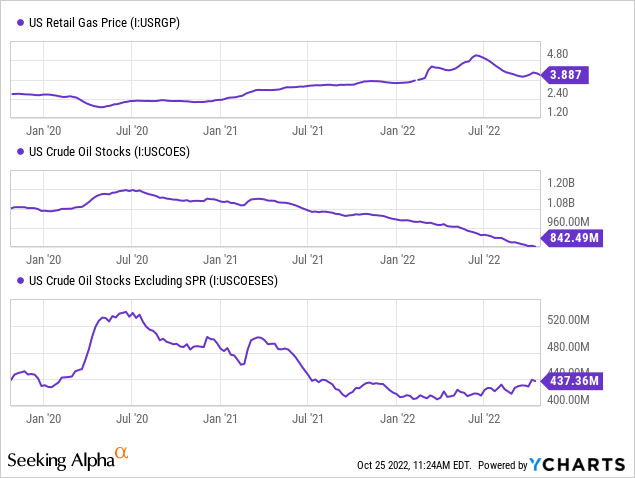

To me, gasoline prices are the chief economic factor influencing these trends as they relate to the logistics and transportation industry. Higher gas prices force freight rates to increase, usually at the expense of demand, as seen in UPS’s weak volumes. Outside of the West Coast, gasoline prices have stabilized, reaching peak levels in May. Commercial oil inventories stopped declining in late Spring and have slowly trended higher since, rebalancing the gasoline supply shortage. However, in my view, this trend is mainly artificial, as the total supply of crude oil has declined rapidly since then. The only reason commercial inventories have risen (despite a large overall decline) is the substantial decline in the Strategic Petroleum Reserve. See below:

Retail gasoline prices are heavily determined by short-term supply and demand factors. US gasoline demand has declined very slightly this year while the aggregate supply has risen materially since May amid the considerable increase in commercial oil inputs. That said, actual oil production remains well-below current demand levels, meaning a significant shortage may occur as the SPR release ends. The Biden administration recently accelerated its release schedule to keep gasoline prices moderated ahead of the November election and plan to end the release next month.

With OPEC+ pursuing cuts, the US drilling rig count stagnated, and the US emergency oil reserve significantly depleted, I believe there is a strong set-up for a significant increase in gasoline prices come 2023. Gasoline is the major driver of inflation and is particularly critical for the freight industry since it increases prices and costs at the expense of demand. Despite the moderate decline in gasoline prices, load-to-truck ratios in the freight market have fallen by over 50% this year and are now verging on 2020’s minimum level. Spot rates have declined slightly and, compared to fuel costs, may slip much more as the low ratio implies there are more available trucks than demand for trucks in the market.

In my view, this situation will likely worsen with higher gasoline prices and could see further strain by secondary negative economic trends, such as increased business inventories, low consumer confidence, and the impact of rising interest rates (which will not likely let up if gasoline-driven inflation continues). With this in mind, I believe investors should expect UPS to face some margin difficulty over the next year and may not see organic earnings growth for years to come as the e-commerce market plateaus. Very few analysts and investors appear to expect a plateau or lasting decline in real e-commerce spending, but to me, with commodity scarcity growing and global labor productivity falling, the supply of goods can’t continue to rise. If the US and international production of goods are flat or declining, people will not be able to afford to continue buying items, particularly those that are not as necessary.

What is UPS Worth?

My view on UPS largely depends on my outlook that the US and global economy are facing a large, somewhat necessary, “slimming season.” The words “recession” and “negative economy” carry some emotional charge and fail to illustrate the fact that the global economy must occasionally reduce its excesses to stay efficient. 2020’s changes led to immense excesses in financial markets (see valuations) and in the industry (see labor productivity). To me, it is natural and sensible that the US and the global economy must enter a period of reduction where efficiency can be restored. However, shock declines in European output due to war, and the potentially harmful impact of the decline in US emergency oil reserves, are exogenous factors that could unnecessarily worsen the otherwise natural recession.

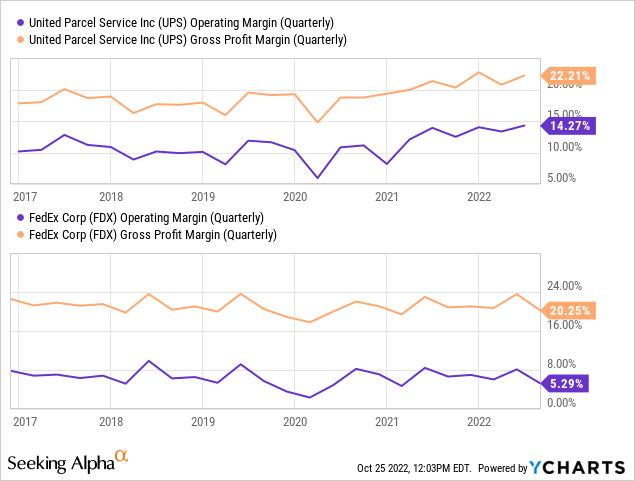

As the demand for shipping wanes, I expect UPS’s ability to use cost controls to keep margins elevated will as well. The company has increased its margins dramatically since 2020 as e-commerce demand rose and has maintained its margins despite headwinds by quickly raising costs. See below:

Compared to FedEx, UPS has maintained high-profit margins, giving the firm considerable sales and earnings growth over recent years. While analysts expect UPS’s top and bottom lines to remain stagnant, the consensus does not currently see a reversal. However, as trucking data and most other economic indications point toward a decline in demand, I believe UPS will likely see its profit margins return to normal levels and potentially lower if inflationary strains continue to mount.

UPS’s long-term fundamentals are fuel cost dependent, and there appears to be a considerable upside risk in fuel costs. If UPS maintains around $100B in annual sales, but its operating margin returns to 2018 levels (11%), its operating income will be $11B. Taking out its nearly $700M in interest and ~23% effective tax rate, I expect the firm’s annual income to be average around ~$7.15B over the coming years. A rise in revenue from inflationary pressures may cause a slight increase in its income from that level. Still, I generally expect inflation to negatively impact its profit margins (as higher prices cause volumes to deteriorate). With this in mind, there is also a decent possibility that UPS will face a more severe decline in profits if the recessionary trend becomes too large.

FedEx currently trades at a ~11X forward “P/E,” and, in my view, UPS has the same degree of fundamental risk. Though its margin-supporting actions in Q3 indeed underscore those risks, I think they may prove to be short-lasting given the macroeconomic environment. Accordingly, I believe UPS may require a low valuation premium to offset its risks. Valuing UPS at an 11X “P/E” with an expected income of ~$7.15B, my “fair value” market value assessment comes out to roughly $79B. This valuation is 45% below UPS’s current market capitalization, suggesting a stock-price target of ~$93.

The Bottom Line

UPS had a better Q3 than many expected, but Q3 was generally a good quarter as many economic strains took a backseat. Gasoline prices fell, the manufacturing PMI and consumer confidence flattened, and the GDP outlook rose considerably. While some may see that as an indication of a “bottom,” it appears to be a respite from the general trend, partially attributable to the SPR impact on inflation.

The first month of Q4 saw relatively significant declines in the PMI and consumer confidence while gas prices rose slightly. As the quarter continues, I expect these trends to become larger and will be prolonged into 2023. Many see “bad news as good news” since weak data suggests an end to the Fed’s rate hikes. However, if gasoline prices rise as expected, the Federal Reserve’s hands will be tied as inflation strains continue despite headwinds. As such, I do not believe that UPS can avoid a significant and lasting reversal in its profit margins.

My outlook for UPS is quite bearish and is likely well below that of most analysts. That said, UPS was trading closer to the $80-$110 price range from 2013 to 2020. While the firm’s value rose dramatically in late 2020, I do not believe its fundamental market position improved markedly. Indeed, its sharp margin spike since late 2020 may be a “one-off” due to short-lasting changes in the supply-demand balance for e-commerce goods. The economic data indicates the supply-demand balance is reversing, so UPS may soon see the most considerable earnings shock its faced since 2008.

Be the first to comment