Feverpitched

Introduction

In the world of stock investing, I believe in the adage that it’s better to be “mostly right than precisely wrong”. My strategies and techniques never claim to have a lot of precision. I don’t really know with a high degree of confidence what any particular stock price will do over a specific period of time. However, I do have a high degree of confidence that if I place enough bets on enough stocks using my strategies, that I can achieve above average returns over time.

But every now and then certain stocks come along that exemplify what I’m trying to do with my stock analyses and everything comes together and I end up being almost precisely correct. PNC Financial (NYSE:PNC) stock is one such stock. I first bought PNC in my marketplace service, The Cyclical Investor’s Club, on March 23rd, 2020, which just happened to be the day the market (and PNC stock) bottomed. I bought a lot of stocks in March 2020, somewhere around 30 of them in total, and I wrote a series of public articles about the 20 of them that were in the S&P 500 index in the months that followed. My PNC article “Stocks I Bought On The Dip: PNC Financial” was published in June 2020. In that article I explained the process I used to buy the stock. Of the 30 stocks I bought in March 2020, only three of them were purchased on the 23rd, the day the market bottomed. (Eaton Vance, which was bought-out seven months later for a 161% gain, and Striker (SYK) which I took profits on in October 2020 for a +63% gain, were the other two) So, 90% of the stocks I bought during the March 2020 crash, were not purchased on the day the market bottomed, and, in fact, I had no idea that particular day would be the bottom. Each stock was purchased based on its individual merits assuming we would have a pretty bad recession.

I make these points up front to dispel the notion that any of my strategies are primarily about so-called “market timing”. While I take into account the current macro circumstances, I don’t let that be the primary factor as to whether I buy a stock or not.

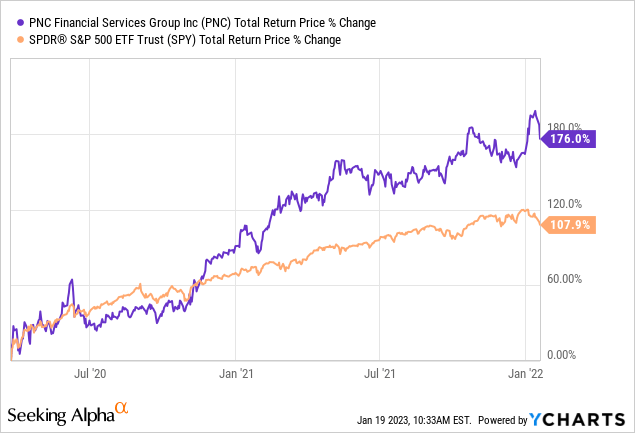

So, I bought PNC right at the bottom, and in January of 2022 (last year) I published an article where I explained why I had sold PNC along with five other financial stocks titled “6 Financial Stocks I Recently Sold, And 2 I Will Hold For The Long Term“. That article came out a few days after I sold PNC. Here is how it performed while I held it:

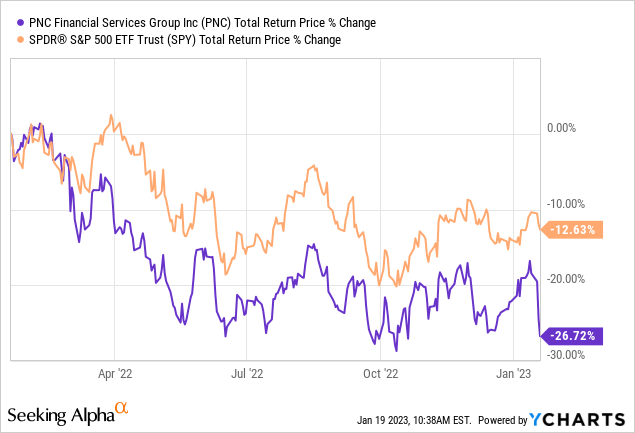

I did really well in just under a two-year holding period. You can read my reasoning for selling PNC in the linked article above, but mostly it had to do with the stock’s high price cyclicality, late market cycle dynamics, and the removal of fiscal stimulus by the government. So, while I bought PNC based on fundamentals, I sold it mostly based on macro issues that I thought had a very high probability of eventually affecting both PNC’s fundamentals and its stock price in a very significant way. This ended up being a near perfect call, and here is how the stock has performed since I took profits.

The price is down more than -25% and down twice as much as the S&P 500. I had no idea I was selling very near the precise top in the price, I just knew that the risks to the downside over the medium-term had risen high enough that it made sense to sell. There are plenty of stocks that I sell which keep going up immediately afterward. Usually, even if I’m right, I’m not precisely right.

Now let’s move forward to more recent times since the stock price has dropped. I last covered PNC three months ago in my article “PNC Stock Is Down 30% Off Its Highs. But Is Cheap Enough To Buy?” I rated PNC stock a “Hold” in this article. Here is some of what I had to say:

Due to an ending of federal government stimulus and the Federal Reserve raising interest rates, I think there is an above-average chance that the US economy experiences at least a mild recession as soon as Q1 2023. This can typically mean two things for a stock. First, it can mean that EPS disappoints, and instead of growing 14% in 2023 as analysts now expect (or growing near the average of 5.55% as I estimated), EPS could fall instead. Judging from PNC’s historical EPS declines, I think assuming a decline as large as -20% to -30% is reasonable. The second thing worth paying attention to is how much the market typically discounts these falling earnings. I call this metric the “Recession P/E” and it is the low monthly P/E that the stock has experienced during past recessions. This can help us predict how low the P/E might go in a future recession.

PNC recently announced quarterly earnings and it missed analysts expectations. For me, it’s not particularly important what happened this quarter. With a few exceptions, I think stock moves immediately following earnings reports are meaningless for investors who are actually investing based on an earnings-based fundamental analysis. Earnings don’t have a lot of predictive power over the short-term. It’s over the medium and long term that the stock price correlates more closely to the earnings trend. This means, what we should care about are what analysts think a year or two from now about earnings. In the quote above from my last article I noted that PNC’s near-term average earnings growth rate to be about 5.55% and that was my baseline expectation for 2023 if we didn’t have a recession, while analysts three months ago were expecting 14% earnings growth in 2023, or $16.57 per share. Now that PNC missed earnings, that expectation from analysts has fallen.

FAST Graphs

What we really care about when we are investing today is what earnings will do years into the future and what we are paying right now for those future earnings. Analysts have changed their estimates a lot for this year (most of the change came overnight after earnings were reported) and now analysts expect 6% earnings growth in 2023, 4% growth in 2024, and 6% in 2025, for an average growth rate of 5.33%. This is basically spot-on with the 5.55% I used for my PNC valuation three months ago. So, now analysts agree with me. (This is why it’s important to do your own work when it comes to valuations.)

I’m going to share a new fundamental analysis in the next section of the article. The big question remains about what one thinks about a US recession in 2023. The estimates above, in my opinion, assume a recession will be avoided. So, I’ll first run an analysis assuming no significant recession, and then I’ll share how I am currently accounting for a potential recession in 2023 when it comes to PNC stock as well.

My Valuation Method For PNC Financial

The valuation method I use for PNC first checks to see how cyclical earnings have been historically. Once it is determined that earnings aren’t too cyclical, then I use a combination of earnings, earnings growth, and P/E mean reversion to estimate future returns based on previous earnings growth and sentiment patterns. I take those expectations and apply them 10 years into the future, and then convert the results into an expected CAGR percentage. If the expected return is really good, I will buy the stock, and if it’s really low, I will often sell the stock. In this article, I will take readers through each step of this process.

Importantly, once it is established that a business has a long history of relatively stable and predictable earnings growth, it doesn’t really matter to me what the business does. If it consistently makes more money over the course of each economic cycle, that’s what I care about – numbers over stories.

FAST Graphs

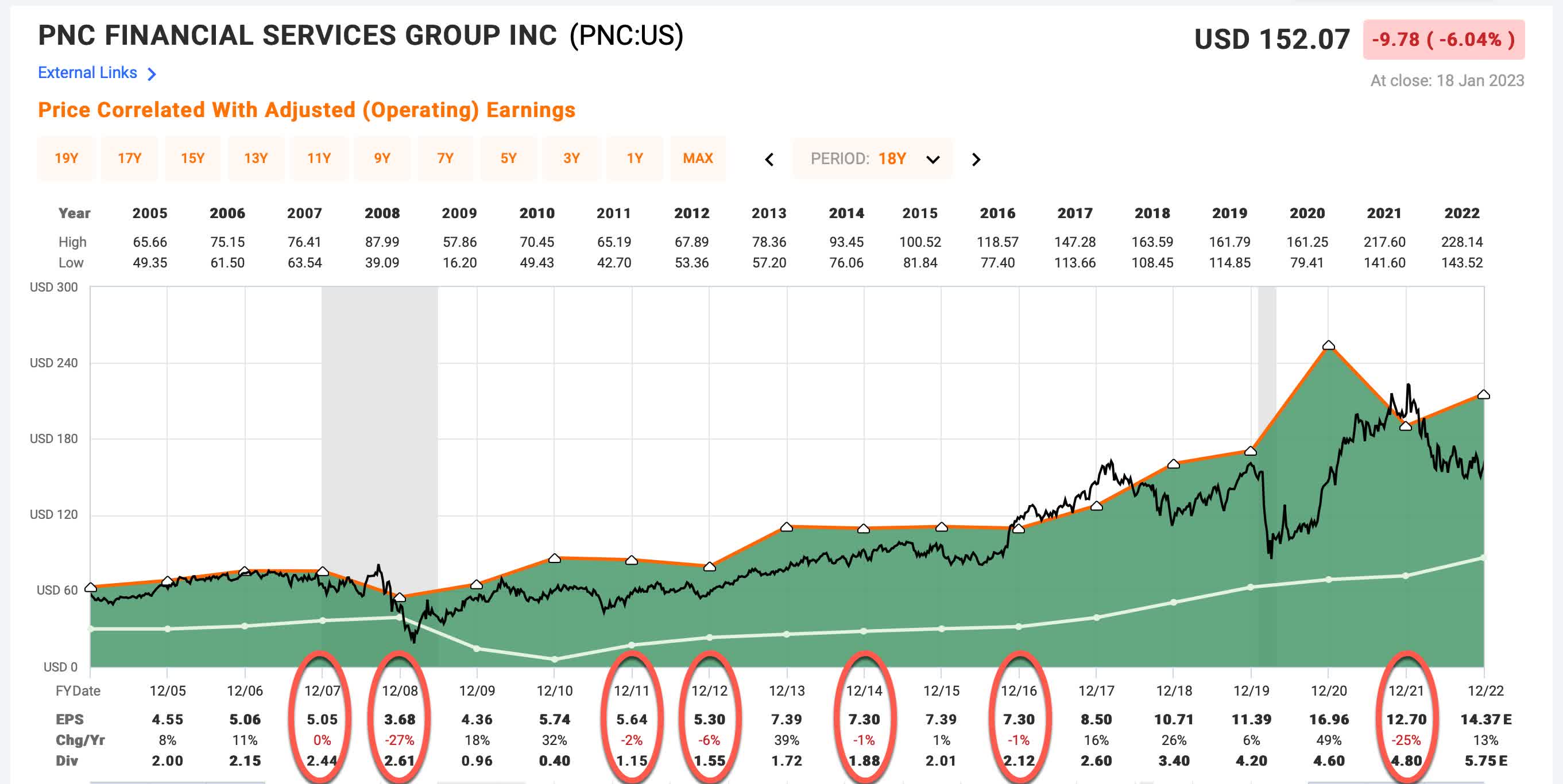

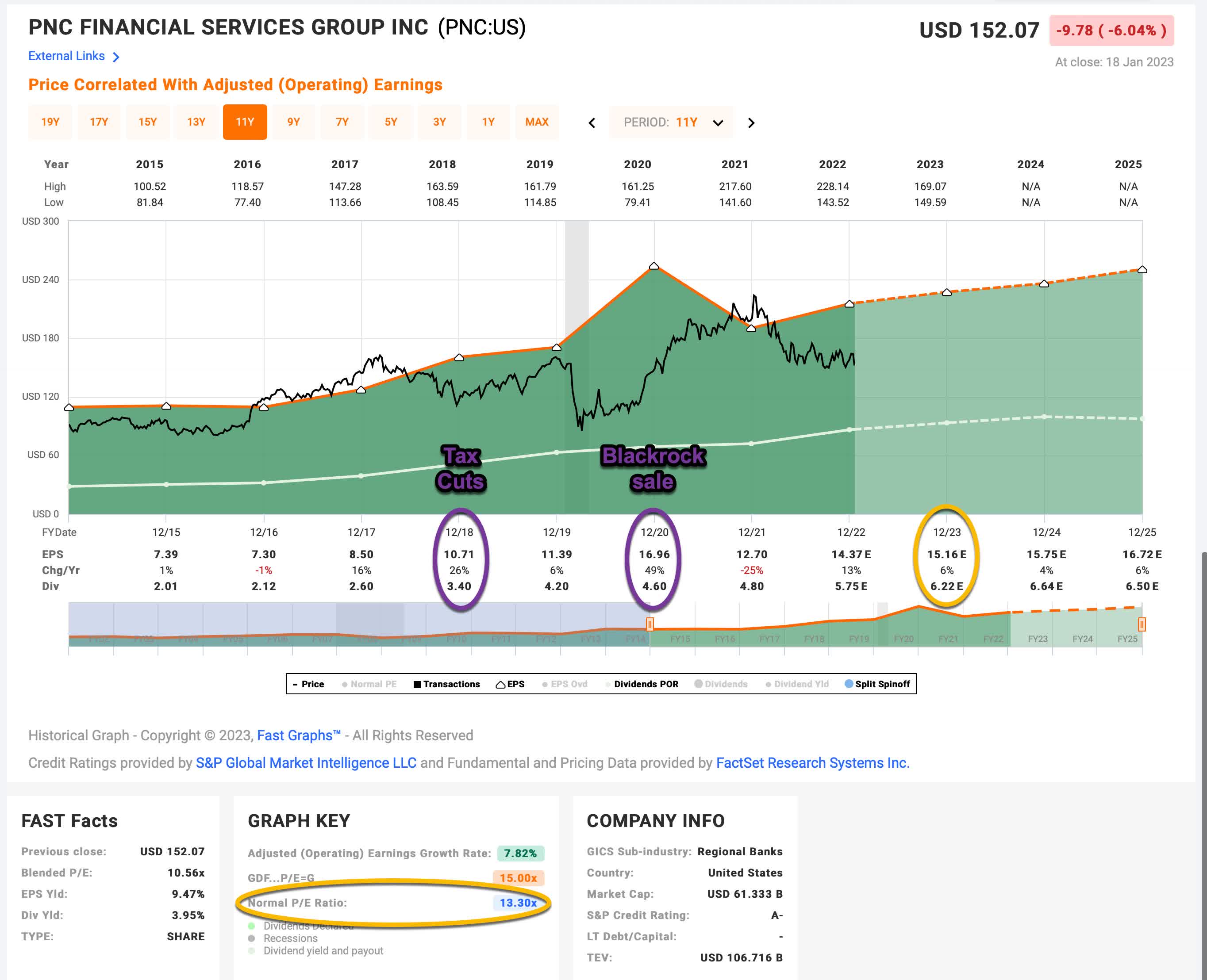

Since 2004, PNC has experienced seven years where earnings growth was negative compared to the previous year. At first glance, this seems like a lot, but five of the seven years were single-digit declines, and the most recent 2021 EPS decline came on the back of an unusually large growth year in 2020 which was likely partially the result of their selling their stake in BlackRock (BLK). Since 2021 EPS was higher than 2019, and 2022 has come in higher than 2021, I wouldn’t really count the 2021 EPS decline as a real decline. This leaves the only EPS growth decline of any real significance to be 2008 during the GFC. I have looked at hundreds of historical EPS graphs of banks and other financial businesses, and the truth is that to only have had a -27% decline in 2008, given the circumstances and compared to peers, was exceptionally good. Because of that, I classify PNC as a moderately cyclical business, and therefore it is appropriate to use historical earnings patterns to value the stock. (If earnings had been more cyclical, I would use a different valuation technique.)

PNC Stock – Market Sentiment Return Expectations

In order to estimate what sort of returns we might expect over the next 10 years, let’s begin by examining what return we could expect 10 years from now if the P/E multiple were to revert to its mean from the previous economic cycle. For this, I’m using a period that runs from 2015-2023.

FAST Graphs

PNC’s average P/E from 2015 to the present has been about 13.30 (the blue number circled in gold near the bottom of the FAST Graph). Using 2023’s forward earnings estimates of $15.16 PNC has a current P/E of 9.73. If that 9.73 P/E were to revert to the average P/E of 13.30 over the course of the next 10 years and everything else was held the same, PNC’s price would rise and it would produce a 10-Year CAGR of +3.18%. That’s the annual return we can expect from sentiment mean reversion if it takes 10 years to revert. If it takes less time to revert, the return would be higher.

Business Earnings Expectations

We previously examined what would happen if market sentiment reverted to the mean. This is entirely determined by the mood of the market and is quite often disconnected, or only loosely connected, to the performance of the actual business. In this section, we will examine the actual earnings of the business. The goal here is simple: We want to know how much money we would earn (expressed in the form of a CAGR %) over the course of 10 years if we bought the business at today’s prices and kept all of the earnings for ourselves.

There are two main components of this: the first is the earnings yield and the second is the rate at which the earnings can be expected to grow. Let’s start with the earnings yield (which is an inverted P/E ratio, so the Earnings/Price ratio). The current earnings yield is about +10.28%. The way I like to think about this is, if I bought the company’s whole business right now for $100, I would earn $10.28 per year on my investment if earnings remained the same for the next 10 years.

The next step is to estimate the company’s earnings growth during this time period. I do that by figuring out at what rate earnings grew during the last cycle and applying that rate to the next 10 years. This involves calculating the historical EPS growth rate, taking into account each year’s EPS growth or decline, and then backing out any share buybacks that occurred over that time period (because reducing shares will increase the EPS due to fewer shares).

PNC has bought back quite a bit of stock since 2015, nearly 23% of the company. I make adjustments to control for the effects these repurchases have on EPS in order to get an estimate of what rate earnings are organically growing. I also include the -25% negative EPS growth year last year. In the end, I get an estimated earnings growth rate for PNC during this period of +5.36%. However, it’s worth noting that this does include a big 26% growth year in 2018, boosted by tax cuts that are unlikely to happen again, and it doesn’t include a “real” recession drawdown as we saw in 2008. So, while I think my earnings estimate is reasonable (and more conservative than the FAST Graphs’ +7.82% EPS growth rate over this period), it’s possible that earnings during the next cycle could be lower if earnings fall during a recession next year. I will address this possibility later in the article.

Next, I’ll apply that growth rate to current earnings, looking forward 10 years in order to get a final 10-year CAGR estimate. The way I think about this is, if I bought PNC’s whole business for $100, it would pay me back $10.28 plus +5.36% growth the first year, and that amount would grow at +5.36% per year for 10 years after that. I want to know how much money I would have in total at the end of 10 years on my $100 investment, which I calculate to be about $238.24 including the original $100. When I plug that growth into a CAGR calculator, that translates to a +9.07% 10-year CAGR estimate for the expected business earnings returns.

10-Year, Full-Cycle CAGR Estimate

Potential future returns can come from two main places: market sentiment returns or business earnings returns. If we assume that market sentiment reverts to the mean from the last cycle over the next 10 years for PNC, it will produce a +3.18% CAGR. If the earnings yield and growth are similar to the last cycle, the company should produce somewhere around a +9.07% 10-year CAGR. If we put the two together, we get an expected 10-year, full-cycle CAGR of +12.25% at today’s price.

My Buy/Sell/Hold range for this category of stocks is: above a 12% CAGR is a Buy, below a 4% expected CAGR is a Sell, and in between 4% and 12% is a Hold. With a 12.25% 10-year CAGR expectation, that would make PNC stock a “Buy” at today’s prices, assuming we don’t have a recession. (However, I think we will have a recession, so I’m not buying, yet.)

Recession Considerations

I always like to start most of my analyses with a couple of basic assumptions. The first is that the historical trend is likely to continue unless there is some obvious change occurring or likely to occur in the near future. And then I like to share a basic analysis that doesn’t make a whole lot of adjustments so we can have a baseline to work with. Sometimes the baseline itself is so extreme in either direction, no further work is needed. But other times, as with PNC, the baseline looks pretty attractive and whether or not one decides to buy the stock depends on something mostly independent from the historical earnings and price trend. Because predicting things like recessions is pretty hard most of the time, especially when it comes to the timing and degree of those recessions, I usually try to show both the baseline, and then also my personal take on the other factors we should consider, like recessions.

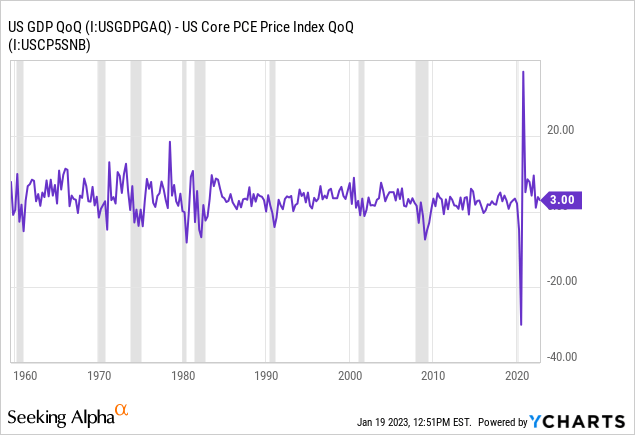

Many people still insist that the US was in recession in June and July of 2022 because we had two quarters of negative real GDP in a row. Most of the people also thought it was a good time to buy stocks because the stock market was off its highs and we were “in a recession” so the likely future movement of the market was up and stocks were a good value then. These people were wrong. We were not in a recession, and the stock market had not bottomed. There are a variety of reasons for their mistake (the most obviously being we’ve stayed at full employment since then) but what I have suggested for people who wish to know whether we are in a recession or not to do is to look at core inflation instead of headline inflation relative to GDP. It has had just as good predictive powers of historical recessions as the “two negative quarters in a row” metric has had, but it is less volatile and therefore less likely to be effected by the transitory inflation caused by supply chains and stimulus money and Russia’s invasion of Ukraine.

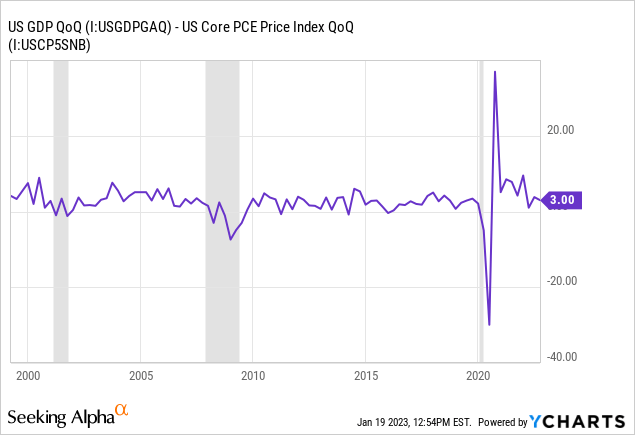

Above is the long-term trend of this spread. When it turns negative for more than a quarter, we have been in recession. When it is positive, we are not in a recession. Below is a more zoomed-in version of just the past 25 years or so.

If this spread hasn’t turned negative, then we are not in a recession, yet. Currently, it is at 3.00 and trending down. (Back in June it was about 2.4 if I remember correctly.) The next GDP numbers come out in a week’s time. I expect them to be lower, but probably still positive. However I expect this spread to turn negative in 2023 at some point, and we will probably be in recession at that time. I’m not sure about the timing, but broadly speaking, 2023 is a high-risk year overall.

What this means for PNC stock is that even though based on recent averages it is at a decent value at today’s price, we haven’t had a “real” recession since 2008, so a recession has not been factored into those estimates. There are two things we should expect during a recession. First, we should expect earnings growth to be significantly negative. And second, we should expect that the stock price will be more negative as well. I like to use what the low P/E was during previous recessions as guide for what the price could do during the next recession. I call this metric the “Recession P/E”.

Here is what I thought in my last article:

We have three different routes we can go with this. We can use the Recession P/E from 2008/9, or the one from March 2020, or an average of the two. The 2008/9 P/E was extremely low at 4.87, while the 2020 low was 6.65. Because the current downturn is not centered around the financial system, and banks are much better situated now than in 2008, I think it makes more sense to use the higher and more optimistic recession P/E from 2020 of 6.65. Currently, using forward earnings for this year, PNC’s price would need to drop about -35% more from here to meet that recession P/E, which is a price of about $97 per share.

Based on the changes and updates I made this quarter for PNC stock, this number has now risen to $101 per share. So, that is the price I would want the stock below before I bought it going into a recession. Once we are actually in the recession, often analysts then get overly negative with earnings expectations, so then I remove the Recession P/E factor and go back to my standard form of analysis, which usually has more conservative estimates at that point in time. Often, if we aren’t having a total crash as we did in March 2020, the Recession P/E price from before the recession started and the updated buy price during the recession converge pretty close together near the same price.

Conclusion

Because I’ve been pretty precise with my predictions of when to buy and sell PNC stock in the past, I want to emphasize again that this was partly luck. I just try to generally get the odds in my favor, and sometimes there are few stocks that happen to hit right at the midpoint of my expectations. PNC stock might ultimately fall to $80 during a recession, or only fall $120. But I think that 1) there is an above average chance we have a recession in the US this year, 2) that will cause PNC’s earnings and stock price to fall more from here, and 3) if I can buy around $100, which has a decent chance of hitting, then I will have a very high probability of producing well above market average returns within five years.

I monitor hundreds of stocks. Right now I have enough cash to buy about 25 1% weighted positions during the next downturn. So I don’t need every single stock I monitor to hit my buy prices. I just need 25 of them to do it, preferably from a variety of industries. PNC is on my list, and getting closer to my buy price again, but it’s not quite there yet. I remain neutral on the stock, and will be patient before buying this one again.

Be the first to comment