Elis Cora/iStock Editorial via Getty Images

Main Thesis & Background

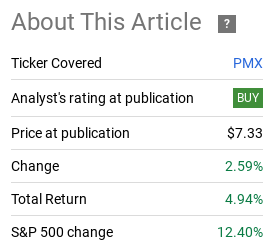

The purpose of this article is to evaluate the PIMCO Municipal Income Fund III (NYSE:NYSE:PMX) as an investment option at its current market price. This is a fund I keep on my radar screen because I see value in PIMCO’s CEF offerings across the board on many occasions. I am an avid investor in the muni space, and I have held muni CEFs from PIMCO in the past.

I saw some value in PMX when I wrote about it last summer. The muni space as a whole was fairly beaten-down, and PMX had a relative valuation advantage against its two “sister funds” from PIMCO (the PIMCO Municipal Income Fund (PMF) and the PIMCO Municipal Income Fund II (PML). In hindsight, my bullishness was vindicated, with PMX registering an attractive gain since that article was published:

Fund Performance (Seeking Alpha)

With 2024 underway in a fairly positive light so far, I thought it was time to do another review of PMX. Rather than selling to protect these gains, I actually see a continued backdrop for the fund to keep on delivering. It has a reasonable valuation and munis as a whole look attractive right now – two factors that suggest “buy” continues to be the correct rating for this CEF. I will explain this reasoning in more detail below.

Valuation Backdrop Still Favorable For PMX

The first topic I will cover is a reinforcement of a point I made back in August. This was that PMX looked attractive in relative terms to its sister funds from PIMCO. These three national muni funds have plenty of overlap amongst their portfolios, so I tend to give a lot of weight to the premiums or discounts to NAV that each trade at. After all, if I can get similar exposure for a cheaper price – what isn’t there to like about that?

Last year, PMX won this valuation attribute, and we can see that today that story remains the same. PMX has both an attractive discount to NAV in isolation and in comparison to the other two peers from PIMCO:

| Fund | Current Premium to NAV |

| PMX | (7.96%) |

| PML | (3.27%) |

| PMF | (.73%) |

Source: PIMCO

As you can see, all three currently have discounts but PMX’s is clearly the favorite for value-oriented investors. While a discount (or premium) is not an attribute that should be taken as a buy or sell rationale categorically, it does help to decipher entry points when all other factors are equal. I see a buy case for munis at the moment – and I will get to why later in this review – so finding muni funds with attractive prices seems like a no-brainer at the moment.

PMX delivers on this score. The discount near 8% is attractive on the surface and clearly beats the other two PIMCO funds in this regard. As a more conservative investor, this puts PMX on my radar screen in a big way.

I Like The Sector’s Momentum

Shifting to a more macro-view, why would investors want to own munis at the present moment? For me, I typically like this sector as a way to hedge equity risk and to round out my portfolio. As a working processional in a high tax-bracket, this is often a more desirable place for me to park my cash than savings accounts or corporate bonds. This is dependent on each individual as to whether or not munis really make sense for them. For lower-income individuals, it may not, so understand this going in.

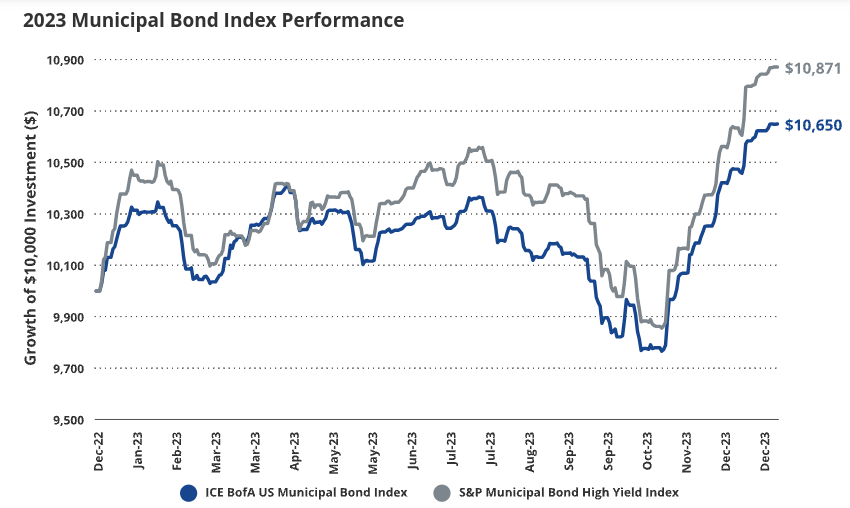

One aspect of the muni market that I don’t find particularly appealing is how it has gotten more volatile over time. It used to be a boring sector, but now it has more swings than in decades past. Fortunately, the sector’s favor has turned overwhelmingly positive of late. After a rocky start to 2023, the final quarter of the year showed across-the-board gains in the muni sector among high-grade and junk-rated issues alike:

2023 Performance (Municipal Bond Sector) (FactSet)

Of course, there are two ways to look at this. One – the view I take – is that this bullish momentum is set to continue because the underlying story for munis is favorable. Investors have wised up to this and gains are likely to keep coming in for the short-term at least.

However, the other view is that munis are ripe for a correction, given the large gains they have seen since October. I won’t pretend to say I know for certain what scenario will play out (maybe neither – they could move in a straight line!).

But I am aware of the run the sector has had, and that does mean investors shouldn’t get too carried away with risk right now. But that again reinforces why PMX is a decent option. While the sector has rallied broadly, PMX still has a discount to NAV nearing double-digits. This helps protect against some downside risk and offers value in a sector that is getting short on value due to the recent rise. Therefore, I see the underlying momentum and PMX’s cheap price as support for buying.

Income Metrics Steady

My next topic is a slightly mixed bag. PMX is not unique with respect to the fact that leveraged CEFs – whether muni focused or not – have been under pressure since the Fed started raising rates. With long-term economic concerns abound, investors have kept the longer-end of the yield curve low while the Fed has pushed short-term rates high. This resulted in an inversion of the curve, making borrowing more expensive while limiting longer-dated opportunities. Since CEFs try to compound their earnings through borrowing short and investing long, this inherently presented challenges.

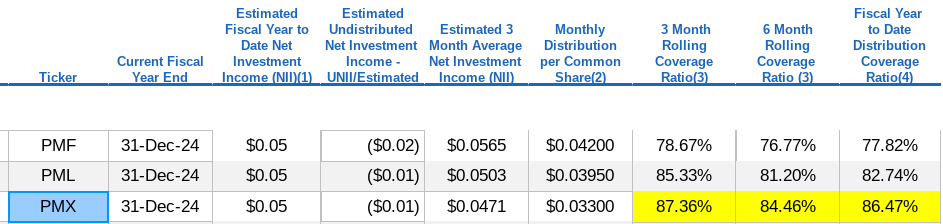

For the time being, this concern has not gone away. So investors need to be careful and nimble because if the Fed disappoints in 2024, then more pain could be on the way for PMX and for the plethora of muni CEFs that dominate this space. Case in point is that income metrics for PMX are not exactly great, suggesting that further weakness could result in a distribution cut:

PIMCO’s UNII Report (January Data) (PIMCO)

Obviously these numbers don’t inspire a tremendous amount of confidence. But I did say this was a “mixed” attribute. The positive message one can takeaway from this is that these figures are relatively unchanged from last summer. So while coverage ratios in the 80% range aren’t “great”, they have stabilized. The absence of deterioration in the fact of a persistently challenging yield curve is important. Further, PMX has a high tax-adjusted yield for those in upper tax brackets. This means investors will likely be drawn to this fund even if a cut does occur, as long as it is moderate. For these reasons, I am able to overcome these income figures and maintain a bullish rating.

Tax Rates Will Increase Without Action By Congress

Shifting back to a macro-discussion, a watch item for me going forward will be tax rates in the US. This is not something to be overly concerned with right now – as no changes will be expected in an election year – but in the coming years it will be a front-and-center topic. This means that keeping this on the radar and monitoring developments will be crucial for portfolio planning in the second half of 2024 and certainly in 2025.

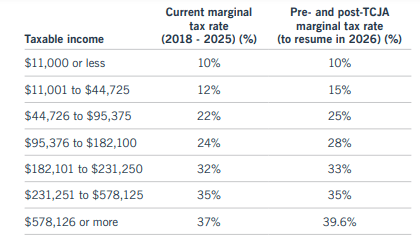

What I am referring to is the change in tax rates from the 2017 Tax Cuts and Jobs Act (TCJA). This act led to a reduction in federal tax rates for most filers, which in isolation makes the tax-exempt status of munis less attractive. This is because taxpayers now save less on their taxes since the tax burden is lower. By contrast, when tax rates are set to increase, munis can often get a boost as more people are drawn to the space.

For illustrative purposes, here is a look at how rates were impacted by the TCJA. Importantly, these “new” rates are set to expire at the end of the 2025 calendar year. So, without new legislation or an extension of the current rates, we will see a return to prior levels:

Tax Rates: Before and After TCJA (IRS)

I must reiterate, this is not a short-term headwind. Tax changes are not going in to effect this year and Congress has all of 2025 to amend or extend current rates before they are sun-setted. But it remains a top-of-mind focus for me because Congress, in its split-form right now, can’t agree on much. This suggests to me that a compromise on taxation may be hard to come by in the future. If so, rates will be forced higher as current law expires, providing a tailwind for munis given their tax-exempt status. This could bode well for PMX.

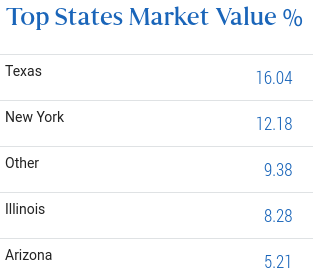

Texas Exposure A Nice Diversifier

My final point goes back to PMX specifically. As investors in the muni CEF space are probably aware, these funds tend to be dominated by the three major players in the sector – which are California, New York, and Illinois. But Texas has been creeping up to become a major contender for muni investors, especially over the past decade. While many funds don’t have a ton of Texas exposure, PMX sets itself apart by having this state as its top weighting:

PMX’s State Exposure (PIMCO)

Whether or not this is “good” or “right” for you is dependent on your individual circumstances. If you live in Texas, then it is probably a good thing. But even if you don’t, likely myself who lives in North Carolina, I see benefits to this. I generally have national muni funds and NC-backed individual issues. So while Texas bonds don’t give me any additional tax advantages, they do help in terms of diversification. It keeps my portfolio from getting too concentrated in any or jurisdiction or sector, and that is generally something I favor.

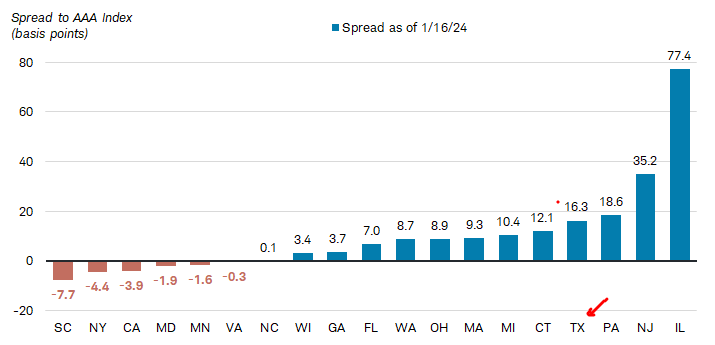

Of course, diversification just for diversification’s sake is not always a net gain. But in the case of Texas’ bonds, I believe it is. The state has seen large population growth over recently – and even over the longer term. This has boosted state coffers as more companies have flocked there. Further, the state maintains a very strong credit rating, while still offering yields well above a generic AAA-rated bond:

Spread to Generic AAA-rated Muni (Charles Schwab)

To reaffirm, Texas is rated triple-A. But its GO-backed muni bonds offer a positive spread to an average triple-A rated bond. So that positive yield pick-up is favorable and helps to boost PMX’s overall yield while not increasing the inherent risk of the fund. That’s a win-win in my book, and helps support my “buy” rating for the fund.

Bottom-Line

PMX has seen a nice gain since my last review, and I see the potential for that to continue. The yield remains attractive, the fund’s holdings help to diversify my muni portfolio, and its discount is attractive both on the surface and compared to its direct competitors from PIMCO. With equities hitting new highs, building on my hedges makes sense here, and I see PMX as a prime way to do that. Therefore, I will be maintaining my “buy” rating on this fund, and suggest my followers give the idea some thought at this time.

Be the first to comment