abadonian

Summary

Our initial report rated Dream Industrial REIT (TSX:DIR.UN:CA / OTC:DREUF) a Hold due to its relatively thin margin of safety and moderately lower portfolio quality relative to certain peers (e.g., Granite REIT (GRT.UN:CA)). This report discusses Dream’s Q4 earnings and provides an updated valuation. While the quarter demonstrated strong rent growth and resilient occupancy and margins thanks to the continued strength of the industrial market, Dream’s valuation has remained relatively high. We maintain our Hold rating and continue to prefer Granite among TSX-listed industrial REITs.

Earnings Update

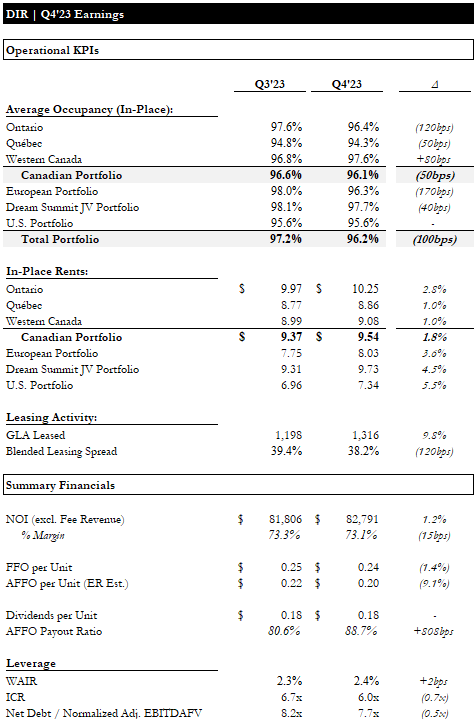

Starting with the core operational metrics, occupancy remained relatively stable across the portfolio, except for ~120bps and ~170bps declines in Ontario and Europe, respectively. These vacancies were anticipated and are expected to be backfilled quickly at significantly higher rates.

Average in-place rents for Ontario, Europe, and the US JVs grew robustly, driven by rent escalators and strong leasing activity. ~1.3MM sqft were leased in the quarter (n.b., ~10% more than the PQ) with a blended ~38% leasing spread.

Q4 Earnings Update (Empyrean; DIR)

This drove ~1.2% NOI growth QoQ, with no material change to margins. However, G&A and interest costs grew ~4% and ~8% QoQ, respectively, driving a ~1.4% decrease in FFO per unit. A ~136% increase in non-recoverable capex drove a ~9% QoQ decline in our estimated AFFO per unit, causing the payout ratio to expand from ~81% to ~89%.

Significant growth in EBITDAFV, mainly attributable to higher distributions from EAIs, drove leverage down ~0.5x. However, interest coverage tightened ~0.7x, though it remains at a healthy 6.0x.

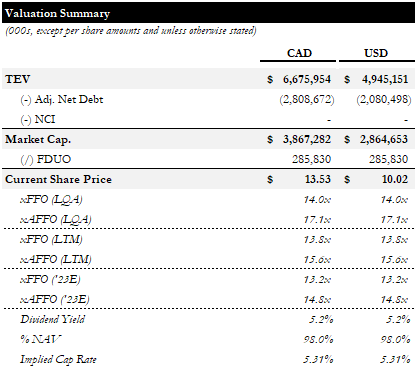

Valuation

Dream is now trading for 14.0x / 17.1x LQA FFO / AFFO and 13.8x / 15.6x LTM FFO / AFFO. Assuming ’24 FFO / AFFO growth of 5% (n.b., management’s guidance is for “mid-single-digit” FFO per unit growth), current prices imply 13.2x / 14.8x FFO / AFFO. Our revised NAVPU estimate implies a ~2% discount and ~5.3% cap rate.

Valuation Summary (Empyrean; DIR)

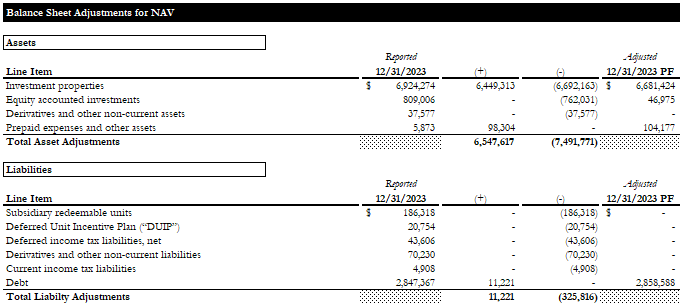

Our principal balance sheet adjustments are described below. Our revised NAV estimate is based on a ~5.46% blended cap rate and ~10% NOI growth over the NTM.

Balance Sheet Adjustments (Empyrean; DIR)

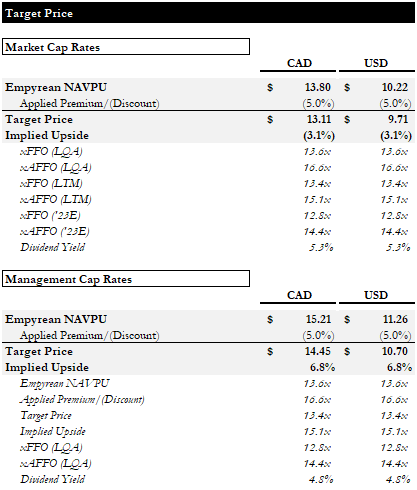

Our target prices are derived by applying a 5% discount to our NAVPU estimate, accounting for the Dream’s external management and slightly lower portfolio quality than peers. We see modest downside risk to our base case and modest upside potential to our “upside” case, which is based on management’s cap rates (n.b., the reported “implied” cap rates).

Target Price (Empyrean; DIR)

Considering the lack of a sufficient margin of safety and the near-term FFO/AFFO pressures from higher interest costs (n.b., ~11% of total debt maturing through ’24), we still do not view the units as attractive. However, we believe the large loss-to-lease combined with near-term lease expirations and the continued strength of the industrial market should provide some level of downside protection. Therefore, we maintain our Hold rating.

Conclusion

Dream’s Q4 earnings demonstrated the continued strength and resilience of the industrial asset class across its core markets. Unfortunately, rising interest costs, overheads, and non-recoverable capex somewhat overshadowed the operational improvements. While we believe the strength of underlying industrial fundamentals should mitigate substantial downside risk, we do not see an adequate margin of safety. We maintain our Hold rating and are looking for more attractive valuations to consider getting bullish.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment