wildpixel

We own shares of Pluri Inc (NASDAQ:PLUR), to our regret. We held the stock all the way down, sold half our shares, and hope our children will profit in the future from Pluri’s R&D. We are bearish in the near term but recommend holding shares in case there is a share price recovery in the distant future.

The Company

Pluri Inc, formerly known as Pluristem Therapeutics Inc, changed its name to Pluri Inc. in July 2022. We use Pluri throughout this article. Pluri was incorporated in 2001 and is based in Haifa, Israel. Pluri Inc is an Israel-based biotechnology research company with various clinical studies underway.

The company is laser-focused on developing and commercializing medical, pharma, and food products from its unique R&D platform using “allogeneic cells originating from the fetal and maternal cells from the placenta,” the company told shareholders in a September 22, ’22 letter.

Pluri has pursued a plethora of exciting projects over the decades employing cutting-edge technology but ending with no commercial impact. For example,

- Pluri researchers pursued treating bone marrow disease in 2008.

- Pluri got the go-ahead in 2011 from the FDA to pursue stem cell use for an orphan drug treating Bueger’s disease.

- In 2017, Pluri launched a pilot study of PLX-R18 cell therapy initiated by the U. S. DoD. The study examined the effectiveness of PLX-R18 as a treatment for ARS prior to, and within the first 24 hours of exposure to radiation. In July 2019, we presented positive results from a series of studies of our PLX-R18 cell therapy product conducted by the DoD.

- In 2019, Pluri explored utilizing its proprietary 3-D cell culturing technology to lab manufacture cannabinoid-producing cells; manufactured medical cannabis will grow faster and in greater quantity than in fields.

- The company pursued stem cell therapies for COVID-19 to stem the pandemic.

- In 2022, Pluri announced it signed a joint venture with Tnuva Group, Israel’s largest food manufacturer, to develop and market cultivated meat and additional biologics technology working toward a mock-meat product launch.

Current Product Candidates

Articles about Pluri’s work appear in a number of scientific publications. In its September 21, ’22 SEC Annual Report, Pluri highlights and details the following products it is pursuing from its allogeneic placenta-based cell therapies. Here are several that “As a platform technology company, we are currently developing additional product candidates, which are modified or induced PLX cells:”

- PLX-PAD is its first product candidate. It is in a Phase III multinational clinical study in recovery following surgery for hip fracture. PLX-PAD is also under clinical development in collaboration with Tel Aviv Sourasky Medical Center (Ichilov Hospital) for the treatment of Steroid-Refractory cGVHD.

- Pluri completed its first in human Phase I clinical study of PLX-R18 for incomplete hematopoietic recovery following hematopoietic cell transplantation, or HCT, in the United States and Israel.

- In collaboration with the National Institutes of Health and the U.S. Department of Defense, Pluri is developing a solution for ARS following or before exposure to massive radiation.

- Modified PLX cells developed in the last decade led to creation of an allogeneic platform based on cells originated from the fetal and maternal cell from the placenta. Using this platform the company claims it can produce large quantities of high-quality cells in automated and robust manufacturing process suitable for cGMP environment.

- On January 8, 2022, Pluri entered into a definitive license agreement with Swiss Takeda Pharmaceuticals International AG, or Takeda. Pluri granted Takeda a global, non-exclusive license to use several patents limited to adipose fat cells only. In exchange, Takeda ceased its opposition with regards to said patents and paid Pluri a lump sum of $200,000.

- On January 10, 2022, Pluri entered into a definitive license agreement with Belgium Novadip Biosciences for a global, non-exclusive, royalty free license to use two of our patents limited to non-placental cells and cellderived therapies, sub-licensable only to Novadip’s customers.

There is no timeline from Pluri for bringing their products to market that we can find, though, when the current CEO, Yakay Yanay took office in 2019, he promised to do more than push the boundaries of science. His vision then was to generate revenue by commercializing Pluri’s breakthrough achievements.

Pluri’s bitty revenue generated over decades came in 2022 by selling proprietary lab techniques. Other income comes from collaborators, grants and awards, and selling stock. Pluri has no commercial product revenue or profit yet.

The Stem Cell Industry

Science Direct, reporting on Future Foods, assesses stem cells “cultured meat is a novel product of future food biomanufacturing and a breakthrough in the global food industry.

The stem cell market was valued at around $16.19B in 2021. Mordor Intelligence forecasts revenue will grow to $29.53B at a CAGR of 10.21% between 2022 and 2027. The stem cell market is segmented by product type, i.e., adult stem cell, human embryonic cell, pluripotent, and other types. They are used for neurological disorders, orthopedics, oncology, for treating injuries and wounds.

Asia Pacific is the fastest-growing market and North America is the largest. Personhood laws in the U. S. make it illegal to create embryos specifically for research. US researchers can use embryos from in vitro fertilization if being discarded and have been donated for research. Israel has no such prohibitive laws that appear to limit R&D and product development from placenta sttem cells.

Pluri Cash

Pluri has not generated revenue or profit from commercializing products revenue or profit. Cash it holds comes from awards and grants, from governments over the years, investments from collaborators including $30M from a Chinese VC. The U. S. National Institutes of Health and the Department of Defense funded Pluri’s work since 2016. In 2018, Japan’s Patent Office granted the company a patent for its anti-radiation or chemical therapy. In 2020, the European Investment Bank (EIB) agreed to €50M of financing to advance Pluri’s clinical development of cell therapies and severe medical conditions.

Breakthrough announcements have always driven the share price. The shares skyrocketed to $72.50 on December 3, 2007, the dropped. The share price hit $44 in 2014. Breaking news that Russia might employ tactical nuclear weapons in Ukraine sparked interest in Pluri’s claims to have a solution for acute radiation syndrome. Shares of Pluri rose to over $2.00 in the first quarter of 2022.

It completed a 1-for-10 reverse split in 2019, then the price tanked. In the past 52-weeks the low price hit bottom at $0.65. Shares climbed in the past 8 weeks closing at ~$1.34 after the board announced signing securities purchase agreements. Domestic and non-U.S. investors are supposedly purchasing 7.9M common shares at $1.03 per share for $8.2M. The next earnings report date is February 6, 2023.

Headwinds

Biotech is a risky business. From concept to successful R&D to product application to value marketing can take a generation. Peter Salk, son of polio vaccine researcher Jonas describes the cui bono in human terms. University Lab Partners describes the kind of work Pluri undertakes this way:

Biotech companies have large failure rates that create only winners or losers, not many in between. This can cause investors to add a risk factor when assessing their investments. Long timelines are unappealing to investors, as they typically want a return in 3-5 years. However, biotech companies can take 12+ years to develop a drug, or even more for a Class III device. The high cash needs of early stage biotech companies signals to investors that they will mostly get diluted in the process. This could cause them to ask for higher shares in the company if they are investing early on.

For example, Pluri’s Tnuva collaboration faces cultural obstacles to the market acceptance of cultured meat products. Can one imagine plastered across the packaged steak, MADE FROM STEM CELLS IN A LABORATORY? Then there are the headwinds to large-scale production, safety assessments, governments building a supervision system, and product-based market surveys influenced by technology challenges.

We think it will be many years before stem cell-based foods are fully incorporated into the food supply; a significant slice of the public disdains genetically modified grains and hormones in cattle and sheep.

Pluri Inc and investors got bad news this year. In March ’22, the U. S. Biomedical Advanced Research and Development Authority rejected Pluri’s request for funding anti-radiation product development “on technical considerations” and the need to “balance” its own current portfolio. Seven months later, the Biden administration announced the purchase of $290M in anti-radiation sickness pills from California company Amgen Inc (AMGN).

Another blow came in July ’22. Pluri reported its Phase 3 study for its patented use of PLX-PAD cells for the treatment of muscle injury following hip fracture surgery among 240 patients did not meet endpoints. It did provide positive indicators for improving muscle strength and regeneration.

Numbers

The stock is -28% over the last 52-weeks. It is more realistic for investors to consider the 92 share price fall over the last 5 years. It was -96% until the recent jump in share price. Amgen stock is +24.5% year to date. Year to date, Pluri’s shares rose nearly 20% in response to actions related to cash infusions rather than any product development news. It has not all been good news.

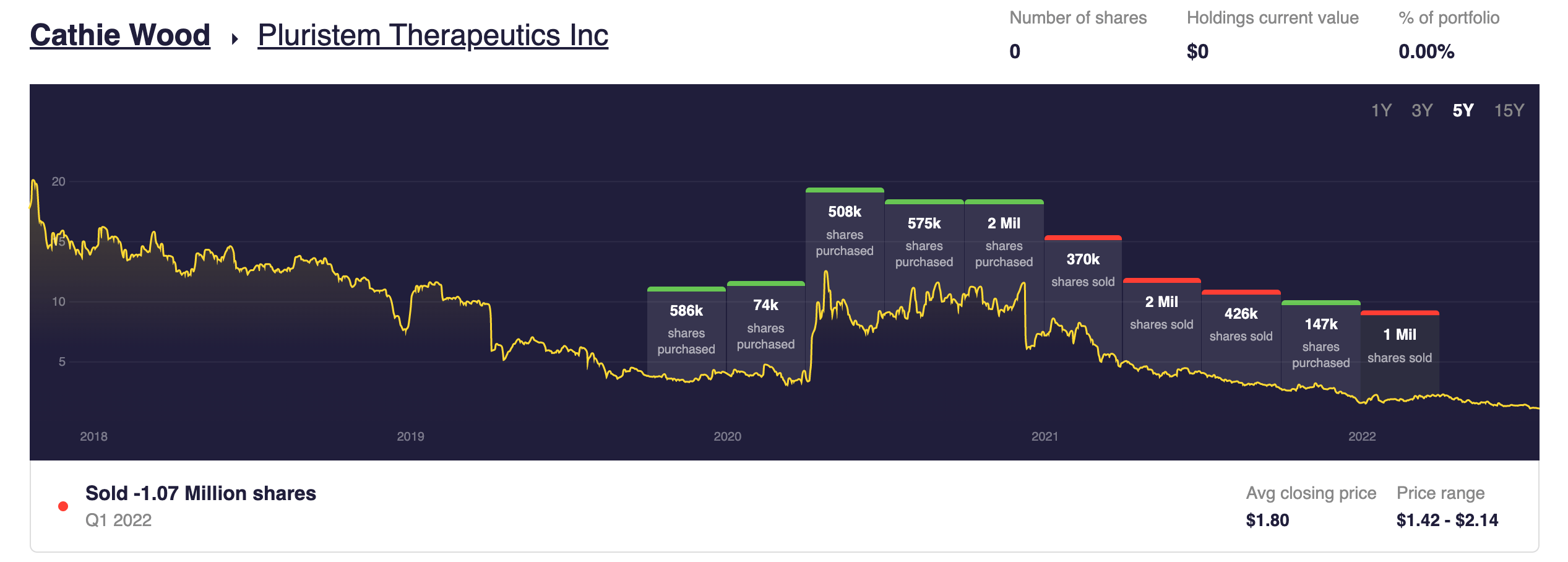

Cathie Wood and private investment equity firm Clover had short-lived flings with Pluri Inc:

CW investment in Plur (stockcircle.com/portfolio/cathie-wood/psti/transactions)

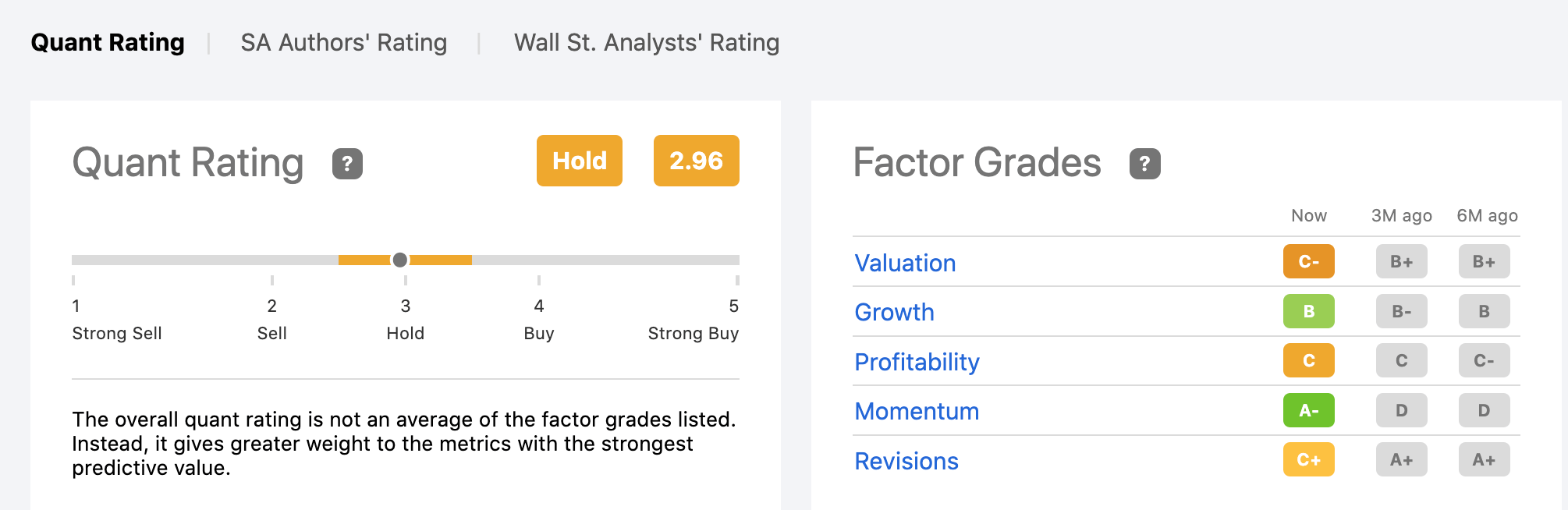

Seeking Alpha’s Quant Ratings rate PLUR a Hold and assigns a profitability Factor Grade of C, higher than its former C-, even though the company has never shown a profit and has not forecast to do so. We agree that PLUR deserves high marks for growth and momentum; unfortunately there is little news about its product commercialization or any corporate takeover.

Quant Ratings/Factor Grades (seekingalpha.com/symbol/PLUR/ratings/quant-ratings)

In 2020 and 2021, 7 hedge funds owned shares. At the end of Q1 ’22, only 1 was still holding shares. 2 more funds bought shares at an average price of $1.53 but sold $1.9K in the last quarter.

The 2 institutions owning shares include one that is a public company advisory firm; we suspect it might have taken shares in lieu of some cash payments for work on behalf of Pluri but we have no information to support that assumption. The other institution is an Israeli investment firm, Meitav Investment House that reportedly owns 167.5K shares.

In addition to Cathy Wood’s purchases and sales of PLUR, Clover Investment bought big in 2020 and sold big in 2021. A corporate insider sold ~$190K worth of shares in the last quarter.

Takeaway

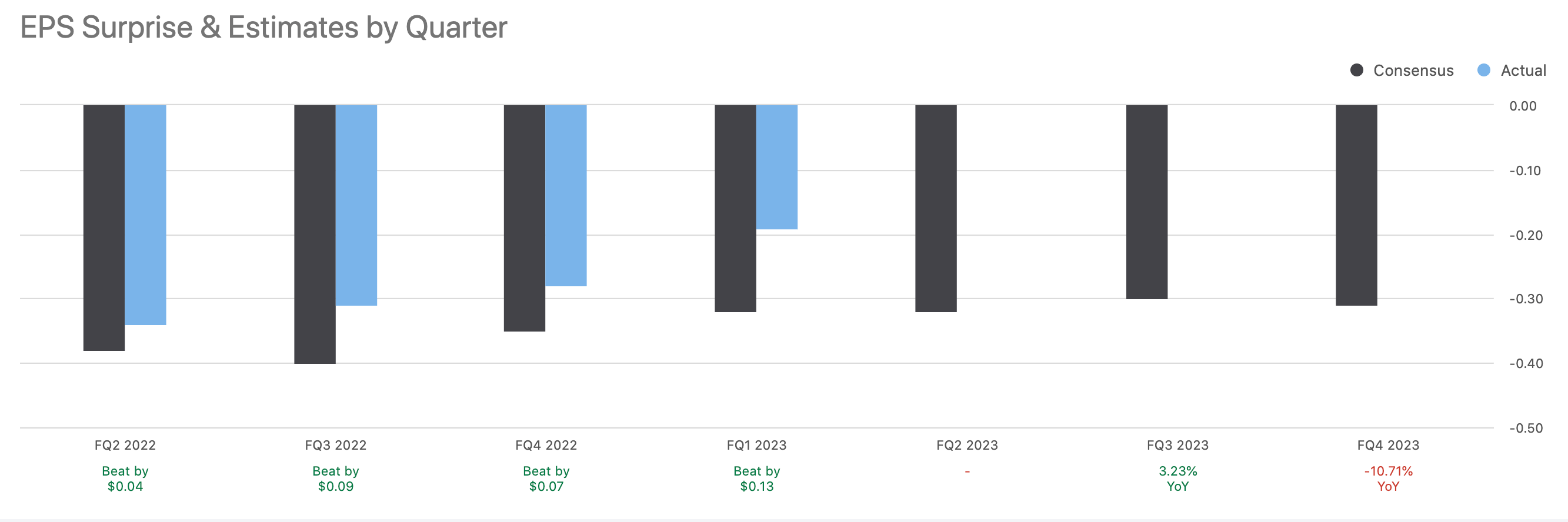

Pluri faces serious headwinds and we recommend they are too wrenching for retail value investors. Past EPS losses have been less than analysts anticipated. Yet, hope springs eternal. Yanay painted a sunny picture in the recent letter to shareholders despite Pluri having little or no hope for revenue and earnings in the near future. And, Seeking Alpha reports 4 Wall Street analysts rate Pluri a Buy.

EPS Past & Future (seekingalpha.com/symbol/PLUR/earnings)

The company has many R&D and collaborative projects underway for decades, but there are still no predictions when any one will be commercially ready. The risks are formidable from regulatory standards to competition to the company’s own financial condition. Yanay closes his letter if one reads to the end with how good 2023 looks, so “I decided to forego $375,000 of my cash salary over the next 12 months and instead receive equity grants.”

In the last SEC filing, Pluri warns

We have a history of losses and have not generated significant revenues to date. We expect to experience future losses and do not foresee generating significant or steady revenues in the immediate future. We may need to raise additional capital to meet our business requirements in the future, and such capital raising may be costly or difficult to obtain and could dilute our shareholders’ ownership interests, and such offers or availability for sale of a substantial number of our common shares may cause the price of our publicly traded shares to decline.

In our opinion, the most significant potential opportunity for investors lies in the salability of Pluri Inc’s oeuvre of patents, know-how, and data. These comprise its biggest asset class, but we have no clue their value to the medical and pharma industries, agriculture, and food manufacturers. Life must be filled with endless hope, but Like Twain quipped, sacred cows make the best hamburger.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment