Just_Super

Shares of Datadog, Inc. (NASDAQ:DDOG) have been under severe pressure in the past 18 months or so as many other growth stocks. Since the all-time high reached in November 2021, the stock is down about 63% for a market cap of about $22.5 billion. However, when the market panics and sells off indiscriminately entire sectors, it is precisely the moment when investors can identify some good bargains.

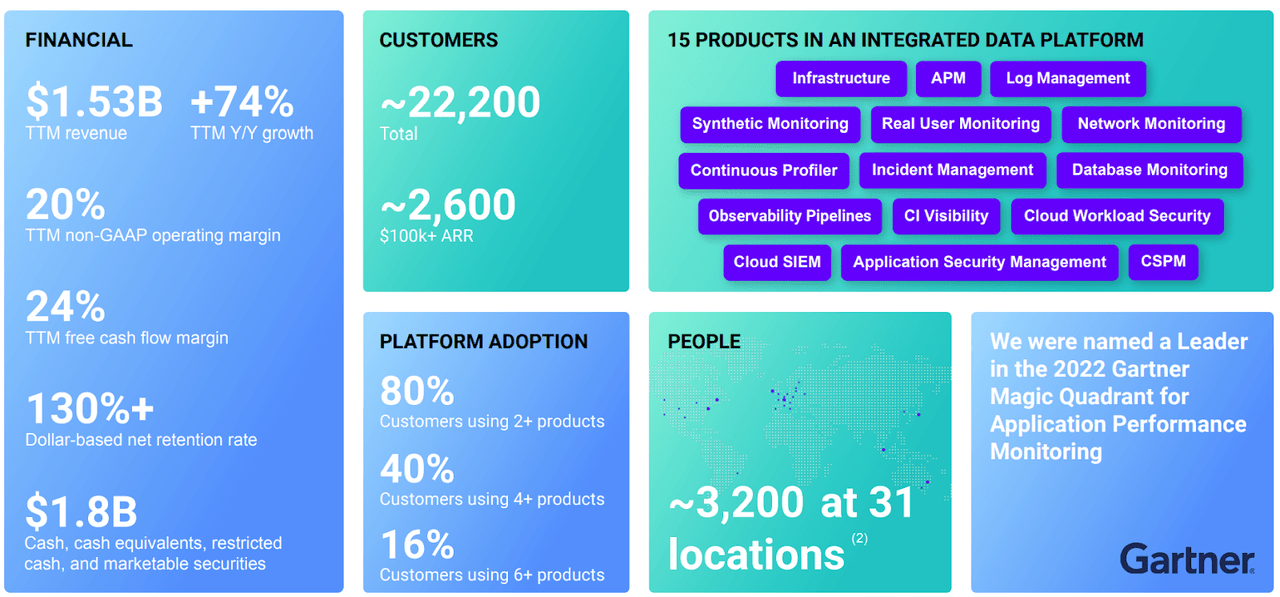

Datadog is undoubtedly a wonderful company. A leader in its field, the company was able to grow revenue at a CAGR rate of 74% per year since 2017 while also becoming Free Cash Flow positive. Today DDOG is on track to deliver about $1.65 billion of yearly Revenue while boasting an impressive 24% FCF margin. The future seems bright for the company, however, the elephant in the room, as always, is valuation. At today’s price, despite the staggering price drop, I would still not consider shares of DDOG as a bargain based on my investment framework.

Great results after years of high growth

Datadog 3Q 2022 Presentation

The company has published third quarter 2022 results on November 3, and the numbers were quite impressive. DDOG posted a revenue increase of 61.4% to $436.5 million, beating previous consensus and guidance. On a GAAP basis most metrics are still negative, while without accounting for Stock-Based Compensation the company generated Non-GAAP operating income of $74.8 million (17% margin).

On a cash flow basis, operating cash flow was $83.6 million, up 24% compared to the same quarter a year ago. Capital Expenditures were also up substantially YoY to $9.7 million (basically tripled), however in absolute terms it remains a very low and manageable number which makes it very easy to imagine a future in which cash from operations will keep growing while CapEx will remain relatively low. The result is growing Free Cash Flow: DDOG was able to grow FCF from $1 million posted in 2019, the year they went public to the current TTM value of $364 million. That is an astonishingly high growth rate, which will obviously slow down at some point, but I don’t expect it to stop any time soon.

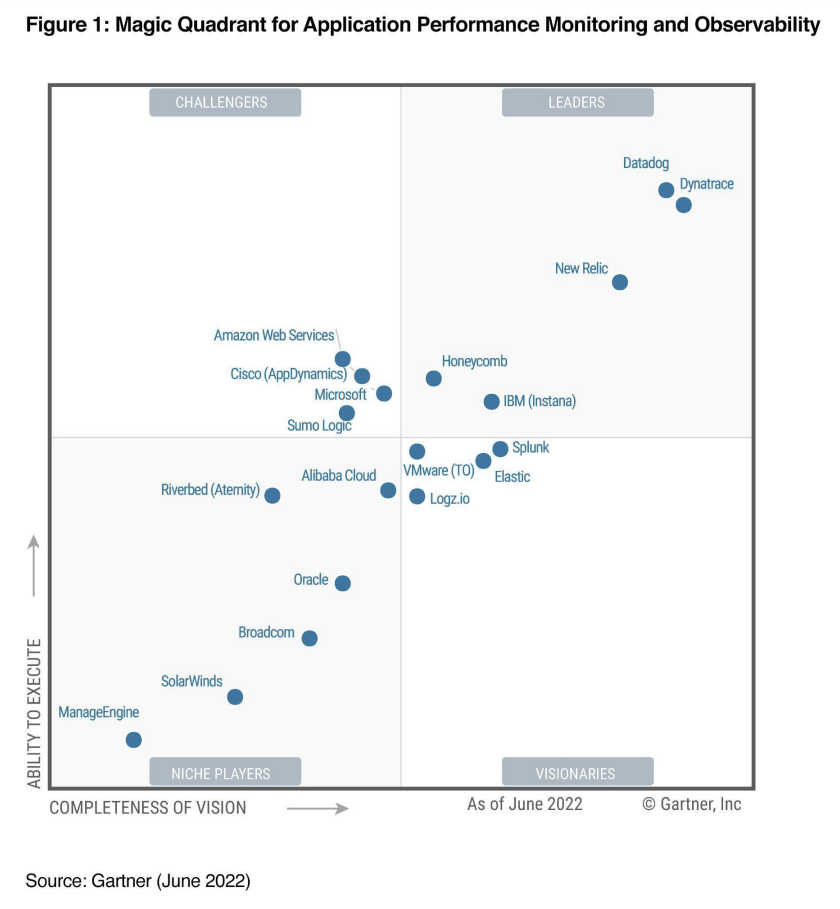

Datadog is a leader in its space, as evidenced among other things from the famous Gartner Magic Quadrant shared by the company in the latest presentation (shown below). What that effectively means is that the company is starting to reap the benefits of brand recognition which allows management to consistently reduce the need for Sales & Marketing expenses. In 2018, sales & marketing expenses represented a share of total Revenue of 45% while currently this share was cut to just 24% (TTM figure). This is a very powerful sign of the company reaching meaningful scale which will ultimately lead to higher and higher profitability in my view.

Datadog 3Q 2022 Presentation

Well managed Stock-Based Compensation is a positive surprise

As in the case of basically every tech company, Stock-Based Compensation needs to be reviewed as it often can make or break an investment thesis. DDOG increased their SBC expenses massively over the years, never below 100% YoY increase in any of the last 8 quarters. The most recent figure as per the 3Q 2022 report is for SBC to account for $101.4 million, about 23% of total revenue for the quarter. That is definitely a lot of expenses that as of now the company is able to address without incurring in cash expenses.

This however does not fully provide investors with a picture of how the practice actually impacts current shareholders; to understand that, we need to review total shares outstanding and figure out if they are increasing, diluting current shareholders. Seeking Alpha compiled data shows that Total Shares Outstanding grew in the last quarter just 1.8%, which is a surprisingly moderate amount. The rate at which DDOG is issuing new shares is actually consistently slowing down, another indication that the company is reaching meaningful scale. To me the moderate dilution seems like an acceptable price to pay for the benefit of retaining a good chunk of cash, which the company can use to invest in R&D and develop new products that customers love.

Guidance is cautious

Management’s tone in the latest earnings call was quite upbeat, having no clear and specific indication of a slowdown despite the economic uncertainties while also doubling down on new products development:

We recognize the macro environment remains uncertain. We continue to see no change to the multiyear trend towards digital transformation and cloud migration.

And we remain confident that we can help our customers with their efforts to sell on costs, drive credit engineering efficiency and take advantage of the benefits of cloud and other next-gen technologies. So we are continuing to invest in our strategic priorities to capture our long-term opportunity. We remain laser focused on bringing value to our customers as we manage through a more challenging economic environment.

The company provided cautious fourth quarter guidance of $447 million of Revenue at the midpoint, about 37% YoY growth. Management has highlighted in the call multiple times that the guidance takes into consideration the economic uncertainties, which if I have to read between the lines tells me that there is a high chance that the company will beat it. As a result, for the full year 2022 management is projecting revenue of about $1.65 billion, up 61% from FY2021. Asked by an analyst during the call, management has specified that the 4Q guidance as of now is not indicative of the company’s growth rate for the future: indications for next year will be provided during the next quarterly update.

Valuation and conclusion

Datadog is a wonderful company most likely blessed by a great future, and that is no mystery. That is precisely the reason why the stock still trades at an impressive Price to Sales ratio of 15 which naturally adds a lot of risk to a potential investment today.

As discussed before, management is projecting about $1.65 billion of revenue for FY2022. Assuming a FCF margin of 24% (consistent with the TTM value provided by the company in the latest report), that should translate to about $396 million of FCF for the year (P/FCF of 56).

I built a Discounted Cash Flow (“DCF”) model by using $396 million as a starting point. I projected a slightly more muted growth of 25% for the next 5 years and 20% for the following 5 years. Considering 10% discount and a terminal P/FCF value of 15, the current implied value for the stock would be $22.3 billion, perfectly in line with the current market cap.

I honestly have no problem imagining a world in which Datadog is able to hit this projected growth, and as such the stock might be positioned today for a 10% yearly return (minus a bit of dilution due to SBC which should be accounted for). In my point of view however there is not enough margin of safety for an investment as the current valuation implies a massive downside risk in case the company does not flawlessly execute. Lower prices will obviously make the thesis a whole lot better but those could also never materialize. That is investing. At the same time DDOG seems to be a great candidate for a small, speculative bet in a well-diversified portfolio: as always, position sizing matters a lot.

Be the first to comment