Otakeja/iStock via Getty Images

KLX Energy Services (NASDAQ:KLXE) is coming off a solid quarter, with all its segments performing well, led by its Northeast and Mid-Con segment. It improved on both its top and bottom lines, and if the market continues to be up, I think it’s going to maintain momentum in 2023.

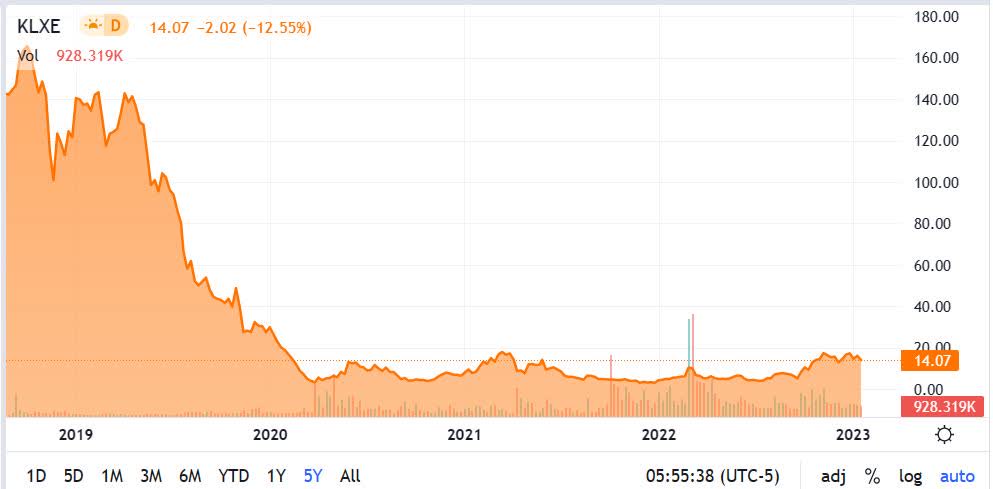

The major question that has yet to be answered is whether or not this assumption is already priced into the stock. Looking at a two-year chart, the company has failed to break through the $18.00 per share mark, which it traded at on March 16, 2021, and has bumped up against, but failed to break through, several times since early November 2022.

With guidance for the fourth quarter being flat on the top and bottom lines, if that is how it performs, it’s probably going to continue trading in the current range of about $13.00 per share to $17.50 per share it has traded at over the last couple of months.

TradingView

On the other hand, if there is a surprise to the upside, it’ll likely sustainably push past the $18.00 share price level, if it’s accompanied by positive guidance for 2023.

Since its operators and customers hadn’t provided the company feedback for 2023 as of its last earnings report, there isn’t the visibility yet concerning the level of activity expected for this year. Until that happens, and the next earnings report is released, the company will continue to trade sideways, in my opinion.

With the clarity management has at this time, they’re leaning toward momentum continuing going forward, but it needs to be confirmed before modeling the next year.

In this article we’ll look at its latest earnings report and whether or not momentum is likely to continue in the quarters ahead.

Some of the numbers

Revenue in the third quarter of 2022 was $221.6 million, compared to revenue of $139.00 million in the quarter ended October 31, 2021, a gain of $37.2 million, or 20.2 percent. Revenue in the first nine months of 2022 was $558.3 million, compared to revenue of $341.7 million for the nine-month period ended October 31, 2021.

The increase in revenue was attributed to an increase in pricing across its core service offerings and higher utilization across its drilling, completion, production and intervention activities, along with reduced white space.

Based upon its product lines, completion accounted for 52 percent of revenue in the quarter; drilling, 26 percent; production, 12 percent; and intervention, 10 percent.

Adjusted EBITDA in the third quarter of 2022 was $37.1 million, and adjusted EBITDA margin was 16.7 percent. Adjusted EBITDA margin was up 113 percent sequentially in the quarter.

Net income in the reporting period was $11.1 million, or $0.96 per share, compared to a net loss of -$(18.8) million, or -$(2.19) per share in the quarter ended October 31, 2021.

One expense that continues to hang over the company is its $2.1 million lease associated with its coiled tubing packages leased in Q4 of 2019. As management mentioned, this has an impact on its comparison to its peers.

Free cash flow in the third quarter of 2022 was $11.1 million.

Cash and cash equivalents at the end of the third quarter of 2022 was $41.4 million, compared to cash and cash equivalents of $28.00 million at the end of the quarter ended October 31, 2021. The company has another $45 million in liquidity from its ABL facility.

The increase in cash was from $18.5 million in positive operating cash flow, monetization of $5.3 million in obsolete assets and non-core real estate, and $1.6 million in share sales, partially offset by an extra payroll cycle in the reporting period.

At the end of the third quarter of 2022 the company held $296.6 million in total debt. As of the end of the third quarter the company had a net leverage ratio of 1.7x.

Performance by segment

Northeast and Mid-Con segment

Revenue in the third quarter of 2022 from its Northeast and Mid-Con segment was $86.6 million, up $15.3 million from the previous quarter. The increase in revenue was attributed to improvements in coiled tubing, directional drilling, fishing, pressure pumping and rental services across its regional footprint.

Adjusted operating income in the third quarter of 2022 was $17.2 million, compared to adjusted operating income of $7.4 million in the second quarter of 2022. Adjusted EBITDA came in at $21.3 million in the reporting period, compared to adjusted EBITDA of $11.1 million in the prior quarter. The boost in activity and pricing, which led to wider margins in the product lines mentioned in revenue, were the catalysts behind improved profitability in the segment.

With Northeast and Mid-Con being the largest segment, how it does going forward is going to have a significant impact on the performance of the company. While management expects growth to continue, the lack of clarity from its customers has resulted in the company guiding for a flat performance in the near term. Longer term it should enjoy incremental growth in 2023, if economic conditions cooperate with it.

That said, I think it’s going to take a solid performance for the stock to break out past its ceiling.

Southwest segment

Revenue in its Southwest segment was $68.5 million in the third quarter of 2022, up 14 percent from the prior quarter. That largest increase in revenue came from coiled tubing, rental and wireline.

Adjusted operating income for the Southwest segment was $5.6 million, up $1.8 million sequentially. Adjusted EBITDA in the third quarter was $10.2 million, compared to adjusted EBITDA of $6.4 million in the previous quarter.

Rocky Mountains segment

Revenue from its Rocky Mountains segment was $66.5 million, up $13.4 million, or 25 percent sequentially. The boost in revenue sequentially came from an increase in pricing and activity across DJ Basin, Wyoming and Bakken, with coiled tubing, fishing, rental and wireline leading the improvement. Adjusted operating income in the third quarter of 2022 was $12 million, compared to $4.1 million in the second quarter of 2022. Adjusted EBITDA was $17.3 million in the reporting period, compared to adjusted EBITDA of $9.3 million in the second quarter. The improvement in profitability was for the same reasons as the increase in revenue.

Expectations that pricing power should remain in place in 2023, the Rocky Mountains segment should also help the company maintain growth momentum in the quarters ahead, assuming the recession doesn’t surprise to the downside.

Conclusion

For the fourth quarter of 2022, the company guided for revenue and adjusted EBITDA to be relatively flat, with revenue possibly being slightly up.

Concerning 2023 guidance, the company is holding back because its customers and operators haven’t given guidance input in regard to whether or no activity is going to increase in 2023, or to what level.

That said, management believes it’s probably going to increase over the next year or so, primarily on assumptions concerning the market remaining up, continued pricing power, and another 50-plus rigs in 2023. Based upon its run rate, it appears the company is likely to maintain momentum going forward.

I like the performance in the last quarter, but according to guidance for the fourth quarter, it appears the stock is probably going to be somewhat flat in the near term.

Assuming the market remains up in 2023, the company is positioned well to compete. It has increased materials and components to mitigate supply chain constraints, improved its balance sheet, and is poised to add over 50 more rigs in 2023.

On the other hand, if the market doesn’t perform as expected, or macro-economic factors come into play, it could be a tough year for the company, especially with CapEx being increased, which if revenue is down, will result in its bottom line being under pressure.

Looking at the performance of its share price over the last couple of years, and seeing that it has hit a ceiling at approximately $18.00 per share several times, it’s going to have to generate some decent numbers in order to break out, especially have soaring from a 52-week low of $3.64 per share on July 14, 2022, to its 52-week high of $18.63 per share on November 11, 2022, before pulling back to trade at about $14.00 as I write.

Until there is more clarity concerning activity in 2023, the stock is going to continue to trade rangebound. It’s not trading at a bad price at this time, but it’s still elevated when considering the lack of visibility in the market. It could easily go either way depending on its fourth quarter numbers and activity guidance for the year.

For those reasons, I would wait before taking a position until there is more clarity, and/or the share price corrects to levels that offer a better risk/reward scenario.

Be the first to comment