Editor’s note: Seeking Alpha is proud to welcome Douglas McKenny as a new contributor. It’s easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Pgiam/iStock via Getty Images

Global advisory-focused investment bank, PJT Partners Inc. (NYSE:PJT), has richly rewarded its investors over the last five years. In the last five years, the share price has appreciated over 60%, compared to more than 40% for the S&P 500. That excellence has been driven by strong fundamentals, fundamentals that were challenged in 2022, hitting the share price. However, a review of the company’s business drivers shows that the firm’s business model rests on strong, underlying trends. Firstly, global M&A activity is likely to remain strong, given the importance of M&A to value creation. Secondly, global bankruptcy and restructuring activity tends to counteract what is happening in the M&A world. This reduces risks in the company’s business model. Thirdly, the company has invested heavily in its staff, who are some of the best paid professionals in the industry. This investment allows the firm to enrich and widen its offerings. With these three remaining intact going forward, PJT Partners is likely to continue to do well on the market. Investors should consider having it in their portfolio.

Enviable Stock Market Performance

In the last five years, PJT Partners has gained 62.55%, compared to 42.3% for the S&P 500.

Source: Google Finance

In 2022, the company still managed to outperform its benchmark, despite declining 0.69%, compared to a decline of 19.95% for the S&P 500.

Source: Google Finance

The decline in stock market performance reflects the decline in fundamentals in 2022, and the challenging economic environment that year.

Strong Financial Performance

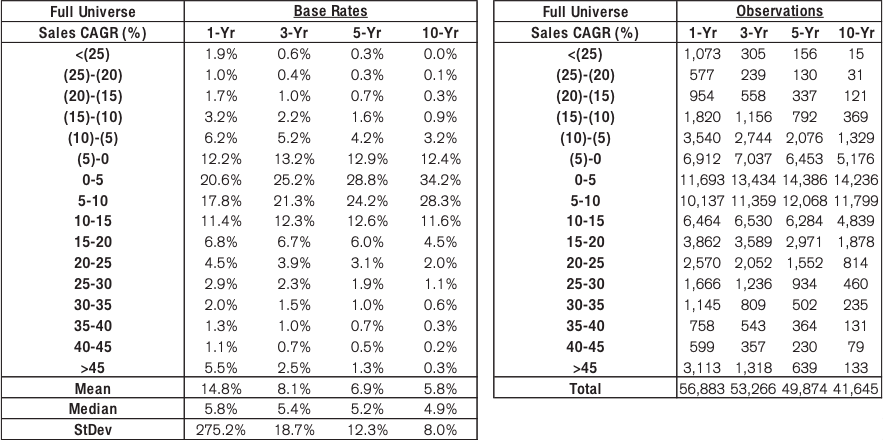

In the last five years, revenue has risen from $499.28 million in 2017, to $991.95 million in 2021, at a 5-year revenue compound annual growth rate (CAGR) of 14.71%. According to Credit Suisse’s “The Base Rate Book”, 12.6% of firms between 1950 and 2015, had a similar rate of growth.

Source: Credit Suisse

In the trailing twelve months (TTM), revenue rose to over $1 billion, despite significant headwinds in global M&A activity. This was a great demonstration of how the company’s quality is able to see it through even during periods of economic difficulty.

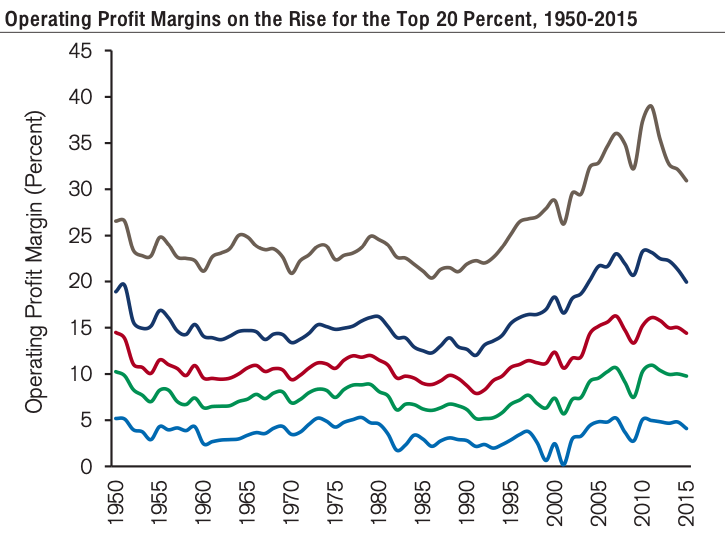

Operating income rose from $10.05 million in 2017, to $219.45 million in 2021, at a 5-year operating income CAGR of 85.28%. operating income declined somewhat in the TTM period, to $216.32 million. Meanwhile, operating margin rose from 2.01% in 2017, to 22.12% in 2021. In the TTM period, operating margin declined to 20.43%. This places the company’s operating margin among the top tiers in America.

Source: Credit Suisse

Net income rose from -$32.55 million in 2017, to $106.17 million in 2021. In the TTM period, net income declined to $100.86 million.

Return on invested capital (ROIC) rose from 1.6% in 2017 to 17% in 2021. In the TTM period, ROIC declined to 16.7%.

PJT Partners has grown free cash flow (FCF) from $110.15 million in 2017, to $117.69 million in 2021, at a 5-year FCF CAGR of 1.33%. In the TTM period, FCF jumped to $264.47 million.

The Business Model

PJT Partners’ genealogy can be traced to 2013, when Paul J Taubman founded PJT Capital LP. In 2015, the partnership combined with spin offs of alternative investment management firm, Blackstone Inc. (BX). These spinoffs were the financial and strategic advisory, and restructuring and reorganization advisory services and Park Hill Group arm of Blackstone. The combined entity listed on the New York Stock Exchange in October, 2015.

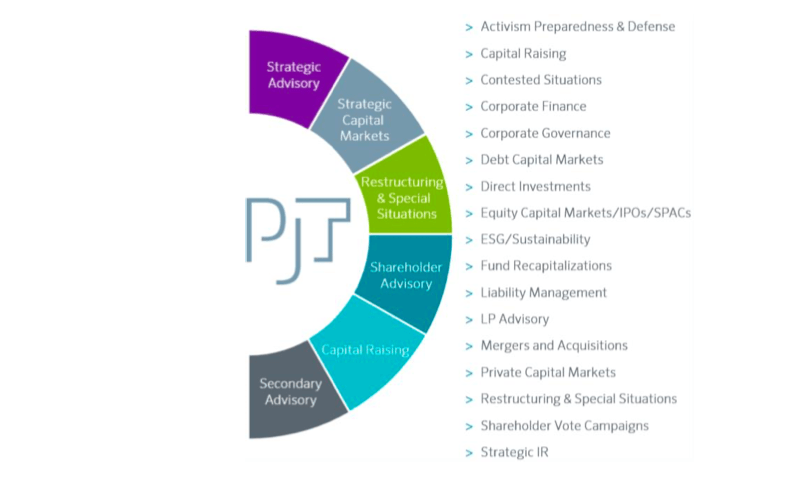

PJT Partners provides a wealth of services to its clients, namely, strategic advisory, capital markets advisory, restructuring and special situations and shareholder advisory services to corporations, financial sponsors, institutional investors and governments, and private fund advisory and fundraising services for alternative investment strategies. PJT Park Hill is responsible for the alternative asset advisory and fundraising services.

Source: PJT Partners 2021 Form 10K

Business Drivers

The company’s long-term results are driven by their ability to enrich and expand its advisory services. That, in turn, is a function of the state of the economy and the company’s ability to recruit and retain the best advisors in the world.

Global M&A Activity

In its history, PJT Partners has done more than $750 billion worth of M&A deals, and more than $850 billion worth of liabilities restructuring. PJT Partners has also raised more than $195 billion worth of capital. The company’s success is, I believe, grounded on the secular strength of the global M&A activity. An overview of global M&A activity will highlight this.

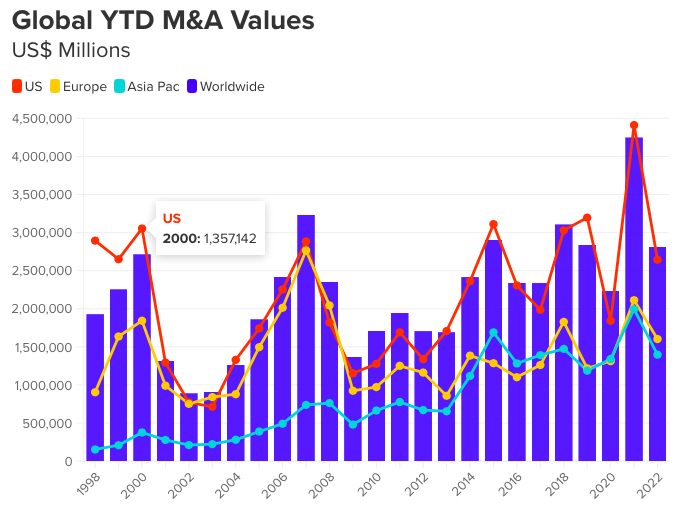

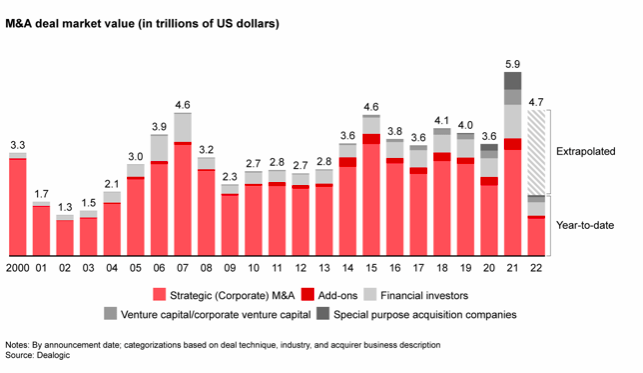

While 2021 was hailed as “the year of M&A”, with $5.9 trillion worth of global M&A activity, the value of deals in 2022 is likely to be lower.

Source: Refinitiv

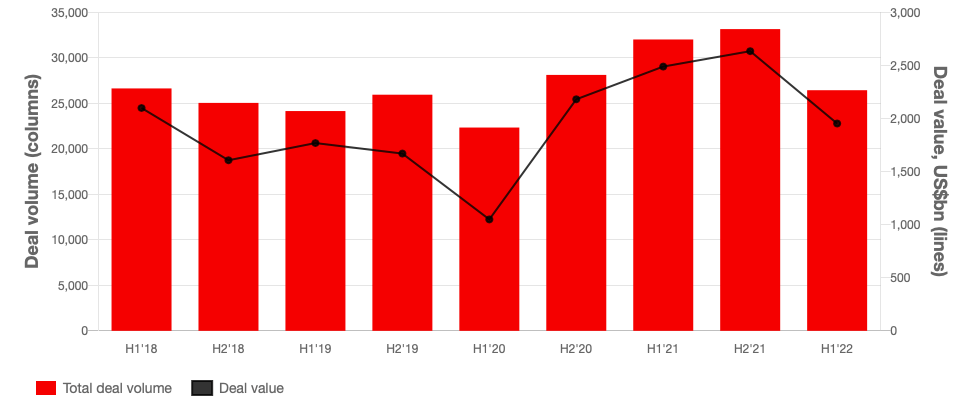

In the first half of 2022, the value of M&A deals was down 21% compared to the same period in 2021, at $2.2 trillion. Not only did the value of global M&A activity decline, the volume of the same did as well, declining 17% compared to the same period last year.

Source: PwC

Importantly, as a result of the decline in value and volume of M&A activity, investment banking profits across the board declined. In January 2022, a 16-month run of global investment banking fees in excess of $10 billion was ended. In 2022, as of October, only March and June had fees in excess of $10 billion, with September achieving half that.

This goes a long way in explaining the decline in PJT Partners share price in 2022. Nonetheless, global M&A activity remains in line with healthy, pre-pandemic levels. Indeed, when you zoom out, it is clear that 2022 is still likely to be one of the strongest years for global M&A activity, despite the declines in 2022.

Source: Bain and Company

In 2023, many of the drivers of M&A activity will be weaker. With rising interest rates, dealmakers will be more cautious about the value and volume of deals they do. However, this could increase the number of distressed sellers, shoring up volumes. Many firms will look to divest themselves of non-core assets in order to sanitize their balance sheets. Although transformational deals are unlikely, technology-driven disruption deals will remain or possibly gain strength.

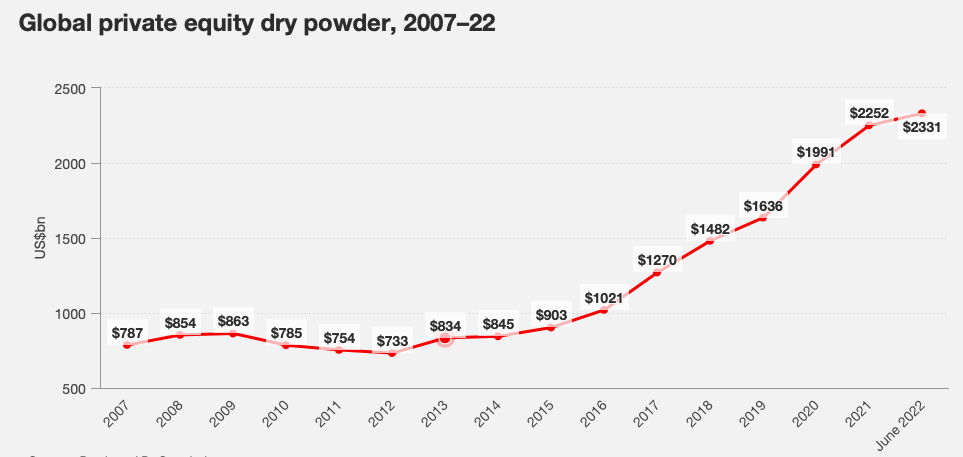

M&A will remain an important part of value creation strategies, and so, the odds of a truly catastrophic collapse in global M&A activity remain low. Not only is M&A an important part of a business’ value creation, there is financial support for such activities. The growth of global private equity dry powder over the last fifteen years has provided M&A with a reliable source of capital for dealmaking.

Source: PwC

Global Restructuring Activity

Global restructuring activity in 2022 remained low, continuing a post-pandemic decline, as a result of the low cost of capital, high valuations, and strong consumer demand. In addition, the effects of direct government liquidity support for businesses, and monetary policy, have given life to businesses that would otherwise have been forced to restructure. Furthermore, with private equity dry powder, and capital from special purpose acquisition company (SPAC) IPOs, there has been ample capital to shore up struggling businesses.

Source: PwC

With the decline of SPACs, one source of life support for zombie companies has been weakened. Rising interest rates will make investors more careful about the kinds of deals they do, and this should force more businesses to restructure. Thus, we are likely to see a rise in bankruptcy filings in 2022 data, and this number is likely to increase in 2023, as interest rates rise, inflation takes hold, and valuations are compressed. With renewed Covid-19 uncertainty from China, there are even more reasons to believe that 2023 will see a rise in global restructuring activity. However, this may not be a very high rise, given that governments have shown an appetite to support businesses in the past. So, while an increase in global restructuring activity and bankruptcies can be expected, this will not be a tidal wave of new activity.

The Global Fight for Talent

While broad economic trends are important, they are, in a sense, meaningless: PJT Partners competes against a huge number of investment banks from across the world. Competition is a loser’s game. Faced with competition, any firm will find it hard to exert pricing power on the market. Competition means that there will be a fight for essential resources, and in the world of investment banking, that essential resource is talent, and the price of talent is rising with each year.

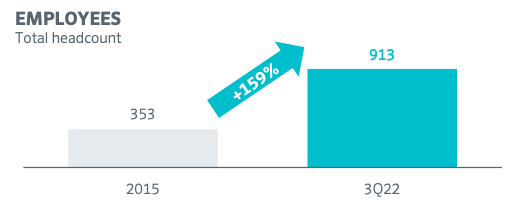

PJT Partners has responded by offering the best pay for first year analysts and having, overall, one of the best compensation offerings in the industry. In 2022, average compensation at PJT Partners was nearly $800,000, with pay going up 12% that year, while rivals pulled back compensation expenditure. Indeed, compensation and benefits have risen from $391.5 million in 2017 to $640 million in 2021, at a 5-year compensation and benefits CAGR of 10.33%. The rise in compensation and benefits is a result of the firm hiring more people in order to enrich and widen their services. In fact, PJT Partners has grown its total headcount from 353 in 2015 to 913 in Q3 2022, including 105 partners in the United States, Europe, and Asia.

Source: October 25 Investor Presentation

Compensation and benefits make up around 80% of total expenses. In 2017, compensation and benefits ate up around 78% of revenues, but this declined to 64% in 2021, as efficiencies improved.

Due to the high average compensation levels, PJT Partners has its pick of the industry’s most sought after talents, with big firm capabilities and the feel of a small firm. The firm employs feedback from its workers to improve their conditions. In one survey, an employee responded that, “I feel an intense sense of ownership and that what I do every day actually contributes to the success of the firm”, while another said, “PJT is a modern forward thinking company that does well by its employees”.

Risk

The thesis is predicted on global activity remaining within the bounds of what is normal. Yes, the global economy looks as if it will struggle in 2023, but, global M&A activity will remain in line with pre-pandemic activity, and results will be supported by any increase in bankruptcy and restructuring. Consider 2019, for instance, when global M&A activity declined, but bankruptcy filings increased. Or 2020; when global M&A activity declined further, but bankruptcy filings increased. It is hard to imagine the conditions under which that relationship could be broken. If such conditions exist in a meaningful way, they could be that the growth in value of bankruptcy and restructuring business is much smaller than the decline in value of M&A activity. This is possible if larger businesses avoid bankruptcy and restructuring. While there has been a lot of talk about zombie companies, the idea that there is a sizable group of companies who are existing despite being unprofitable and debt-ridden has not really been tested.

The real question is probably whether business continues to accrue to PJT Partners. The company has placed itself at the head of the queue for talent. Nobody pays better than PJT Partners. While the company has had issues, such as the “3am email” in which a Vice President in Asia suggested that their US-based staff be up at 3am when they were, it has a reputation for being a great place to work. It is the quality of the work that the staff does that makes PJT Partners attractive to its clients. Above that is the PJT Partners brand. Clients go to the company because they believe they are dealing with one of the best advisory-focused investment banks in the world. If something changed to tarnish the company’s brand, that would impact its ability to draw in clients. At present, there are no suggestions that there are problems with staff, or the company’s attractiveness to new talent or clients. These are more long-term risks than they are immediate.

The question reverts back to broader economic questions. If the balance of global M&A and bankruptcy and restructuring activity is outside the norm, then PJT Partners will be in some trouble in the near-term. That is the most pressing question for the company.

Valuation

On a relative basis, PJT Partners is trading at a price-earnings multiple of 19.24, compared to 19.97 for the S&P 500. On the face of it, that suggests that there is no margin of error for investors. However, with $264.47 million in FCF in the TTM period, and an enterprise value of $2.86 billion, the company has a FCF yield of 8.6%, compared to the FCF yield of 2.1% of the 2000 largest firms in the United States, according to New Constructs. Thus, there is a meaningful margin of safety available to investors, and a signal that future stock market performance will be strong.

Conclusion

PJT Partners has established itself as a premier global advisory-focused investment bank. Thanks to the significant investment that the company has made in spending on talent, it is able to offer a rich range of services to its clients, and attract business even during down periods, as we saw in 2022. That strength is likely to remain. Although global M&A activity will probably decline in 2023, that should be counterbalanced by a rise in global restructuring activity and bankruptcies. Thus, PJT Partners is a good defensive stock to have in a period of economic uncertainty.

Be the first to comment