grandriver/iStock via Getty Images

Pioneer Natural Resources (NYSE:PXD) produces mostly shale-focused hydrocarbons. The company has been witnessing revenue increase at a pace that is relatively high in recent times, owing to the high oil prices in the past few years. On the other hand, production has largely been flat during the period, as increasing oil prices made up for the lack of production. The current projections by management also state that in the next quarter, the company will only slightly increase output, which may put further pressure on revenue. This means if realized oil prices are much lower, and unless oil prices head back up the company could see revenue moderate in 2023, and that would put pressure on valuations, and could see the stock sell off.

Where Are Oil Prices Headed?

In order for Pioneer to continue its rate of growth it will either have to improve its realized price per barrel of oil, or it will have to increase production. The company currently has around 2.2 billion in reserves and is expected to continue production of around 360-380 BOPD in the coming quarter. I expect that number could jump to 400k BOPD in 2024, on average, but it may not be enough to keep revenue growing.

The current price of oil (WTI), is hovering around $80 a day, and that number may increase as demand increases from China’s reopening, pushing prices up. Global oil production averaged around 99.9 million BOPD, in 2022. 99.9 is below the 100.8 estimates by analysts earlier, and in 2023, estimates are that oil demand will grow by another 1.5-1.7 million BOPD mainly due to consumption from China, India, and the Middle East. But, the oil supply may not increase by any significant amount, which works out in favor of oil producers. Despite the deflationary headwinds from numerous sources including the rising dollar, and a flat or decreasing level of money supply, prices are likely to head back up. Plus, there are a number of factors including peak oil that are affecting the price of oil. Meanwhile, American shale is in no position to increase its own capacity, for the year by any significant amount, owing to CAPEX schedules, and limitations stemming from the capital-intensive nature of shale production.

In addition, OPEC and specifically Saudi Arabia are consistently targeting higher oil prices. And have been willing to cut production as well to ensure as much. Oil inventories in the US have been increasing in recent times, and this has led to oil prices remaining rangebound. But inventories may slowly start to decline, as global demand continues to increase.

“While lower oil prices come as a welcome relief to consumers faced by surging inflation, the full impact of embargoes on Russian crude and product supplies remains to be seen,” the IEA said. “As we move through the winter months and towards a tighter oil balance in the second quarter of 2023, another price rally cannot be ruled out.”

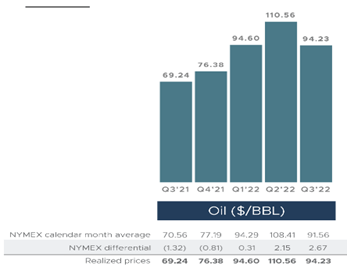

Pioneer Natural Resources remains relatively hedged out, in terms of oil, which limits the downside but had been realizing oil prices at levels that are usually quite high. This means that, since oil prices have come down revenue is likely to come down as well until prices recover.

Realized Prices (Investor Presentation)

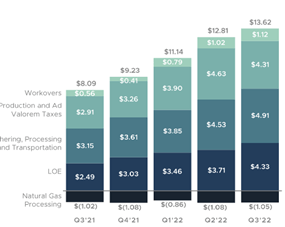

Meanwhile, as revenue moves towards moderation, costs have continued to rise every quarter, and next quarter could see costs increase to $14 or thereabouts, which would mean there would some pressure on the company’s finances.

Cost Structure (Investor Presentation)

China Reopening:

Chinese crude demand is expected to increase by 410-510,000 bpd. This is partially due to the reopening of the economy and partially due to increasing demand. China’s economy will face headwinds, as global trade slows, but local consumption has been increasingly replacing global consumption, which drove GDP in past. Therefore, it could very well be that China does not face any real decline even if the global economy slows. China has its own problems though, especially due to excessive debt, that could hamper demand.

Valuation In Terms Of The Current Outlook

Should oil remain rangebound the forward P/E is likely heading towards 10-11, at which point it would still be cheap. Should oil prices start to rise once again the combination of increasing oil prices and increasing supply could see a small increase in revenue, mostly a single-digit, increase in 2023. This would still push the forward P/E to around 6x earnings, which would translate into the cheap being inexpensive.

While recessionary sentiments continue to loom along with a deflationary background, the combination of falling inventories, increasing production, and improving prices could push valuations into value territory.

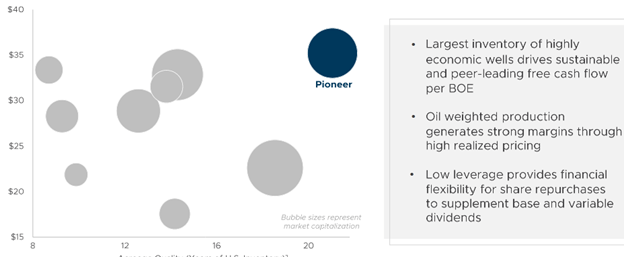

PXD’s efficiency relative to competitors (Investor Presentation)

But risks remain, oil demand could come down for the year as high-interest rates, slowing savings, and weight on consumption, lead to a slowdown in demand for oil. Even if oil prices go up the headwinds from the current economic environment make it likely that they could well fall back down as consumers may not be able to sustain prices around $100.

2023 is currently looking slightly favorable for Pioneer, as current valuations, and a high return on capital, continue to likely lead to a strong cash flow. This means that even in deteriorating conditions the lean nature of Pioneer’s operations means plenty of cash will keep coming. This could make the stock interesting for investors, especially those looking for a company that has high levels of dividends. In fact, the dividend yield being around 10.7% means that alone could send the stock slightly higher.

Pioneer has strong long-term fortunes regardless of what happens in the short term. Their assets are efficient, and their costs are likely to stop rising as quickly as they did previously. Should oil head back towards $90, investors may consider taking a position. On the other hand, if prices remain rangebound, then it could be a case where holding the stock would be more prudent.

Be the first to comment