NicoElNino

A Quick Take On ExlService Holdings

ExlService Holdings (NASDAQ:EXLS) reported its Q3 2022 financial results on October 27, 2022, beating revenue and EPS estimates.

The firm provides a range of IT services and business process management services to companies worldwide.

EXLS is exposed to several less cyclical industries, so a downturn may affect its trajectory less than others.

For that reason, my outlook on EXLS is a Buy at around $170 per share.

ExlService Holdings Overview

New York, NY-based ExlService Holdings was founded in 1999 to provide a range of outsourced digital operations, claims processing and data analytics through its insurance, healthcare, analytics and emerging business segments.

The company is led by co-founder and CEO Rohit Kapoor, who previously was Business Head at Deutsche Bank and Vice President at Bank of America.

ExlService’s primary service offerings include:

-

Business Process Outsourcing [BPO] Services

-

Analytics Services

-

Technology Solutions

-

Digital Transformation Services

-

Care Management

-

Customer Acquisition Software

The firm acquires customers through its direct sales, marketing & business development efforts and through a variety of channels, including digital and traditional marketing campaigns, webinars, lead generation activities, affiliate programs, word of mouth referrals, and events.

Additionally, the company has partnered with other service providers to expand its reach in different markets and industries.

ExlService Holdings’ Market & Competition

According to a 2021 market research report by Grand View Research, the global market for business process outsourcing was an estimated $232 billion in 2020 and is expected to reach $446 billion by 2028.

This represents a forecast 8.5% from 2021 to 2028.

The main drivers for this expected growth are an increasing usage of digital tools and delocalized talent to maximize business efficiencies.

Also, the versatility of outsourcing services is increasing as other types of service process automation and intelligence adds to return on investment for enterprises.

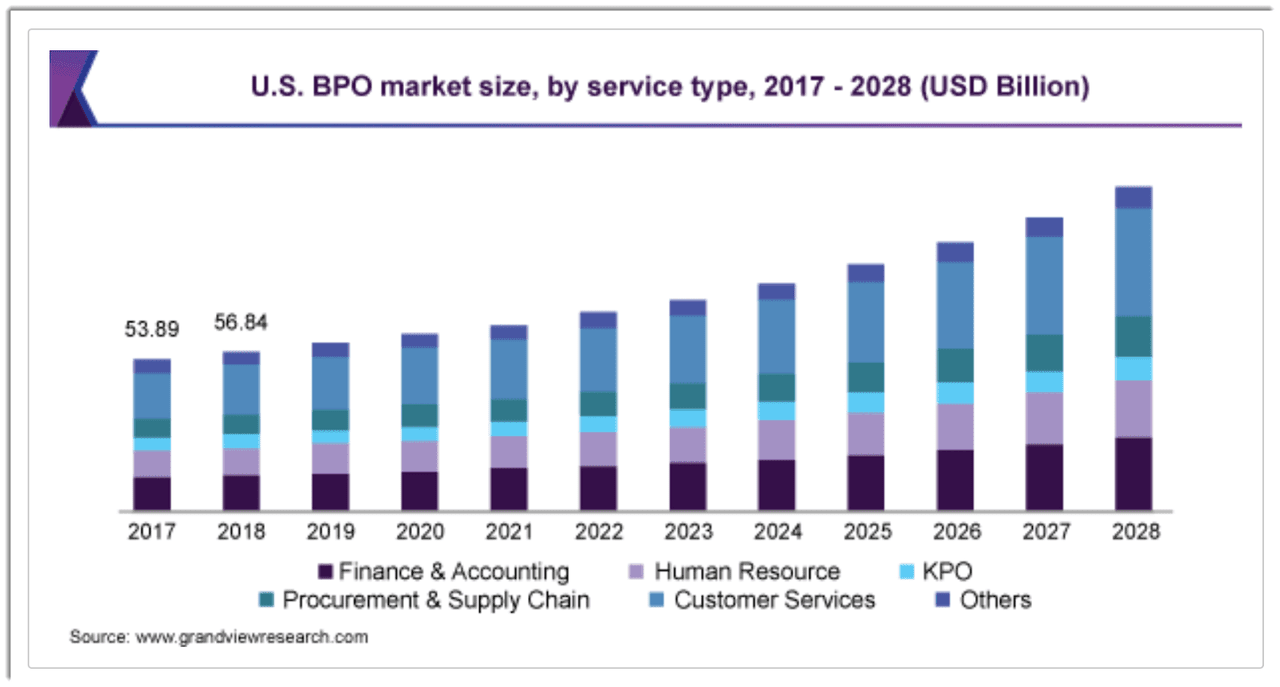

Below is a chart showing the historical and expected future growth trajectory of process outsourcing services in the U.S.:

U.S. BPO Market (Grand View Research)

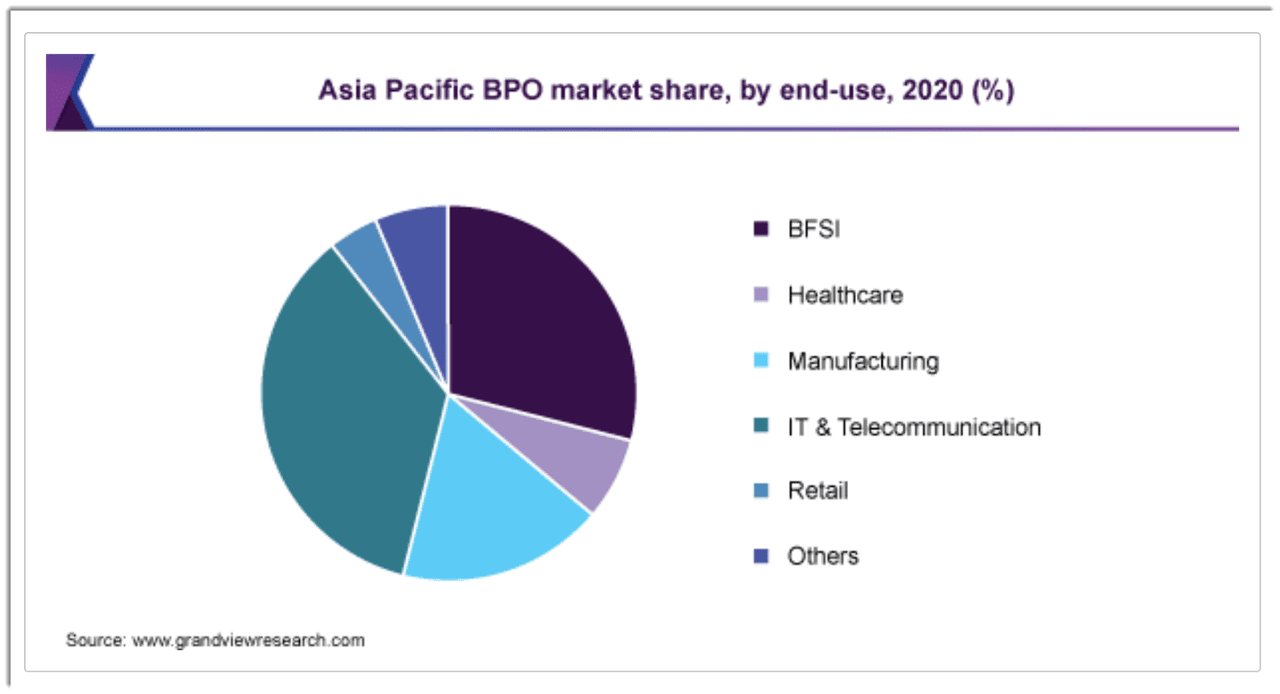

The Asia Pacific market is forecast to see the highest CAGR from 2021 to 2028 and the chart below indicates the breakdown of that market by end-use industry in 2020:

Asia Pacific BPO Market (Grand View Research)

The company also operates in the business process management industry, which was a $10.6 billion industry in 2020 and is forecast to reach $26 billion by 2028, representing an expected CAGR of 12.0% from 2021 to 2028, according to a Fortune Business Insights research report.

Notably, AI-enhanced business process management services are expected to emerge as a major trend in the BPM industry over the coming years, as it has the promise of providing further insights into generating business process efficiencies across organizations and their ecosystems.

ExlService Holdings’ Recent Financial Performance

-

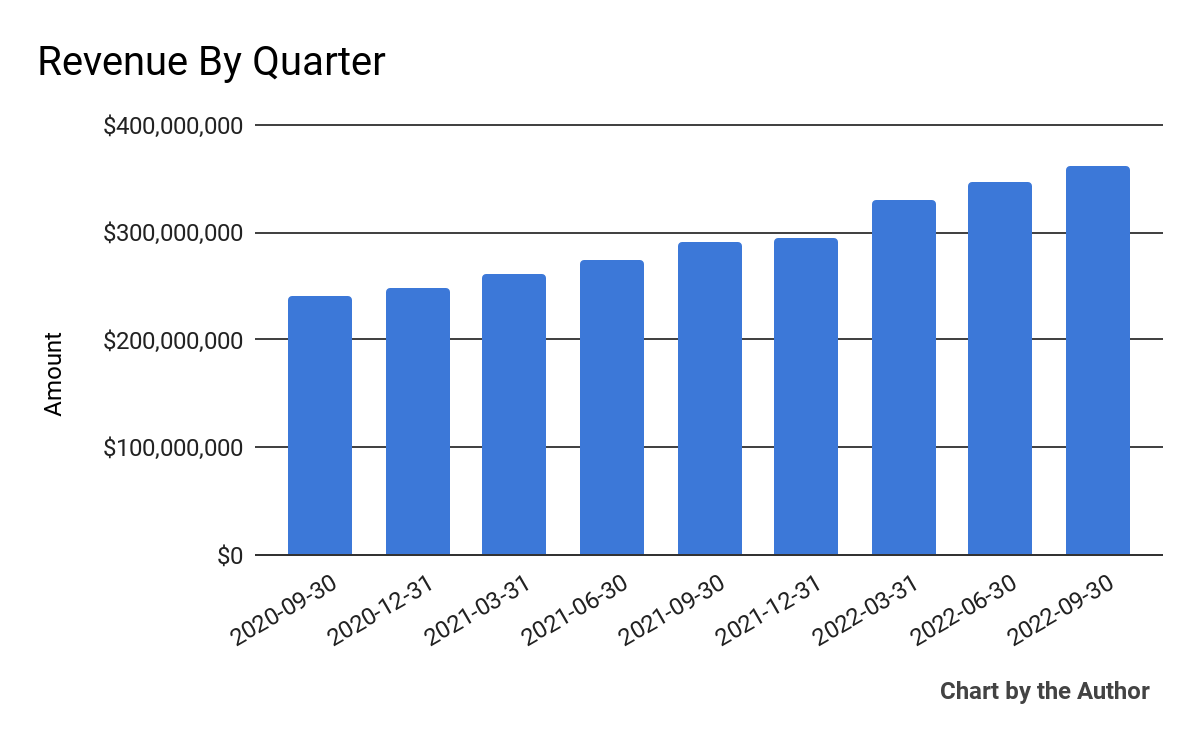

Total revenue by quarter has risen steadily in recent quarters, as shown below:

Total Revenue (Financial Modeling Prep)

-

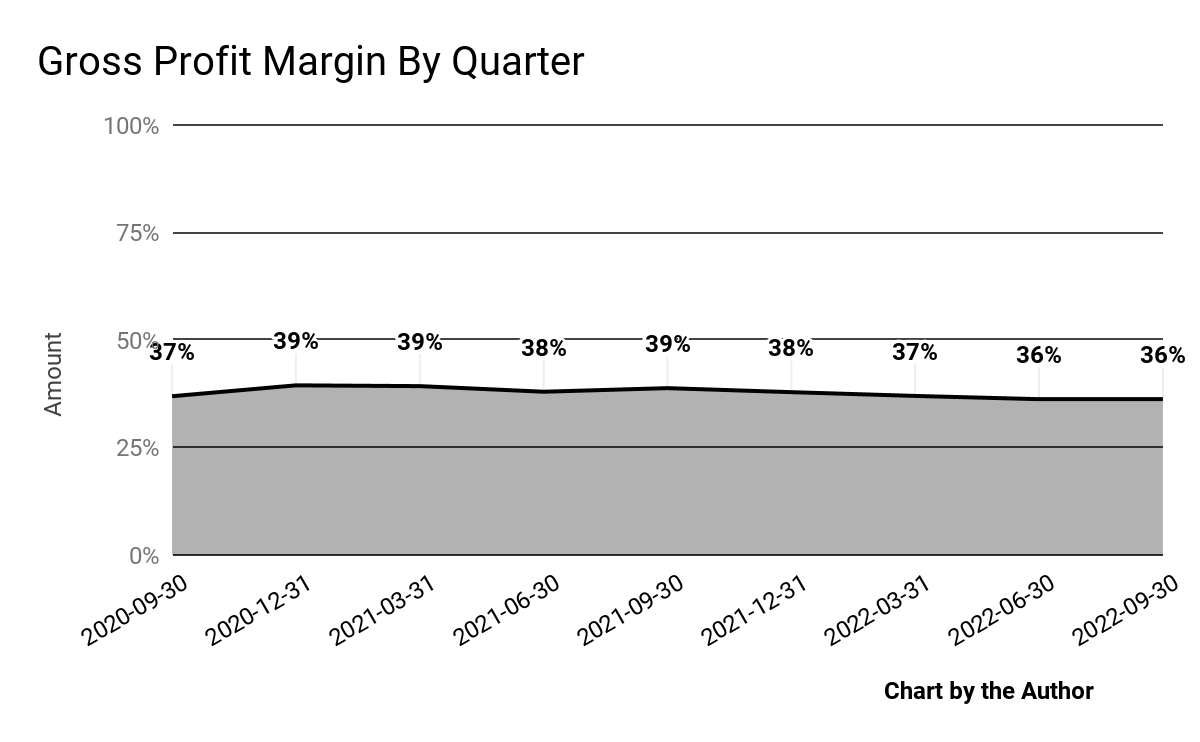

Gross profit margin by quarter has trended lower in recent quarters:

Gross Profit Margin (Financial Modeling Prep)

-

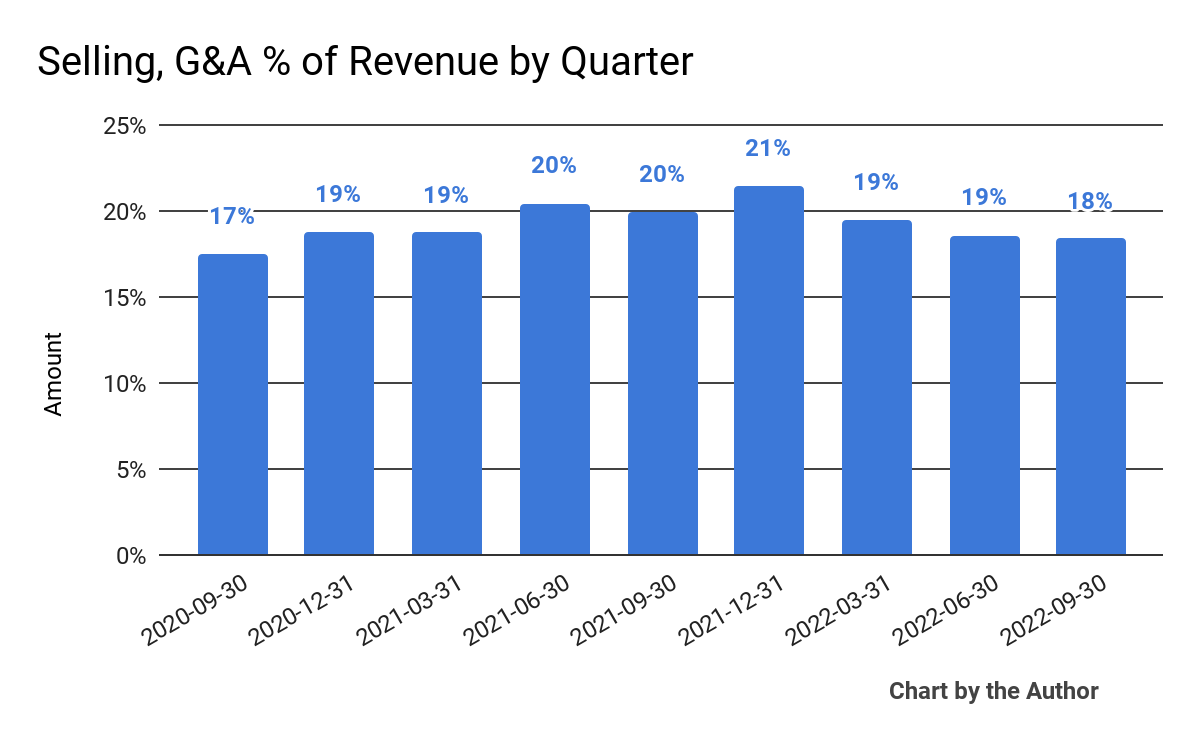

Selling, G&A expenses as a percentage of total revenue by quarter have dropped in recent quarters, indicating the company is becoming more efficient in generating each marginal dollar of revenue:

Selling, G&A % Of Revenue (Financial Modeling Prep)

-

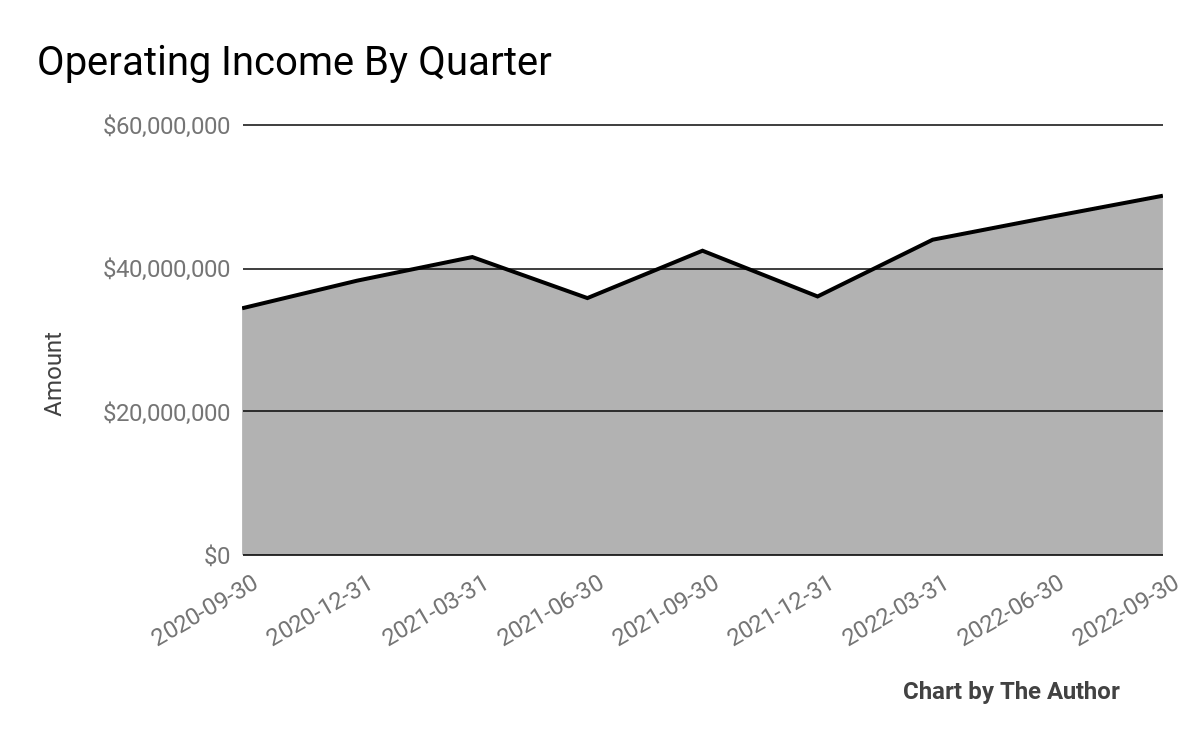

Operating income by quarter has trended higher recently:

Operating Income (Financial Modeling Prep)

-

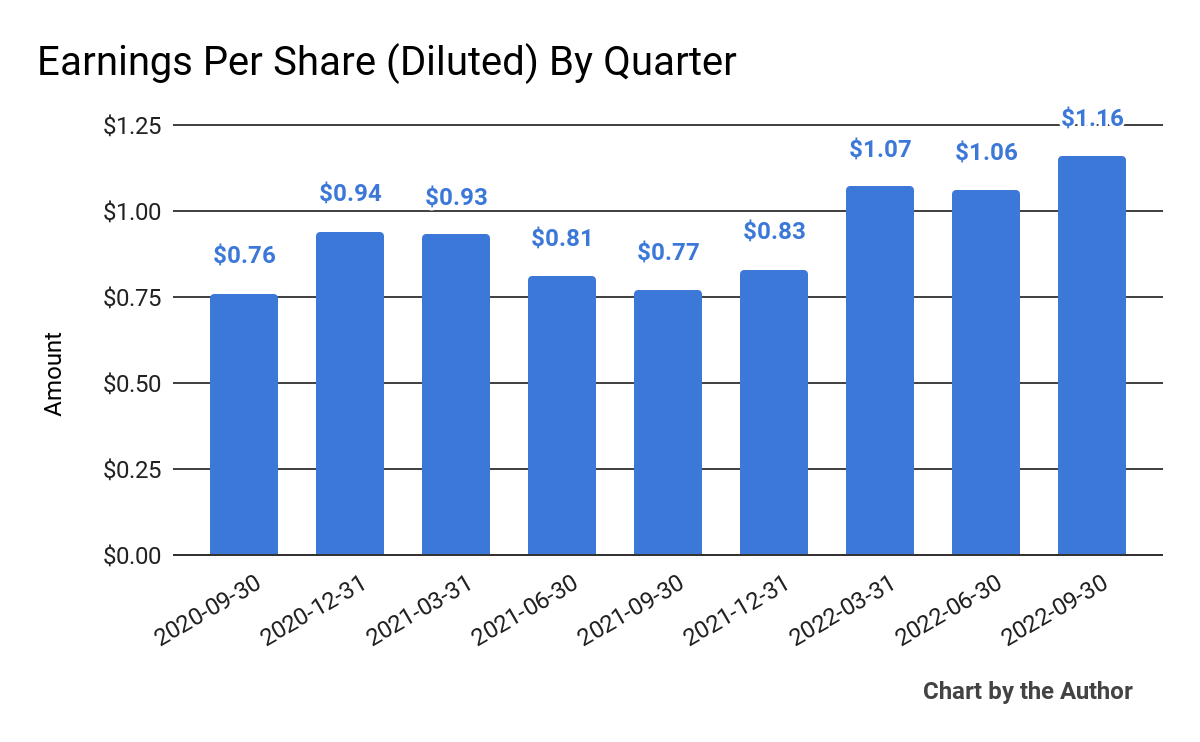

Earnings per share (Diluted) have also risen more recently, as the chart shows below:

Earnings Per Share (Financial Modeling Prep)

(All data in the above charts is GAAP)

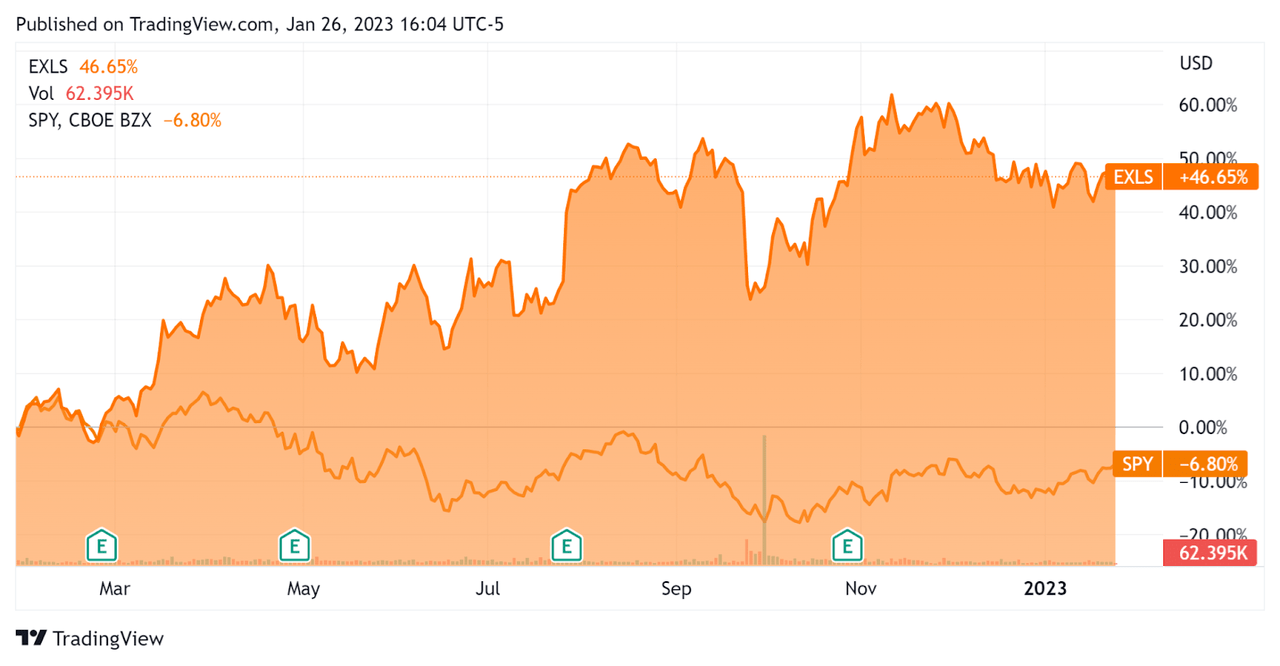

In the past 12 months, EXLS’s stock price has risen 46.7% vs. the U.S. S&P 500 index’s drop of around 6.8%, as the chart below indicates:

52-Week Stock Price Comparison (Seeking Alpha)

Valuation And Other Metrics For ExlService Holdings

Below is a table of relevant capitalization and valuation figures for the company:

|

Measure [TTM] |

Amount |

|

Enterprise Value / Sales |

4.5 |

|

Enterprise Value / EBITDA |

22.2 |

|

Revenue Growth Rate |

23.9% |

|

Net Income Margin |

10.5% |

|

GAAP EBITDA % |

20.1% |

|

Market Capitalization |

$5,656,361,472 |

|

Enterprise Value |

$5,938,088,091 |

|

Operating Cash Flow |

$171,714,000 |

|

Earnings Per Share (Fully Diluted) |

$4.12 |

(Source – Financial Modeling Prep)

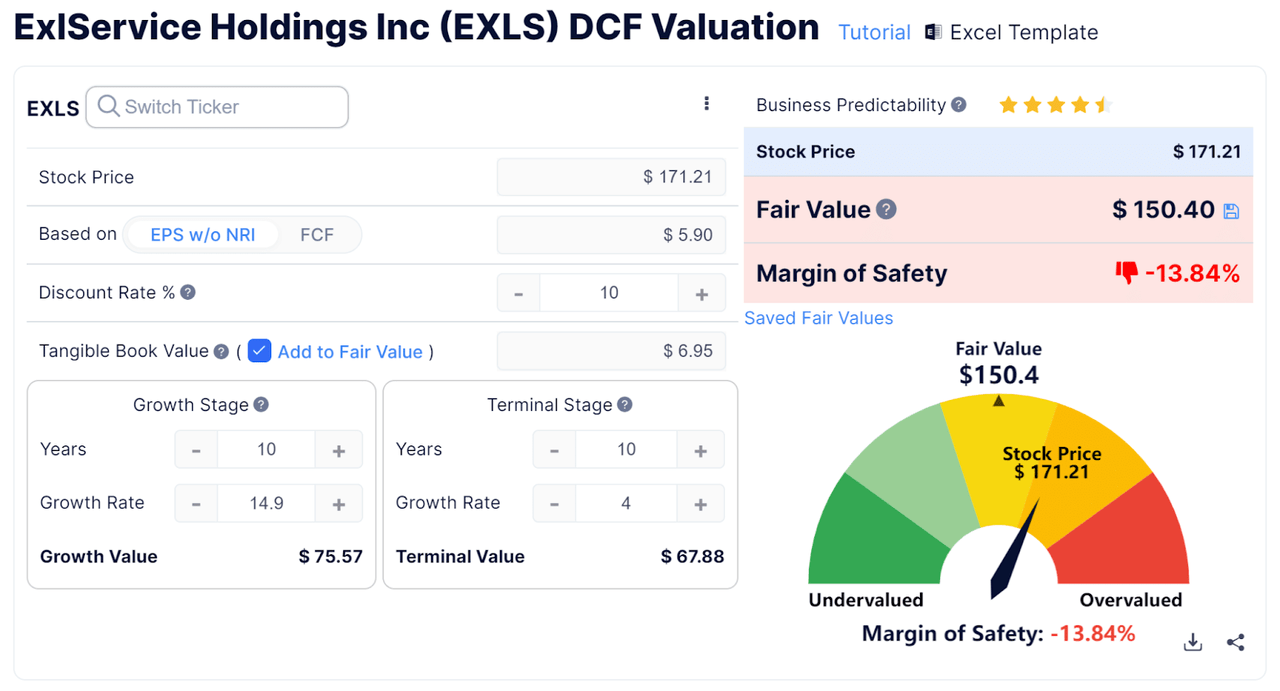

Below is an estimated DCF (Discounted Cash Flow) analysis of the firm’s projected growth and earnings:

Discounted Cash Flow Calculation (GuruFocus)

Assuming generous DCF parameters, the firm’s shares would be valued at approximately $150.40 versus the current price of $171.21, indicating they are potentially currently overvalued, with the given earnings, growth, and discount rate assumptions of the DCF.

Commentary On ExlService Holdings

In its last earnings call (Source – Seeking Alpha), covering Q3 2022’s results, management highlighted the heightened concern from clients that are leading them to reduce costs and streamline their operations, providing ample demand for the firm’s service offerings.

Through the end of Q3, the firm added 5,700 employees focused on the functions of data engineering, data science, cloud and AI.

As to its financial results, revenue rose 24.5% year-over-year, with the company’s Analytics segment driving most of the growth and representing 46% of total revenue.

SG&A expenses as a percentage of revenue dropped 1.5% year-over-year due to operating leverage, but adjusted operating margin fell by 90 basis points due to ramping up to service new clients and ‘higher operating expenses as we return to the office.’

For the balance sheet, the firm finished the quarter with $262.2 million in cash, equivalents and short-term investments and $270 million in total debt.

Over the trailing twelve months, free cash flow was $131.4 million, of which capital expenditures accounted for $40.3 million. The company paid a hefty $46.6 million in stock-based compensation.

Looking ahead, management raised its full-year 2022 revenue guidance to growth of 24.5% at the midpoint of the range on an as-reported basis and adjusted EPS to be $5.90 at the midpoint.

Note that adjusted EPS does not include stock-based compensation, which is a considerable amount for EXLS.

Regarding valuation, my discounted cash flow calculation assumes adjusted EPS for the full year period of 2022, and still the company’s stock appears to be fully- or over-valued at its present price level.

The primary risk to the company’s outlook would be a slowdown in customer engagements due to a macroeconomic slowdown, although there is significant disagreement as to whether or when that may occur.

EXLS has performed quite well during a difficult year for stocks but a question is how much the stock can continue to appreciate in value ahead.

Management says their guidance has been conservative, even with the increase, and that conservatism is due to the uncertain macroeconomic environment as they see some deals being delayed while others are being sped up.

The firm is exposed to several less cyclical industries, so even a downturn may affect its trajectory less than others.

Given that positioning and despite its apparent full DCF valuation, my outlook on EXLS is a Buy at around $170 per share.

Be the first to comment