Justin Sullivan

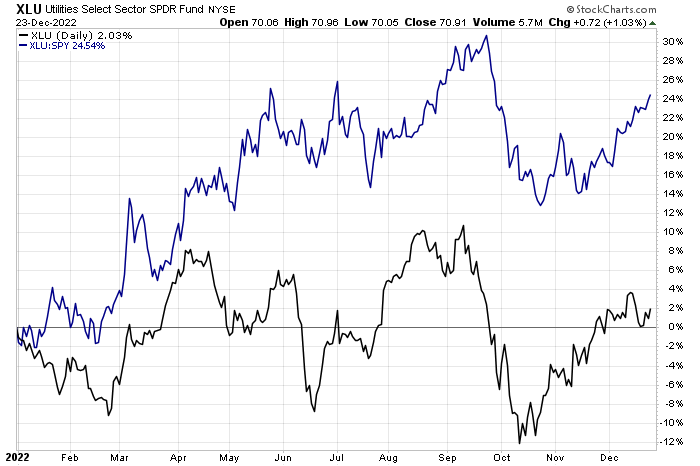

Utilities stocks have seen a wild ride this year. The Utilities Select Sector SPDR ETF (XLU) is fractionally positive (when including dividends) in 2022, outpacing the broad market by nearly 25 percentage points. Late September through much of October was a volatile period, but relative strength quickly returned for this defensive niche of the market.

One name has gone seemingly straight up over the past six months, but are more gains to come in shares of PG&E? Let’s turn on the lights on this trade.

Utilities Relative Rally Back On

Stockcharts.com

According to Bank of America Global Research, PG&E Corporation (NYSE:PCG) is the owner of the Pacific Gas & Electric Company, a regulated utility servicing 13 million people in a 70,000 square mile service area in Northern and Central California. The utility has businesses in electric and natural gas distribution, electricity generation, procurement, and transmission, as well as natural gas procurement, transportation, and storage. Pacific Gas & Electric manages 5.2 million customer accounts and 4.3 million gas customer accounts.

The California-based $31.9 billion market cap Electric Utilities industry company within the Utilities sector trades at a near-market GAAP price-to-earnings ratio of 19.1 and does not pay a dividend, according to The Wall Street Journal.

Back in October, the company reported an EPS beat but missed analysts’ revenue expectations. Shares rallied on big volume around the earnings release. PG&E continues to work away from its wildfire claims while focusing on reducing further environmental and regulatory risks. With EPS growth near 10%, higher than many of its industry peers, that risk seems more than accounted for.

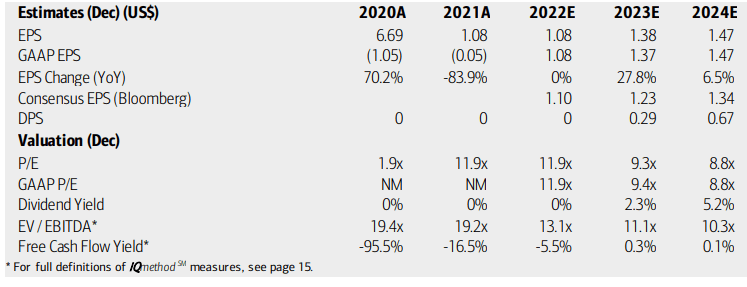

On valuation, analysts at BofA see earnings printing a goose egg (in terms of its annual growth rate) in 2022 but then recovering sharply in 2023 after a difficult, regulatory-risk-laden 2021. Per-share profit growth is then expected to moderate, though still be positive, in 2024. The Bloomberg consensus forecast is not quite as optimistic as BofA when looking ahead to 2023 and ‘24.

Dividends should be reinstated next year, which could be a bullish headline risk. Both the stock’s operating and GAAP earnings multiples venture into the single digits over the coming quarters, but the latest share price rise has left the stock a bit pricier than that now. Overall, I still like the valuation.

PG&E: Earnings, Valuation, Dividend Forecasts

BofA Global Research

Looking ahead, corporate event data provided by Wall Street Horizon show an unconfirmed Q4 2022 earnings date of Thursday, February 9 BMO. The calendar is light on volatility catalysts aside from that event though.

Corporate Event Calendar

Wall Street Horizon

The Technical Take

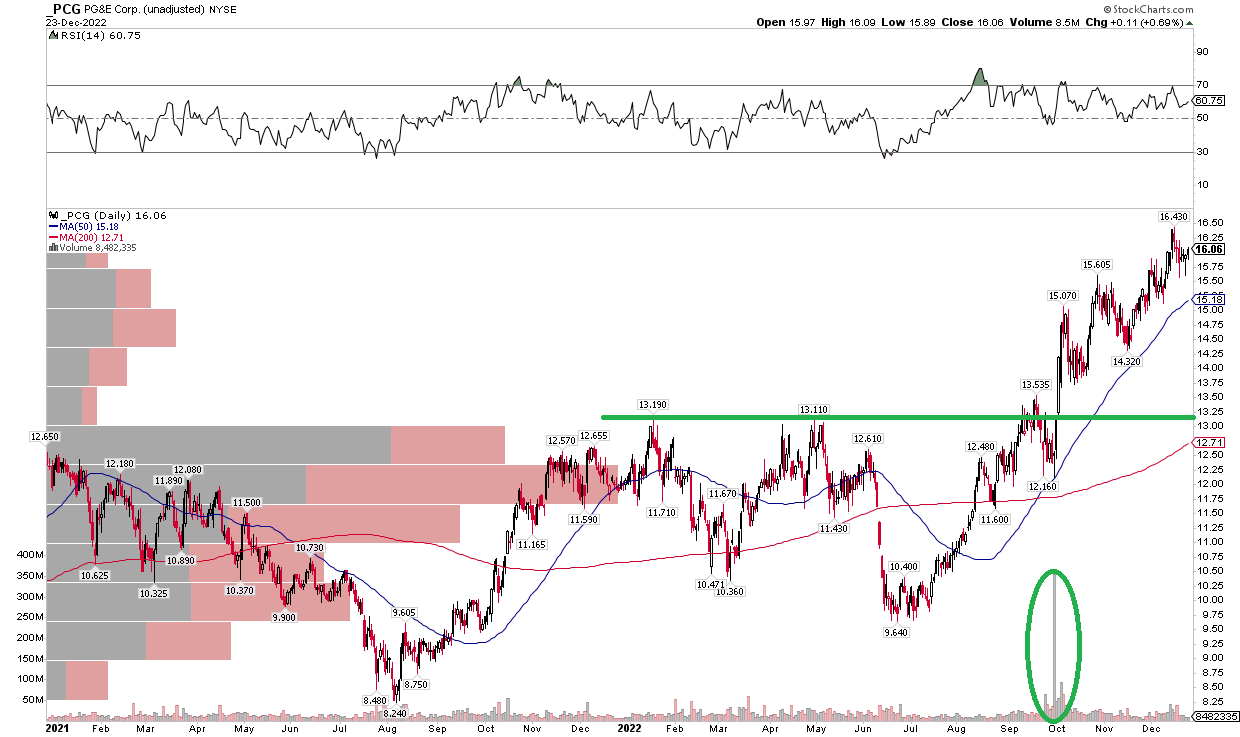

PCG has been among the best large caps in the market over the last several months. Shares are up more than 60% from their low under $10 back in June, notching a high just a few sessions ago near $16.50. The upside momentum comes as the Utilities sector has seen its bouts of volatility, but recent price action in favor of defensive areas has helped PCG. The stock had a bullish breakout above key resistance just above $13 in Q3, and it was off to the races after that.

The bears could make the case that a bullish price objective into the $16s has now been completed (based on the measured move from the $9.64 to $10.36 lows to the $13.11 to $13.19 highs). Until the uptrend breaks, the chart still looks solid. A break below the rising 50-day moving average could be bearish, but there should be good support in the low to mid $13s.

PCG: Strong Uptrend From the Summer, $13 Support

Stockcharts.com

The Bottom Line

I continue to like the valuation, and PCG’s technical chart shows big upside momentum. I maintain my buy rating.

Be the first to comment