U.S. Chamber Of Commerce Hosts CEO Summit Of The Americas In Los Angeles Anna Moneymaker

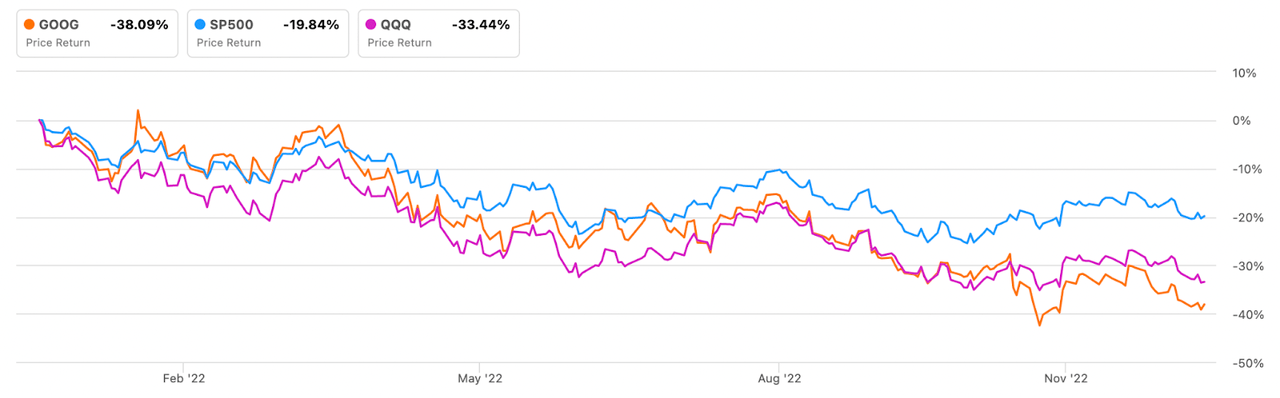

Alphabet Inc. (NASDAQ:GOOG) stock has been hit hard this year. Down 39% for the year, it has underperformed the NASDAQ-100 benchmark.

Google vs SPY vs the NASDAQ (Seeking Alpha Quant)

Google’s underperformance is a recent development. Earlier in the year, it actually avoided the worst of the tech stock crash, faring much better than the beaten down names that dragged down the index. If you look at the chart above, you’ll see that Google was ahead of the NASDAQ for much of the year, most recently on November 25. It flipped to underperformance in the last month.

So, what happened here?

Basically, it was two things:

-

Google’s first quarter earnings release showed a massive increase in headcount despite a slowdown in revenue growth. Overall results missed analyst estimates. Predictably, the stock tanked after the release came out.

-

ChatGPT launched recently and became a huge phenomenon on Twitter, with many people commenting that it could replace Google Search for some use cases.

After those two events transpired, Google stock dipped below the NASDAQ-100 on a full year basis.

The ChatGPT risk to Google has been covered extensively on Seeking Alpha. Some contributors think that total disruption is imminent, others believe that the risk is overblown. I myself wrote an article arguing that the risk was overblown, owing to the fact that ChatGPT does not overlap with all areas of Google’s business.

I still believe what I wrote in my recent article on ChatGPT. Google Search is 57% of Google’s business, and ChatGPT doesn’t have anything to do with search use cases like news, because its training data ends in 2021. There is little overlap between ChatGPT and other Alphabet businesses like YouTube, Google Cloud and Gmail.

However, there is a real risk to Google shareholders, not coming from ChatGPT, but from Google’s own management:

Hubris

Hubris, described as “excessive pride or self confidence,” is the cardinal Sin of the successful. It causes a person to think that their past success will continue into the future, and that nothing can stop them from getting what they want.

In late 2022, it’s hard not to believe that Google isn’t being affected by some degree of hubris. The company’s management persisted with expensive hiring drives long after it became obvious they were impeding performance, it fell behind OpenAI on consumer-facing AI apps, and it allowed its culture to become slow and bureaucratic (according to some insiders). None of these signs on their own “prove” that Google’s management considers itself untouchable, but collectively, they give pause.

Another factor suggesting Google leadership is getting too confident is the claim that Search results are getting worse. Many programmers now say that Reddit is better than Google for retrieving information, and others say the same thing about ChatGPT. It would be strange for Google to lose its status as the world’s best way to search for information, given that it has the resources to stay on top. Unfortunately, management seems unaware that there’s a problem: when people ask Google about why Search results are getting worse, they are often dismissed. For example, ex-Googler Marissa Mayer once said that it was the internet, not Google, that was getting worse.

There’s a strong case to be made here that the people in charge of Google feel their position is unassailable. That’s a real risk for shareholders to be aware of. ChatGPT in itself won’t kill Google, but enough ChatGPT-like disruptions could eventually eat away at Google’s moat. As of today, the moat is quite wide, but nothing is predestined to last forever. In this article I will explore the possibility that Google’s moat could diminish due to management complacency, ultimately concluding that it is a real long-term risk (though not a huge deal in the short term). I remain bullish on the stock overall, though, because it has a great collection of products and services that on the whole are very profitable.

Hubris in the History of Business

The idea that hubris leads to failure is one of the oldest tropes in literature. In Greek tragedy, the protagonist’s hubris would usually lead to self-destruction, or at least a major setback. The same pattern has been seen many times in business. In his essay “The Psychology of Human Misjudgment,” Charlie Munger describes a case when HP Inc. (NASDAQ:HPQ) decided to hire Carly Fiorina because CEO because management thought she seemed “articulate and dynamic.”

Because management was accustomed to success and believed in its own abilities, it felt confident in its positive opinion of Fiorina, and hired her, even though (according to Munger), a methodological recruiting process would have ruled her out as a candidate. Ultimately, HP under-performed the S&P 500 during Fiorina’s tenure, leading her to be forced out.

There are many other such examples of businesses facing difficulties due to hubris. A classic example is BlackBerry (BB) missing the transition to touch-screen smartphones after Apple (AAPL) launched the iPhone, because its sales were so good already. Ultimately, Apple’s vision triumphed and BlackBerry stock tanked.

Could Google have a “BlackBerry moment” on the horizon?

Right now, it does not look like any of Google’s products are going to be disrupted overnight. As I mentioned in my last article on ChatGPT, the most obvious competitive threat is only a partial threat. ChatGPT can’t compete with Google Search for news or product searches because its training data ends in 2021. Product searches are the most lucrative part of Google’s Search business, as they allow Google to show people ads relevant to products they’re searching for. So, the revenue impact of ChatGPT should be minimal in the near term.

However, if Google’s management is becoming complacent, then a series of ChatGPT-like threats could eat away at the company’s moat. Imagine, for a second, that ChatGPT added new data to ChatGPT’s training database, so that it could summarize breaking news stories and pull product reviews from Reddit. If that happened then ChatGPT would be competing with the totality of Google search. There are technical challenges to training AI on breaking news–the subject matter is changing all the time, making validation a challenge. But we could see this kind of thing emerge in the years ahead.

In the face of such possibilities, we have stories of excessive bureaucracy at Google, programmers saying that Reddit is better than Google for retrieving information, and Google executives dismissing claims that Search is deteriorating. It certainly looks like hubris is at play here; if it is, it could cause an erosion of value over time.

Why I’m Still Bullish

Having explored signs that Google’s management is getting overconfident, it’s time to explain why I’m still bullish on the stock. So far, my analysis makes it sound like Google is a minefield of risks, but overall, I think the stock is actually a good buy. In the next few paragraphs I’ll explain why I feel that way.

The first reason is valuation. Thanks to this year’s drawdown, Google is now cheaper than at any point in recent memory. At today’s prices, Google trades at:

-

17.8 times earnings.

-

Four times sales.

-

4.5 times book value.

-

12.4 times operating cash flow.

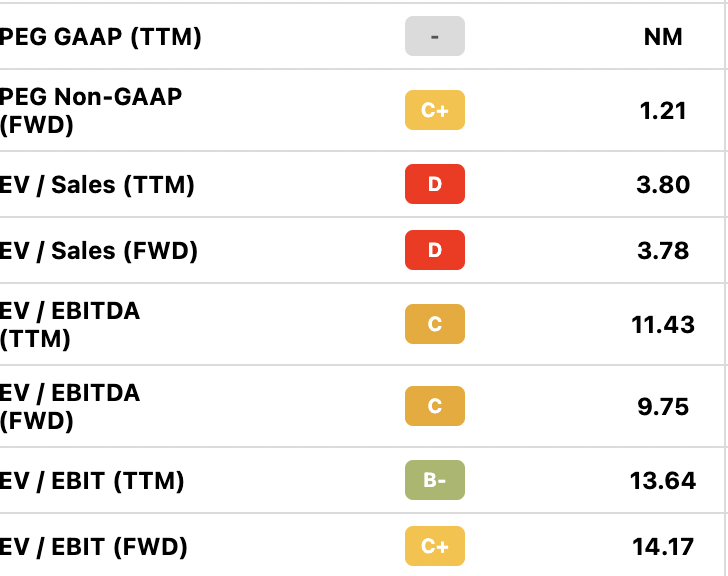

The first and last of these multiples are genuinely low, the middle two are still high, but lower than they were in the past. You can see some more valuation ratios below courtesy of Seeking Alpha Quant.

Google valuation (Seeking Alpha Quant)

Google also comes out pretty cheap in a discounted cash flow (“DCF”) model. I’ve done complete Google DCF models, with modeled financial statements and estimated growth, in past articles. You can check out one such model here. For now, I’ll just point out that in a terminal value model, GOOG has upside with no growth assumed. If you assume 0% growth and discount the company’s $4.76 in free cash flow per share at 5%, you get a $95 price target. The current treasury yield is 3.75%, so the chosen discount rate includes a risk premium. Normally equity risk premia tend to be higher than 1.25%, but since my growth assumption is incredibly conservative (0%), discounting at 5% is justified. If Google never grows again, it should be worth at least $95.

Apart from its valuation, another reason I’m bullish on Google is because it still has appreciable top line growth. Google’s earnings have been trending down in recent quarters, but it still has revenue strength. In the most recent quarter, Google’s revenue grew at 6%, when other big tech companies like Meta Platforms (META) and NVIDIA (NVDA) saw their growth turn negative. Of course, the earnings growth achieved on this revenue level was not strong. But rising revenue provides a path to future earnings growth assuming that management eventually sees the light on cost discipline. The hubris I mentioned earlier might delay the realization that such discipline is needed, but we have got hints that cost reduction could start as early as the first half of 2023. That would be great news were it to materialize.

Google’s recent headline earnings metrics (Alphabet Inc)

The Bottom Line

The bottom line on Google is that it’s a great company whose management needs to make some big decisions right now. Cost discipline is urgently needed in the near term, while long term investments in AI and Search result quality will have to be made. It won’t be easy, but a little stock market volatility can be just the wakeup call management needs to start taking action.

Be the first to comment