Wagner Meier

A little more than a year ago, slightly agitated by the way the market has approached the question of valuing the Brazilian oil and gas giant, we wrote an article pointing out what we considered a major oversight when it comes to assigning value to the true potential of Petrobras (NYSE:PBR) (NYSE:PBR.A). The article under the title: “The Best Oil Stock Remains Hidden In The South” can be accessed through this link. Interestingly enough, the company was trading at a relatively similar price of $10.28 per share at the time, with slightly similar discussions concerning the political risks surrounding the company. I find that there are a lot of similarities between today and late 2021. As the subtitle from the famous Tolkien novel would suggest, it seems we have gone “There and Back Again.” Now, as we are facing the other end of the pendulum swing in terms of energy price movements, just as significant political headwinds threaten to endanger shareholders’ interests, we believe it is worth revisiting the question of the Brazilian black goldmine.

What makes today different?

The company’s share price has truly been nothing short of a rollercoaster ride as of late, even as we compare it to a very turbulent year in the markets. The reasons behind this have been mostly political in nature. Brazil has gone through a very close presidential race between incumbent Jair Bolsonaro, a pro-business and capitalist politician, and Lula da Silva, a former president, and social democrat.

The share price first came under pressure as early polls indicated that the challenger had a fairly good chance of knocking the incumbent out of office. It was not uncommon to hear predictions of a resounding victory in the first round. At the time, the company was still handsomely rewarding shareholders via dividends.

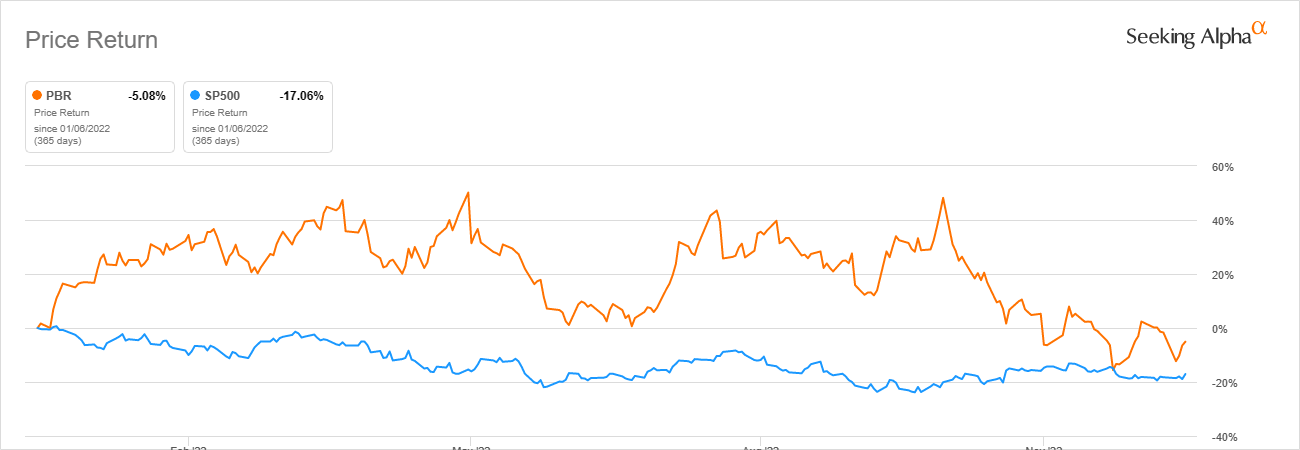

The first round of the elections led to a somewhat unexpectedly good performance by the business-friendly candidate, resulting in a slight uplift in the price. Shares of PBR traded as high as $16.05 in October. However, after being soundly defeated in the second round by the leftist-leaning Lula, a selloff ensued.

Petrobras vs S&P500 1-Year Return (Seeking Alpha)

Since then, but even during the election cycle, the new administration has sent out several messages that were quite clear: If you are a Petrobras shareholder, things are set to change for the worse from this point on. The company is now expected to undo years of investor-friendly management, that came with aggressive cost-cutting, and some hefty dividends.

Petrobras has to be profitable, it has to earn, it has to distribute dividends to the shareholders. But it cannot be the madness that it is today. What is happening is a total debacle, it is a crime against the Brazilian people.

Luiz Inácio Lula da Silva, Brazilian President

Like many other oil and gas companies across the globe, Petrobras benefited from the energy crisis triggered by Russia’s invasion of Ukraine, among other factors. This fact, combined with the rising fuel prices the Brazilian people had to endure, made great cannon fodder in political debates for the veteran politician.

Under the new regime, the focus is expected to shift significantly toward increasing investments in refining and renewable energy. In one of the first major decisions concerning Petrobras, Lula decided to name Jean-Paul Prates, a senator from his leftist-leaning Workers’ Party and a former Petrobras official, as the new head of the oil company.

The last “nail in the coffin” of the bull thesis was the decision to remove Petrobras from the government’s privatization list. Privatization was long debated as one of the major cornerstones of the bull thesis that could potentially fully unlock the value hidden behind the majority government-owned Petrobras.

In an attempt to ease investor concerns, the new company CEO has announced that the oil giant will continue to sell oil in line with global fuel prices for the foreseeable future. However, as seen from the recent price volatility, those willing to trust the new government remain a minority.

If we add dwindling energy prices on top of that, that is how we end up with a free cash flow dividend machine trading for a trailing dividend yield of nearly 70%. Essentially, the perfect storm and multiple bear thesis play themselves out at the same time. We don’t want to imply that we belong to the previously mentioned minority, but that we believe those difficulties are what brought Petrobras back to the value territory we prefer to operate in.

Accessible shareholder gains

While Petrobras’ share price has been on a rollercoaster ride lately, it would be cynical to conclude the shareholders have been taken for a ride, in fact, they’ve been handsomely rewarded for their willingness to look beyond the oil and gas industry in the United States over the previous twelve months. Perhaps even more importantly, they have been rewarded for their willingness to engage with the inherent political risks associated with the investment.

Dividend History (Petrobras Investor Relations)

This is especially true for those shareholders who have been investing in the post-2020 recovery when shares could still be bought even for mid-single digits. Many of those investors have had their entire principal paid back via dividends in a little less than two years.

These are nothing short of amazing returns when we examine broader market movements. Just to note, the S&P 500 (SPY) has yielded approximately 9.37% over the previous two years, including dividend reinvestment. Much less otherwise. The Brazilian oil and gas giant has created significant shareholder value through its dividend program in the past couple of years.

The combination of lower energy prices, which should reflect on the company’s bottom line, and the changing strategic paradigm on top will almost certainly result in significantly lower dividend distributions in the short-to-mid term future. Still, a complete dividend cut is currently out of the question, and even the most negative estimates still place the dividend yield in the high single digits, at least with the current share price in mind.

Petrobras Stock Valuation

We’ve already said that, in our opinion, the business is still undervalued. That is, in other words, the company’s potential to outperform is still there, just remains hidden behind rising political challenges.

Because of the political concerns that come with investing in Brazil and the “crackdown” conducted by the Lula administration, Petrobras continued to trade at a noticeable discount to its industry peers, whether we are discussing US-based counterparts such as Exxon Mobil (XOM) and Chevron (CVX) or international companies like BP (BP), Equinor (EQNR), PetroChina (OTCPK:PCCYF), TotalEnergies (TTE), and others.

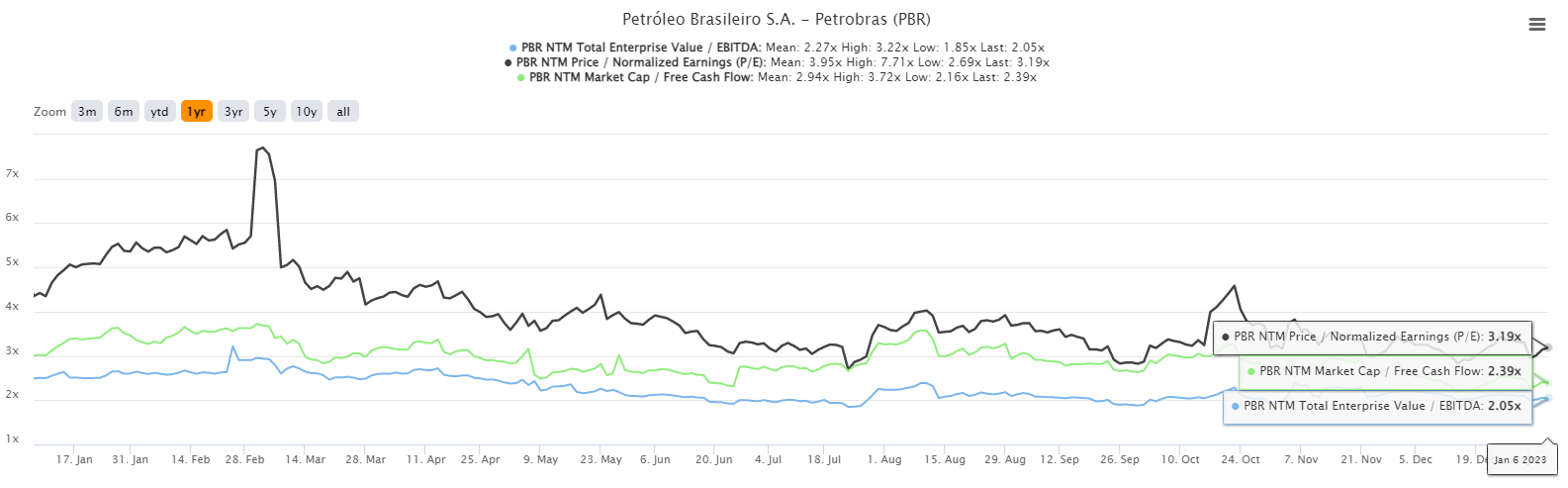

Petrobras Valuation (TIKR Terminal – IQ Capital Data)

This has led to an enticing valuation, with Petrobras’ current price implying that it is being sold for an NTM EV/EBITDA of 2.05x, an NTM P/E of 3.19x, and an NTM P/FCF of 2.39x. The pure value proposition here is something that is difficult to argue with. However, many analysts have not yet factored or priced in a significant change in strategy, such as higher CapEx and its potential impact on cash flow and subsequent dividends. With shifting strategies and likely degrading operational results moving forward, this probably won’t last for very long. Nonetheless, it says a lot about how highly the market values the current political risk, which we believe is a little too high.

Closing Arguments

Both internal and external factors weigh heavily on the current share price of Petrobras. Multiple bear theses are playing themselves out at the same time in what seems to be the perfect storm, much to the detriment of the average investor. On one end, with energy prices hitting new lows almost weekly, executives are left with little room to maneuver as the bottom line is likely to get thinner. This serves to highlight the internal factors even more because President Lula’s new left-leaning political leadership is likely to steer the corporation away from the interests of the average individual shareholder, in an attempt to appease the broader public amid ever-worsening macroeconomic conditions.

As a result, the subsequent market selloff has once again priced the firm far below what we consider reasonable levels. Those who were willing to engage with the company while previous political concerns were active have been handsomely rewarded in recent years, though such returns are not completely off the table. We maintain that the business is still incredibly attractive on a fundamental level, and we reiterate our conviction that the market has misjudged the political risks associated with the Petrobras investment to a certain degree.

Be the first to comment