cemagraphics

ETFs are a great way to gain automatic diversification, and for many investors, this comes with a peace of mind in not having to trade the market day in and day out and second guess one’s own decision-making abilities.

For investors who wish to own an all-in-one basket of stocks, low cost ETFs are a good option, and Vanguard is a posterchild for charging low fees, considering that its owners are the very investors in its funds.

This brings me to the Vanguard High Dividend Yield ETF (NYSEARCA:VYM). While this ETF holds a number of quality names, I highlight why caution is warranted at this time with regards to buying into this ETF, and give a level at which I’d be interested, so let’s get started.

VYM: Wait For A Drop

The Vanguard High Dividend ETF seeks to track the performance of the FTSE High Dividend Yield ETF. As one would expect from a dividend focused ETF, VYM has lower exposure to technology stocks, which generally do not pay or pay low dividends, compared to the S&P 500 (SPY).

Similar to Vanguard’s family of ETFs and mutual funds, VYM charges a low expense ratio of just 0.06%, sitting well below the 0.40% median across the ETF universe. This has earned VYM an A+ Expense Grade. This expense is more than covered by VYM’s 2.94% dividend yield and should not be of concern to investors.

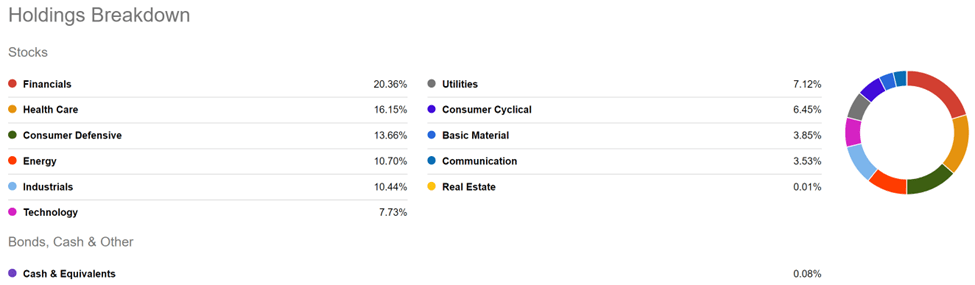

Financials, Healthcare, and Consumer Defensive make up VYM’s top 3 sectors comprising half of the portfolio total. As shown below, VYM has exposure to other dividend paying segments including energy and Industrials, which combine to add another 21% of the portfolio total.

VYM Sectors (Seeking Alpha)

While VYM’s total return has modestly underperformed that of the S&P 500 over the past decade (197% versus 221%), its focus on dividends has proven effective at giving investors significant downside protection over the past year. As shown below, VYM’s total return has been flat over the trailing 12 months, comparing favorably to the negative 16% total return of the S&P 500.

VYM Total Return (Seeking Alpha)

While I do like VYM’s broad diversification, I don’t think it lives up to the “High Dividend Yield” in its name, with a dividend yield of just 2.9%. Moreover, VYM also doesn’t have a particularly high dividend growth rate, with 3 and 5-year dividend CAGRs of 4.6% and 6.3%, respectively. For VYM to be appealing, I would expect for the dividend yield plus 5-year dividend CAGR to be at least 10%.

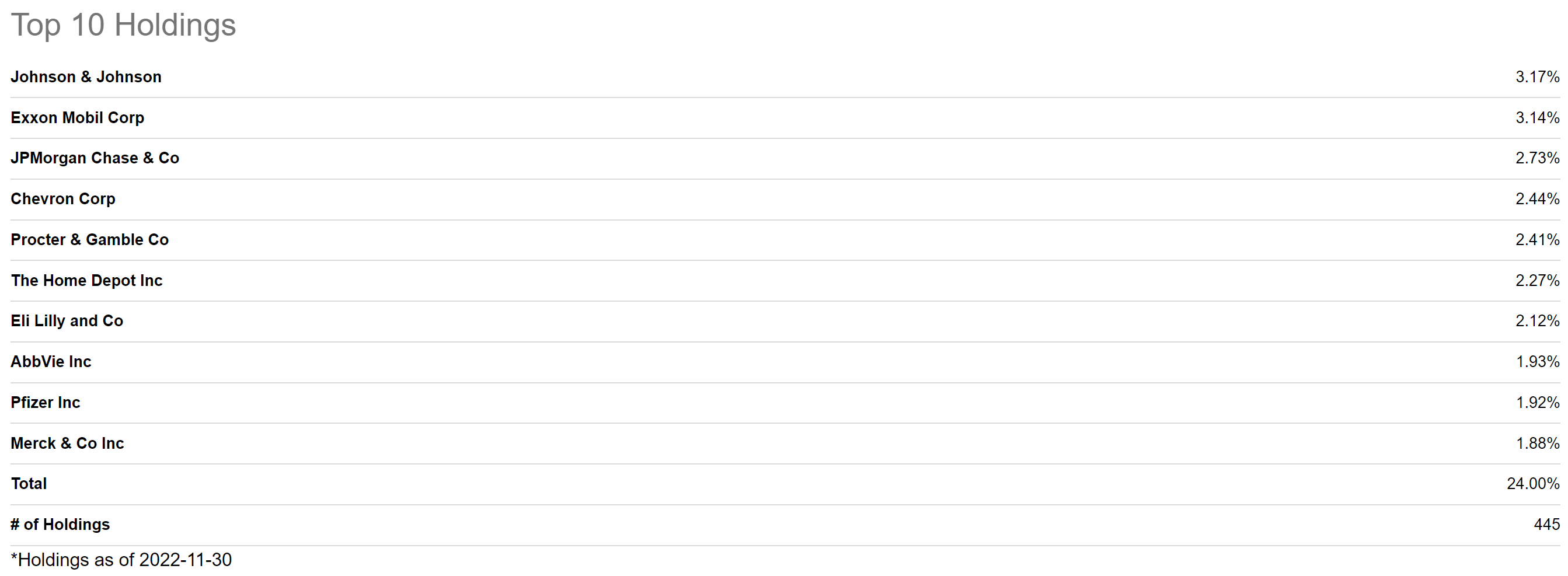

VYM’s top 10 holdings include dividend stalwarts like Johnson & Johnson (JNJ), Exxon Mobil (XOM), and Chevron (CVX). It’s no surprise that the 2 oil giants make up VYM’s top 4 list of holdings, given the run up in energy prices. However, that market has fully priced in all of the good news while ignore the potential downside risk. In fact, Bank of America (BAC) recently downgraded CVX, calling it a “victim of its own success”, and noting the following:

While the transparency of free cash flow has supported buybacks and related dividend growth, the absence of material long-term growth in cash flow means absolute value is capped beyond a more aggressive call on oil above our $80 base case or another reset in project visibility possibly through additional acquisitions from what is now a pristine balance sheet.

As shown below, VYM’s other top 10 holdings include expensive and potentially overvalued names such as Procter & Gamble (PG) which carries a forward PE of 26, Home Depot (HD) with a forward PE of 19, and Johnson & Johnson, which is trading near its 52-week high with a forward PE of 18.

VYM Top 10 Holdings (Seeking Alpha)

Considering the above, I simply don’t see enough value in VYM at the moment, and at a yield of just 2.9%, it doesn’t live up to its name, especially considering the many high yielding options on the market today. As such, I would find VYM to be more appealing after a 10 to 15% drop in price, which would push the yield closer to the 3.5% range.

Investor Takeaway

The Vanguard High Dividend Yield ETF is a low cost option for investors looking to get exposure to dividend paying stocks. However, given its current yield of 2.9% and the expensive valuations of many of its top holdings, I would caution against buying VYM at today’s levels and instead wait for a 10-15% pullback before considering it. I wouldn’t be surprised to see this happen with the potential for a market pullback and the relative overvaluation of some of its top holdings.

Be the first to comment