Kevin Dietsch/Getty Images News

Intro

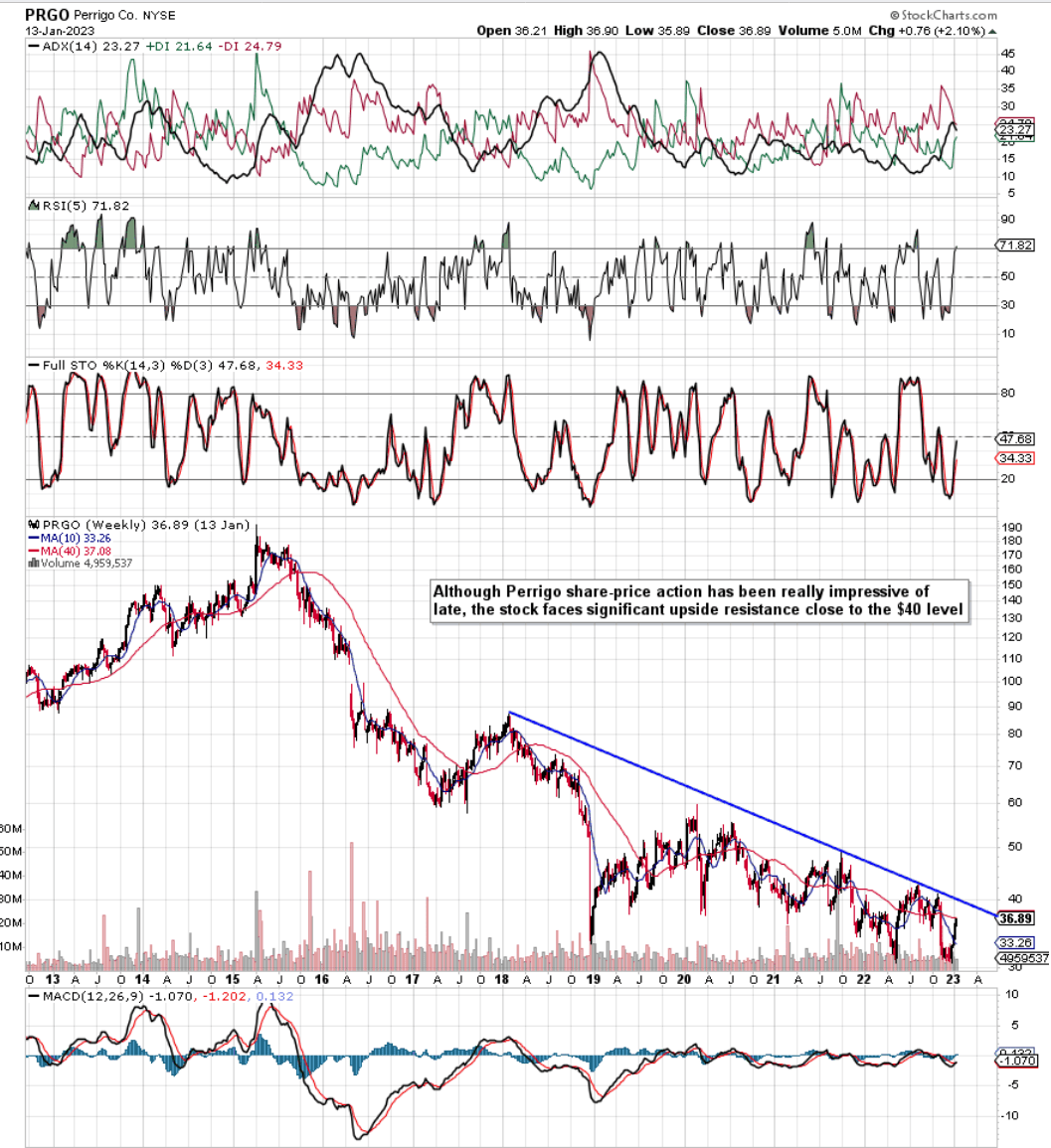

We wrote about Perrigo Company plc (NYSE:PRGO) in April last year when we were hopeful that the healthcare company could finally break out of its multi-year consolidation zone. Fast forward 9 months later and the stock is trading at practically the same level as last April. Suffice it to say, no breakout has occurred. In fact, shares stooped down to test their May 2022 lows last month (December) before delivering a violent rally up to the stock’s 200-day moving average of approximately $37 a share. The question now is whether Perrigo has sufficient momentum to punch above this resistance level and finally break out of long-term consolidation.

The intermediate chart below which dates back to the company’s 2015 highs demonstrates that the company has it all to do. We state this because of the sustained pattern of lower highs in Perrigo although that recent December successful test definitely leaves room for encouragement. The problem however for Perrigo is the wall of resistance that the stock has above it. Suffice it to say, we would need to see something exceptional in the company’s present fundamentals and sustained weakness in the US Dollar (Which is what we have been seeing) for the $40 level to be taken out here in this present rally.

Perrigo Technical Chart (Stockcharts.com)

Latest Earnings Report

Perrigo’s latest third quarter earnings numbers clearly demonstrated that meaningful changes are happening on the income statement. Gross profit rose more than $26 million which helped operating profit to more than double to $52.8 million in the third quarter. Contributors to the company’s growth were CSCI & CSEA and fresh sales from the recent HRA deal. In fact, management increased the estimated synergies to come off the HRA deal which demonstrated how well this acquisition has performed to date.

Bullish external trends across a host of the company’s categories which led to multiple market share gains were encouraging in the third quarter. Women’s health, skincare-related sales, upper respiratory, allergy, oral care, and Perrigo’s nutrition business all saw strong gains in the quarter. It will be interesting to see how baby formula sales turn out this year for Perrigo, considering the shortage last year and how the company had to ramp up production to meet demand.

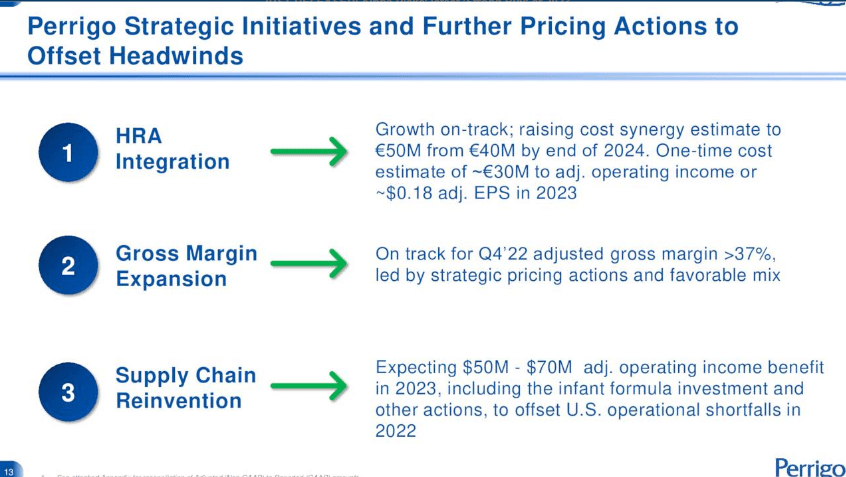

As we see on the slide below, management believes the HRA acquisition, rising gross margin, and supply-chain reinvention program will all positively affect operating profit in fiscal 2023. The CEO did go into the one-off charge of returning inventory from HRA’s former distributors, which now will be managed by Perrigo’s internal sales force. However, if external trends continue across the board and they have been, the initiatives below should turn out to be meaningful tailwinds for operating income.

Perrigo Strategic Initiatives (Company Presentation)

High Leverage

However, we also must look at the other side where the question is how would Perrigo’s financials deal with an environment with more sudden meaningful headwinds. While it is extremely difficult to predict forward-looking external conditions, the ability of a company to keep on investing in its business in a potential downmarket always is a major plus. Over the past four quarters, for example, $133.7 million of interest expense had to be paid from an operating profit kitty of $184.4 million. This gives us a trailing interest coverage ratio of 1.38, which is low no matter which way you size it up.

This is the worrying aspect from the bulls’ standpoint. With a $30 million approx charge to hit the income statement due to the above-mentioned HRA issue next year along with that higher interest expense, net income growth will remain under pressure if those above-mentioned strategic initiatives do not execute as planned. This goes back to the old premise: Sustained growth happens when there are sufficient earnings and cash flow to enable sustained investment which drives the sales and earnings cycle once more. Suffice it to say, we will be watching Perrigo’s upcoming Q4 numbers and any changes to forward-looking guidance closely.

Conclusion

Therefore, to sum up, Perrigo has had an excellent 4 weeks or so, which has resulted in shares rallying aggressively back up to the stock’s 200-day moving average. The significant resistance on the technical chat and the fact that Perrigo’s debt load now tops $4 billion ($4.96 billion market cap) means the gross margin needs to remain elevated to keep the wolf from the door. We look forward to continued coverage.

Be the first to comment