Mikhail Mishunin

***All figures in CAD unless otherwise noted.

Introduction

The market is ripe with discounted preferred shares that have the potential to deliver enormous returns over the next couple of years. Recent articles I have written on Seeking Alpha include AltaGas Series B And H Preferred Shares: Found Money, RPT Realty: A Low Risk Preferred Share Offering With A 7% Yield, and Imperial Petroleum: A Juicy 11% Yield On Preferred Shares. I have decided to discuss another great opportunity in the Pembina Pipeline Corporation (TSX:PPL:CA).

The Company

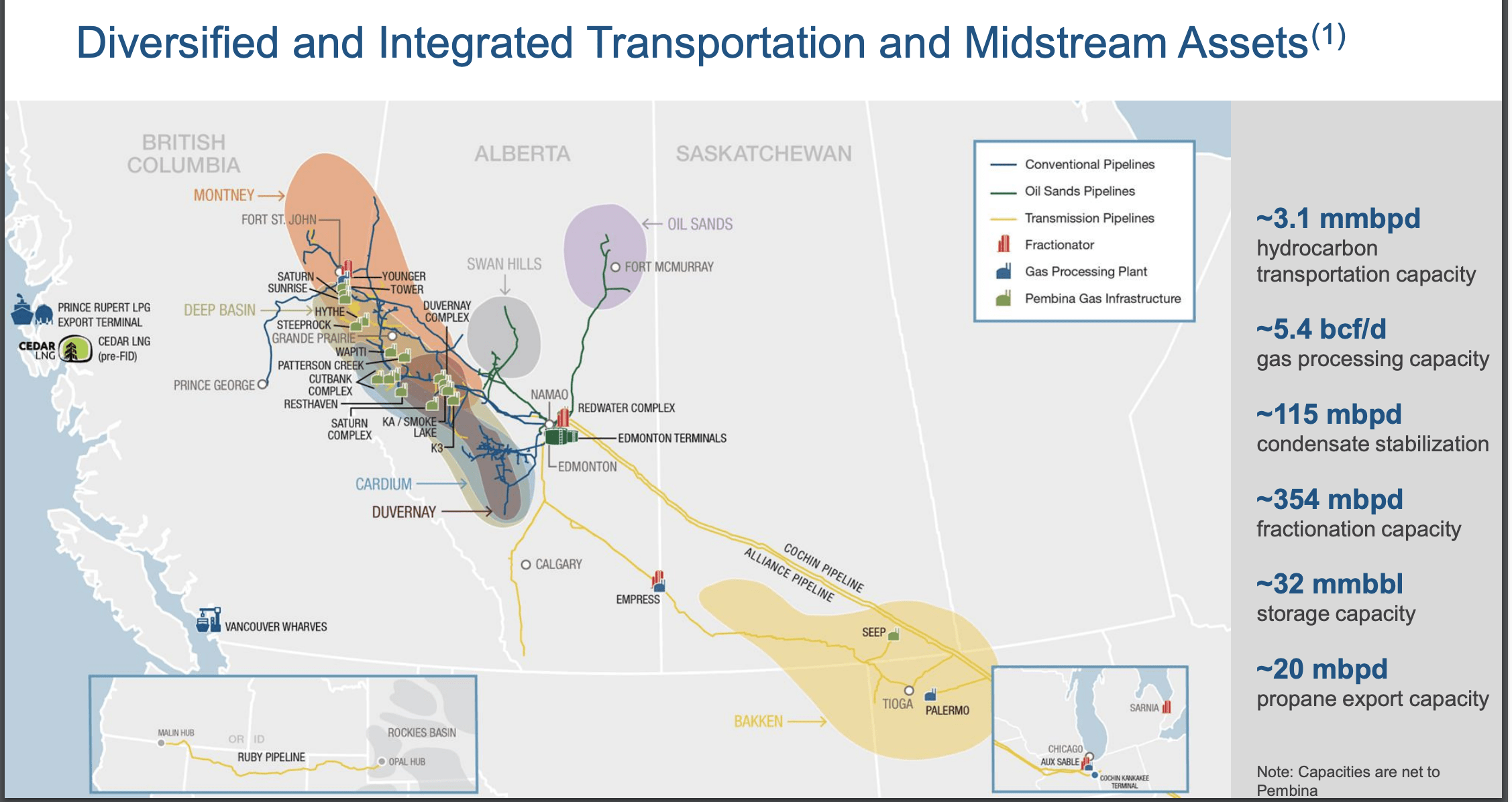

PPL owns and operates oil and natural gas pipelines, processing facilities, and logistics services including an export terminals business. PPL’s assets are primarily located in Western Canada. The business is divided into three segments, which include pipelines, facilities, and marketing and new ventures. The pipelines segment accounts for 55-60% of cashflows. The pipeline division operates 18,000 kilometers of pipelines for the transport of crude oil, natural gas, and natural gas liquids.

Investor Presentation December 2022 (Pembina Pipeline Corporation)

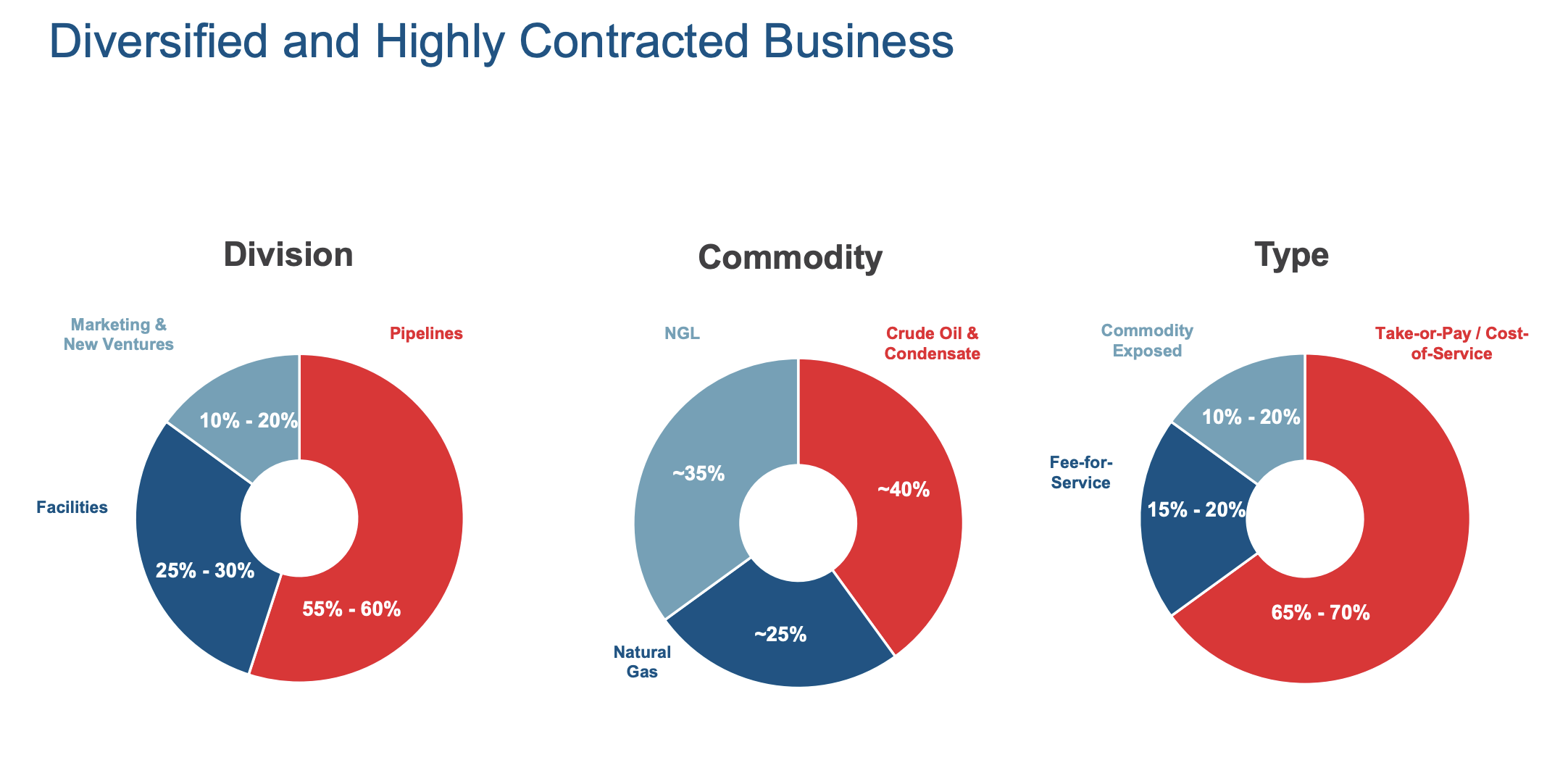

The business is divided into three segments, which include pipelines, facilities, and marketing and new ventures although pipelines account for 55-60% of cashflows. Pembina Pipeline enters into long-term contracts that are usually 5-10 years where the company stores and transports resources for customers. PPL is compensated based on the volume of resources handled, not on their value. In fact, between 80% and 90% of Pembina Pipeline’s cash flow comes from take or pay/fee for service contracts. This is the reason why the company’s cash flows are not nearly as volatile as commodity prices. Although production may fall when commodity prices fall, PPL maintains cash flows by requiring minimum volume commitments in its contracts. 80-85% of counter-parties are investment-grade which include a 20-year midstream services agreement with ConocoPhillips Canada (COP) for the transportation and fractionation of liquids and other long-term services agreement with Tourmaline Oil Corp. (TOU:CA) for the transportation and fractionation of liquids from their multiphase NEBC Montney development.

Investor Presentation December 2022 (Pembina Pipeline Corporation)

Q3 2022 Report

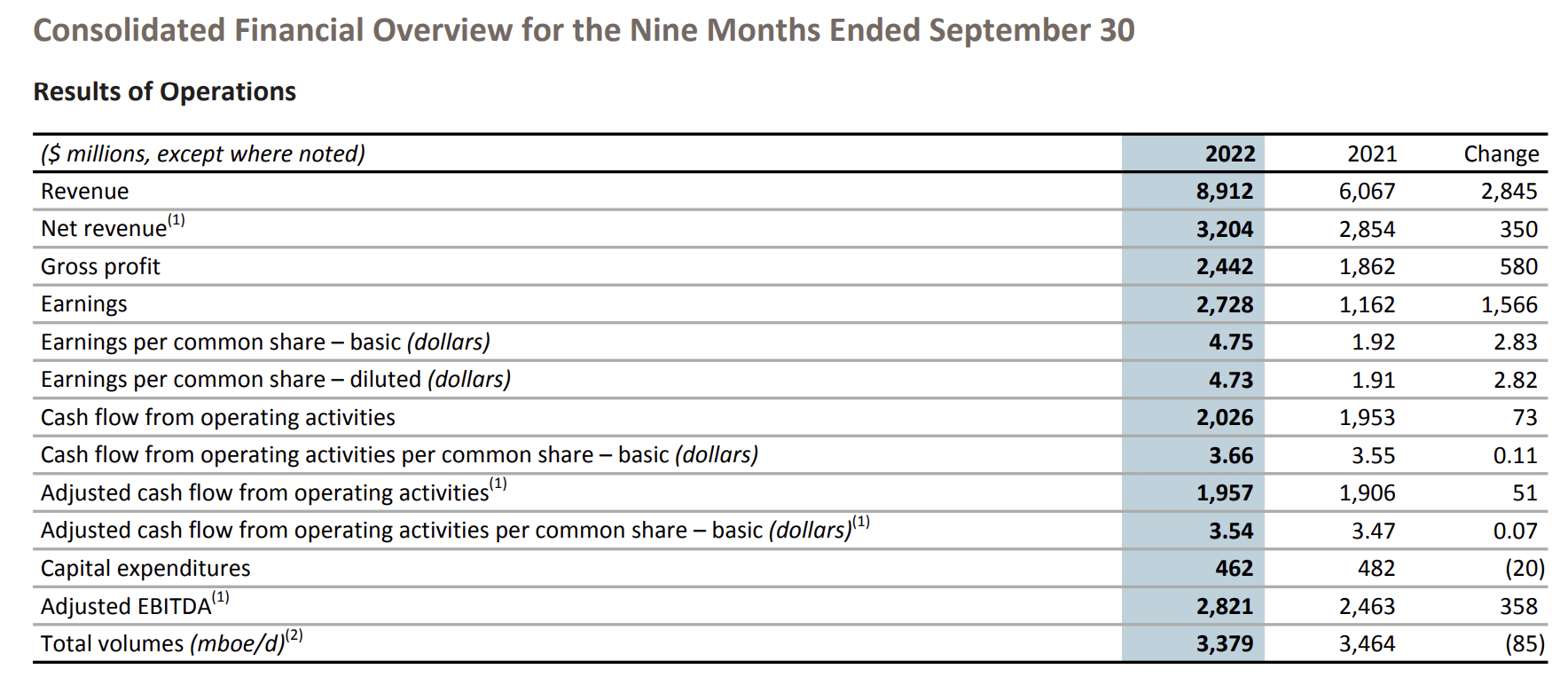

Strengthening oil and natural gas prices have led to higher production, therefore it should be no surprise that revenue and profitability is up across the board for PPL in their Q3-2022 results. EBITDA increased 15% YoY despite a $74 Million increase in power and fuel costs, and a $39 Million increase in salary and wage expenses.

Pembina Pipeline Corporation (Q3-2022 Report)

- $2.8 Billion increase in revenues, was largely due to an increase in crude oil, NGL and natural gas market prices, higher volumes on the Peace Pipeline system and higher tolls largely due to inflation, combined with higher volumes on the Cochin Pipeline and higher recoverable costs, partially offset by lower contracted volumes on the Nipisi and Mitsue Pipeline systems and lower revenue from the Field-based Gas Processing Assets contributed to PGI and now reflected in share of profit from equity accounted investees.

- $358 Million increase in EBITDA, primarily due to higher margins on crude oil, NGL, and natural gas sales, higher contributions due to the strong performance of the PGI assets, higher contributions from Aux Sable and Alliance, higher volumes on the Peace Pipeline system and on the Cochin Pipeline, higher tolls due to inflation, lower losses on commodity-related derivatives, and higher recoverable costs from the Horizon Pipeline system.

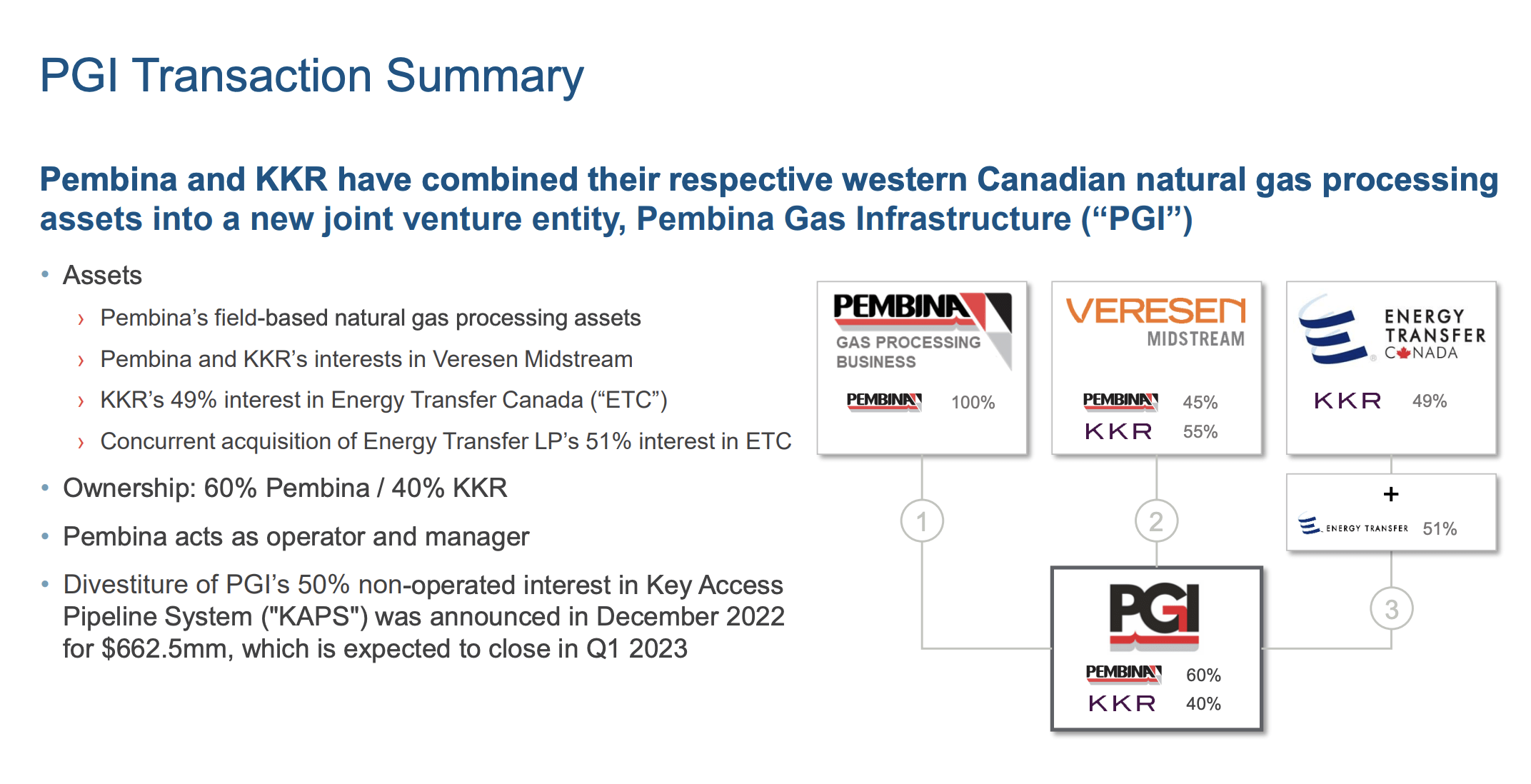

In August of 2022, Pembina completed its previously announced joint venture transaction with KKR & Co., Inc. to combine their respective western Canadian natural gas processing assets into a single, new joint venture entity called Pembina Gas Infrastructure Inc. (PGI). The gas processing entity will have a combined capacity of approximately 5 billion cubic feet per day (approximately 3 billion cubic feet per day net to PPL) and serving customers from central Alberta to northeast British Columbia.

Pembina owns 60 percent of PGI while KKR’s global infrastructure funds own the remaining 40 percent. Pembina will serve as the operator and manager of PGI. Pembina contributed to PGI its wholly-owned field-based gas processing assets, which include the Cutbank Complex, the Saturn Complex, the Resthaven Facility, the Duvernay Complex and the Saskatchewan Ethane Extraction Plant, as well as its 45 percent interest in Veresen Midstream. KKR contributed to PGI its 55 percent interest in Veresen Midstream, as well as its 49 percent interest in PGI Processing ULC.

Investor Presentation December 2022 (Pembina Pipeline Corporation)

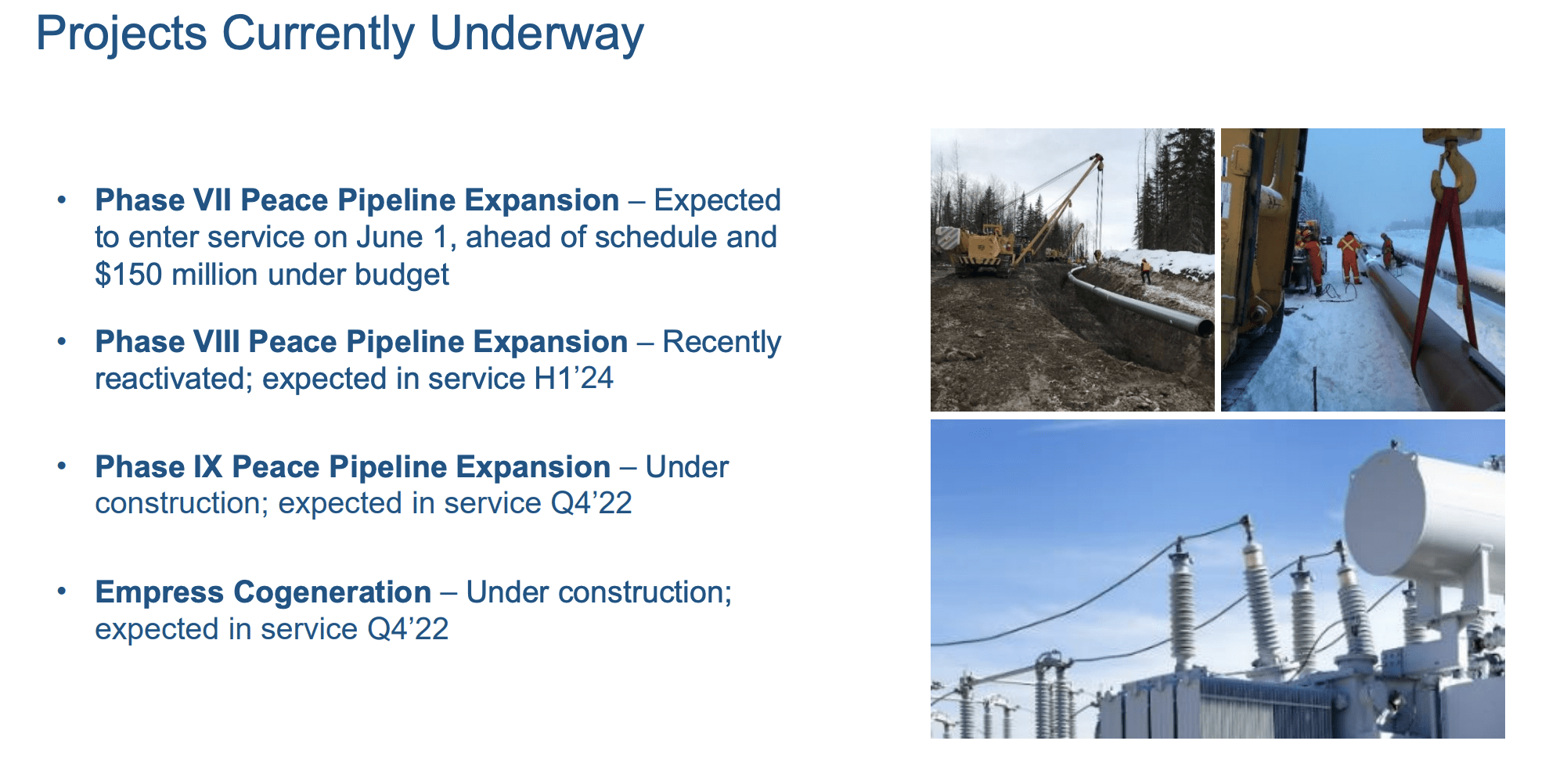

During Q3 2022, construction of the Empress Cogeneration Facility was completed, and brought into service in November 2022. The facility will use natural gas to generate up to 45 megawatts of electrical power, thereby reducing overall operating costs by providing electricity and heat to the existing Empress NGL Extraction Facility. Power will be consumed on site, thereby supplying up to 90 percent of the site’s electrical requirements. Phase IX Peace Pipeline Expansion project was also brought into service. This expansion includes new 6-inch and 16-inch pipelines debottlenecking the corridor north of Gordondale, Alberta. The expansion will see existing pipelines, which are currently batching, converted to single product lines.

Investor Presentation December 2022 (Pembina Pipeline Corporation)

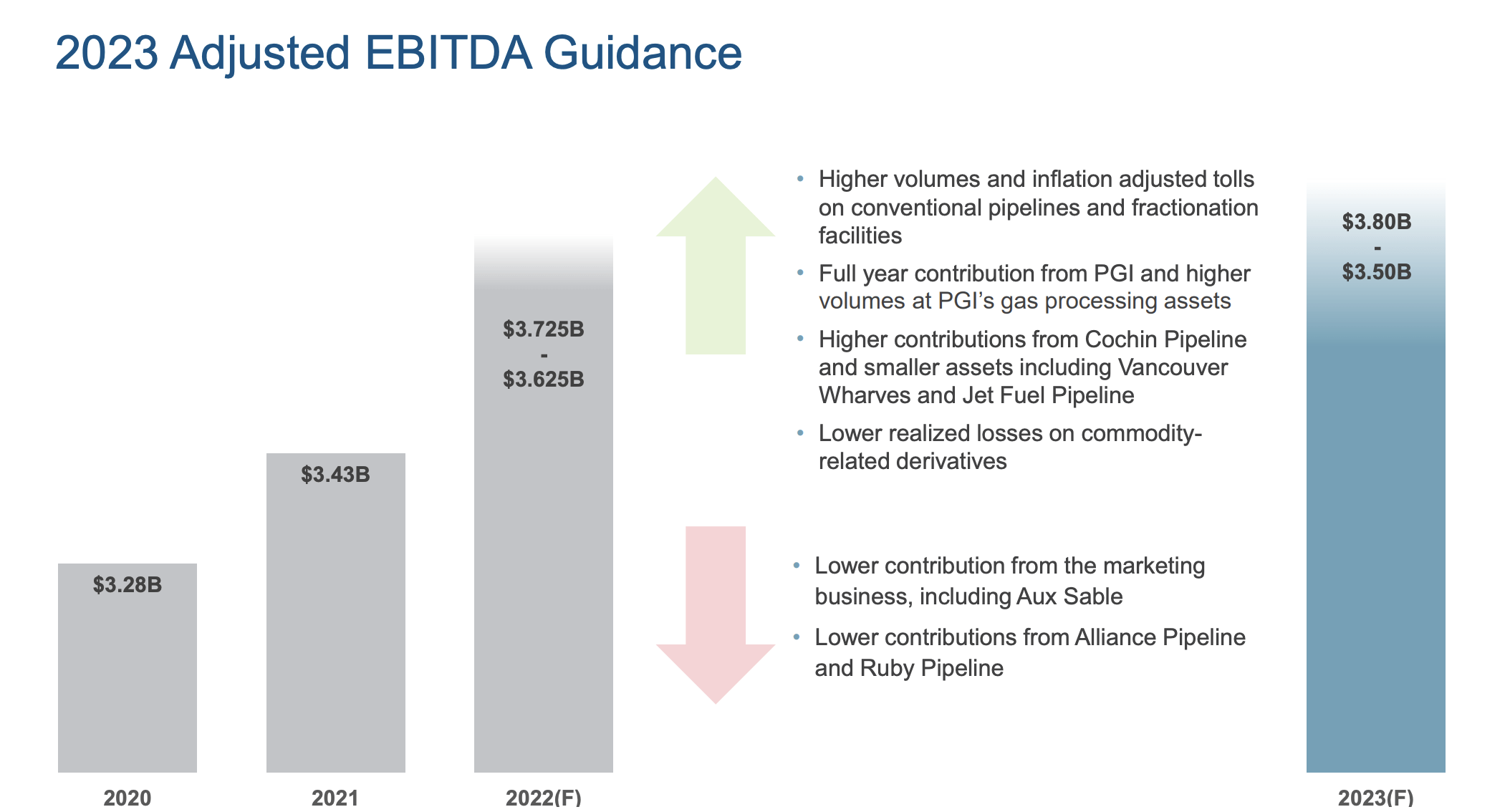

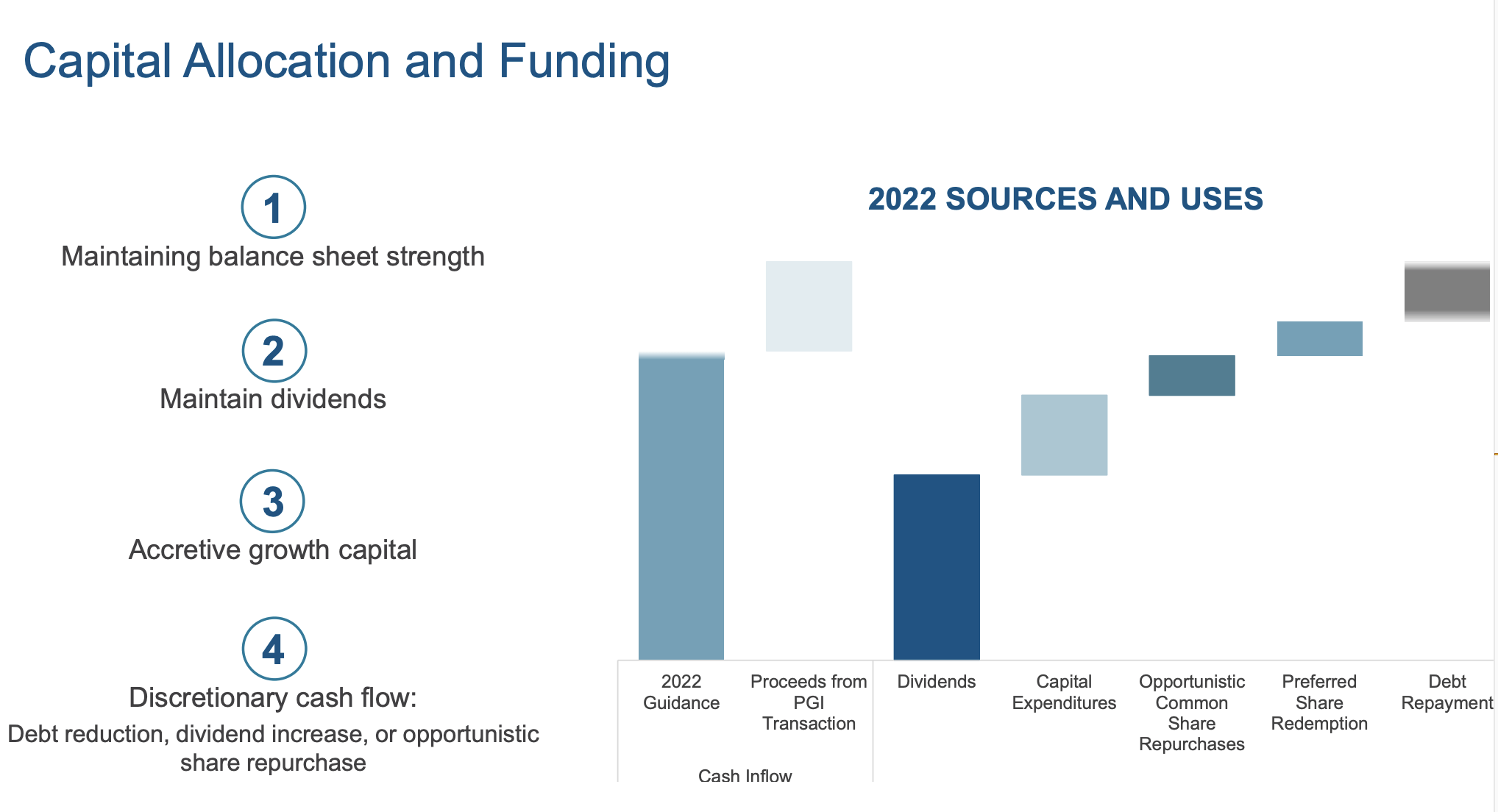

Management has guided for as little as $3.625 Billion and as much as $3.725 Billion for fiscal 2022. As a result of higher volumes and inflation adjusted tolls on conventional pipelines and fractionation facilities, a full year of higher volumes at PGI’s gas processing assets management is guiding for as much as $3.80 Billion in EBITDA for 2023 FYE. Profitability growth will likely be modest due to lower contributions from the marketing business as well as from the Alliance Pipeline and Ruby Pipelines with the latter of which filing for bankruptcy in 2022 and are accounted for under the Equity Method. Management has guided for $730 Million in CAPEX for 2023, so even with $1.416 Billion in common dividends and $124 Million in preferred dividends PPL is very much in self-funding mode (excluding the impact of taxes).

Investor Presentation December 2022 (Pembina Pipeline Corporation) Investor Presentation December 2022 (Pembina Pipeline Corporation)

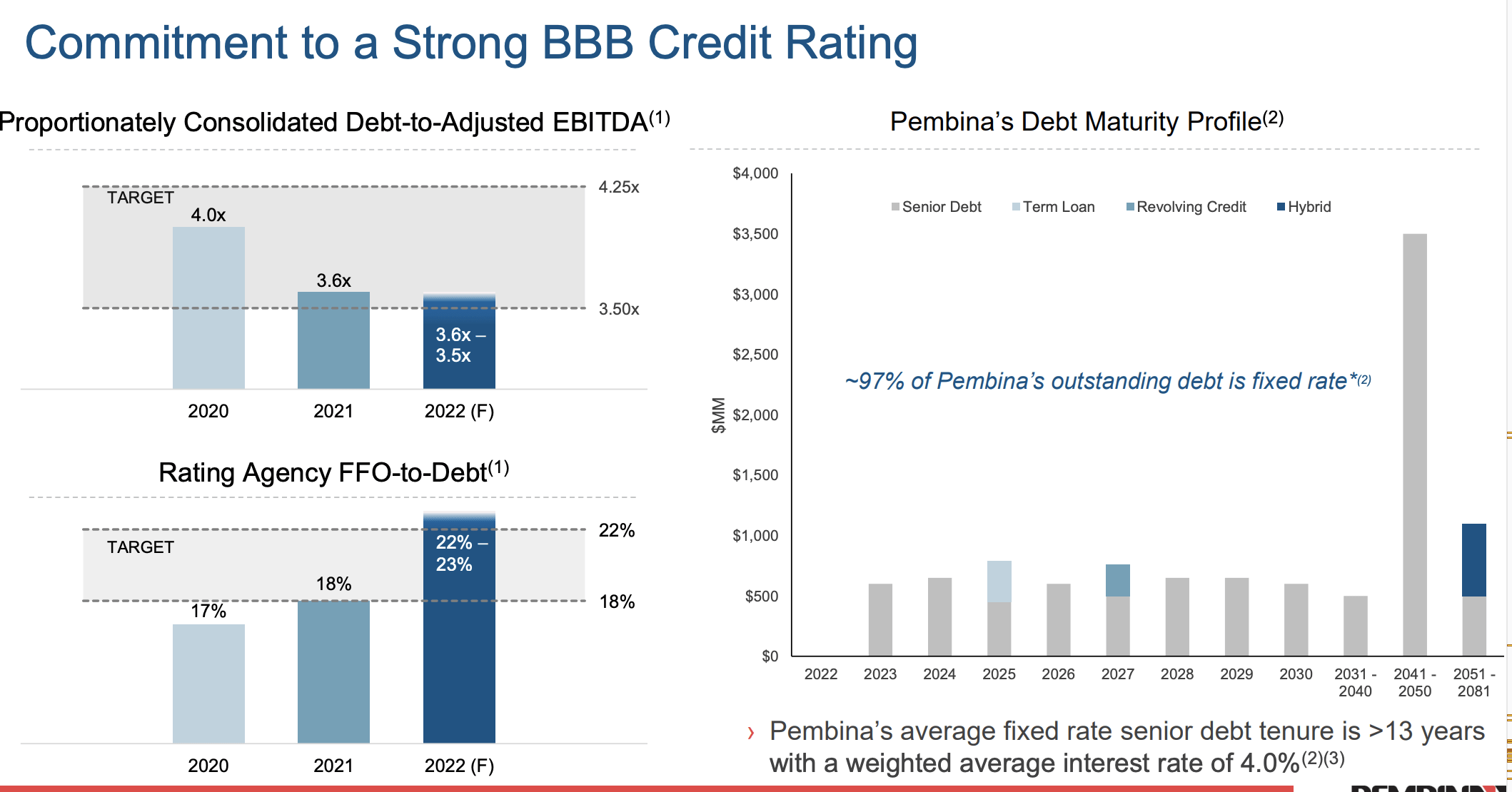

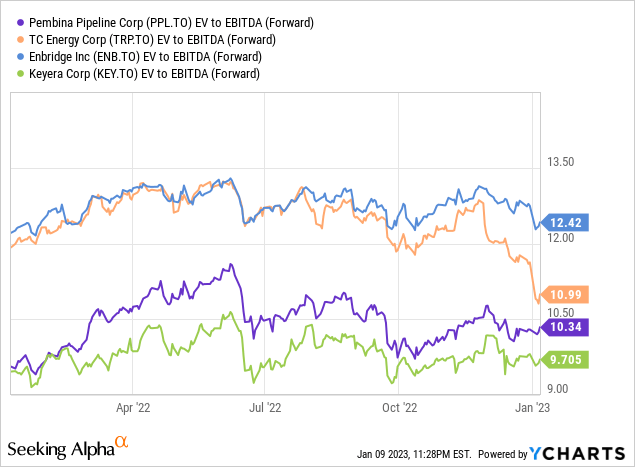

The leverage profile is also quite favourable with debt-to adjusted EBITDA at only 3.5-3.6x and debt-to-FFO of ~4.5x which makes it one of the least leveraged midstream companies in its peer group which includes Enbridge (ENB:CA), TC Energy Corporation (TRP:CA), Brookfield Infrastructure Corporation (BIPC:CA), and Keyera Corp. (KEY:CA). In addition 97% of debt outstanding is fixed rate with a well staggered maturity profile and a low weighted average interest rate of only 4% so rising interest rates should not materially impact cash flows.

Investor Presentation December 2022 (Pembina Pipeline Corporation)

The Opportunity

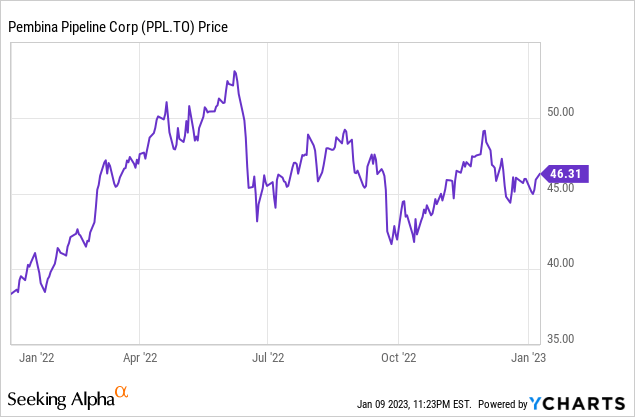

It is quite perplexing that the common shares have dropped 13% since the highs seen in June 2022 while cash flows have increased as well as the monthly common share dividend from $0.21 to $0.2175/share. The forward dividend yield will be at least 5.6%. PPL common shares are also among the cheapest in its peer group, which is perplexing given its strong leverage profile.

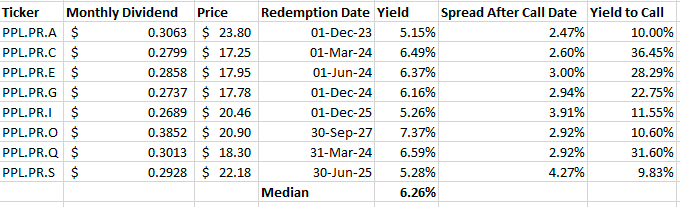

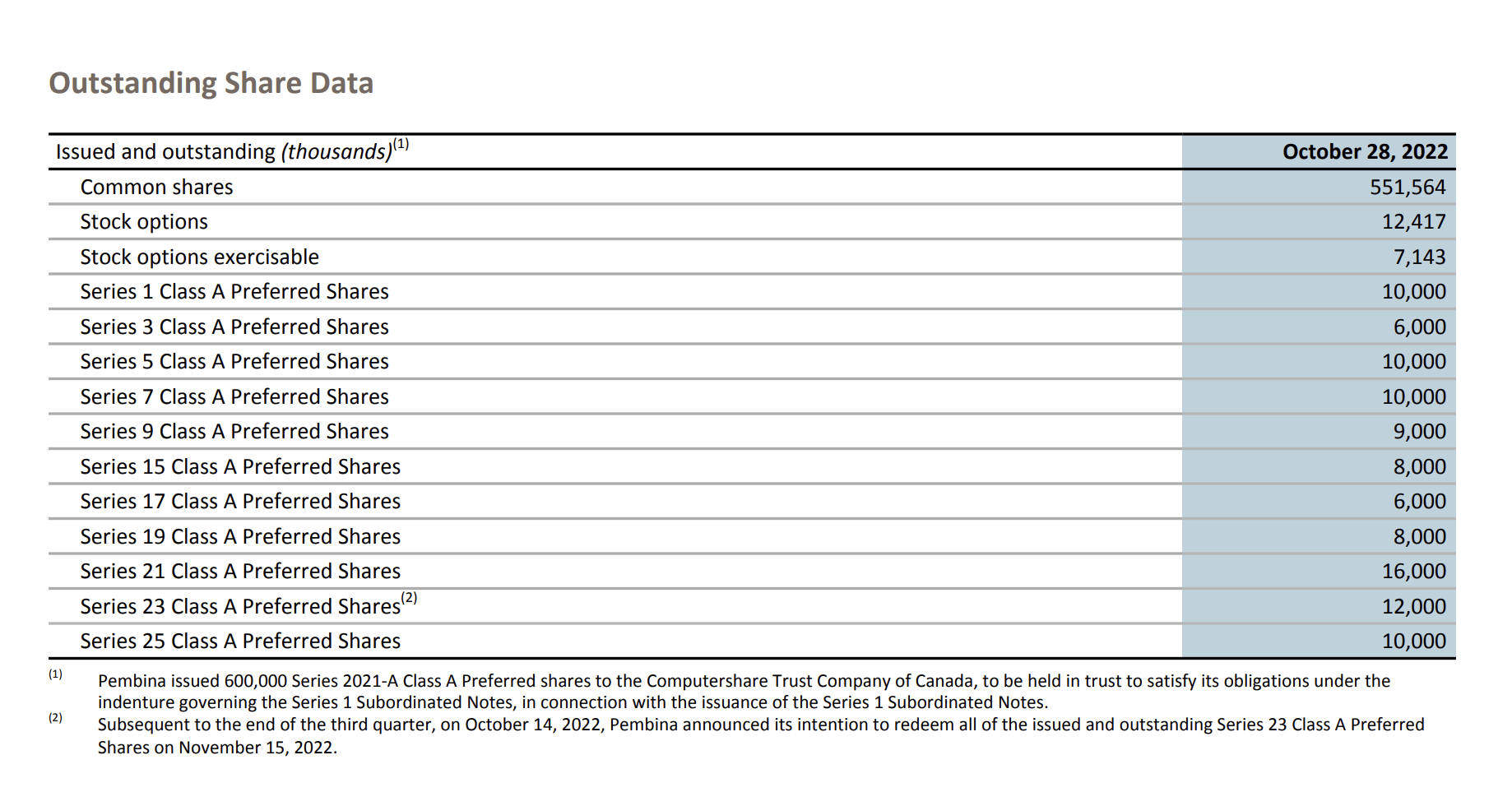

Although I am bullish on the common shares and hold some in my portfolio the preferred shares represent a lower risk way to achieve strong returns which are well covered by run-rate EBITDA. All of PPL’s preferred share offerings are presented below and are redeemable every five years and if the company chooses not to redeem they reset at the 5-year Canada Bond Yield. On October 14, 2022, Pembina announced its intention to redeem all of the 12 Million issued and outstanding Cumulative Redeemable Minimum Rate Reset Class A Preferred Shares, Series 23. The total redemption price for the Series 23 Class A Preferred Shares was $300 Million.

Authors Table (Author’s Calculations)

The Class A Series 15 (TSX:PPL.PRO:CA) represent the best opportunity from a pure income perspective. On August 31, 2022, Pembina announced that it did not intend to exercise its right to redeem the 8 Million Cumulative Redeemable Rate Reset Class A Preferred Shares, Series 15 on September 30, 2022. The annual dividend rate for the Series 15 Class A Preferred Shares for the five-year period from September 30, 2022 to September 30, 2027 is 6.164% but has a current yield of 7.37% due to its discount to par.

The Series 15 Class A Preferred Shares have the highest current yield by far 178 bps higher than the second highest and 111 bps higher than the median in the group. It also has the furthest call date and a strong yield to call rate of 10.6% which is even higher than the Series 1 (TSX:PPL.PRA:CA) which is callable in December 2023.

Investors who believe the hawkish message being dealt by the BoC may still find the Series 3 (TSX:PPL.PFC:CA), Series 5 (TSX:PPL.PFE:CA), Series 7 (TSX:PPL.PRG:CA), and Series 17 (TSX:PPL.PRQ:CA) attractive. All four issues are due in 2024. With the 5-year Government of Canada Bond rate currently at 3.24% the rates would reset for at least 5.8% on those issues. With excess cash flows and ample capacity on the $1.5 Billion Revolving Facility ($342 Million utilized) management may find it worthwhile to redeem. In fact the Series 5 has a floor of 3% so would be the most compelling to redeem. The yield to calls on these issues is at least 28% and would result in enormous returns if called. PPL.PFC has $300 Million par value outstanding, PPL.PFE and PPL.PRG have $250 Million par value outstanding, and PPL.PRQ has $150 Million in par value outstanding, therefore redeeming anyone or possibly all of these series is feasible.

Canada 5-Year Bond Yield Overview (Investing.com) Investor Presentation December 2022 (Pembina Pipeline Corporation)

There is however the mere possibility interest rates could go the other way over the next 18 months in which case the preferred shares would unlikely be called and by holding the ones that are up for redemption in 2024 would provide measly returns. For those who would prefer to not speculate on interest rates PPL.PR.O is still your best bet as the dividend is well covered by cash flows and has 59 payments to go before there is even the possibility it gets called. Assuming even a one notch downgrade from BBB to BB is fair for the preferred shares of PPL, fair value would be $22.30/share which is 6.7% above the current price of $20.90/share. High single digit or low double digit returns are far from unreasonable to expect.

Conclusion

Both the common shares and some of the preferred shares offer exceptional value. The common shares will face stiff competition from lower-risk yields on corresponding preferred shares, and in an uncertain market. There are very few midstream companies with such low leverage with preferred share yields this attractive especially the Class A Series 15 preferred shares.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment