Darren415

This article was first released to Systematic Income subscribers and free trials on Dec. 14.

At this time of year investors are bombarded with outlooks and forecasts for the coming year. In this article, we highlight a risk that often goes unmentioned but one that potentially presents the greatest danger for income investors.

What are the risks that all analysts seem to agree on? There are quite a few to pick from – inflation remaining too high, military escalation in Europe, persistence of Chinese COVID zero and further social instability in the country, Fed overtightening, a hard landing and more.

Given this risk spectrum as well as the price action this year, it’s tempting to get out of the market and only get back in when things settle down. However, this approach to investing is misguided in our view. This temptation to put capital to work only when the skies are clear presents the greatest long-term risk to investors for two main reasons.

First, we may never again see an extended period of a calm macro and market environment. Growing geopolitical tensions, deglobalization, reduced market liquidity due to regulatory-driven bank balance sheet constraints, frequent sector blow-ups, growing volatility of macro indicators like GDP and inflation, and potential for another pathogen breakthrough all suggest that volatility is probably here to stay. So rather than avoiding markets altogether, investors may as well come to grips with this development.

And second, 2021 offers a great example of why waiting for an all-clear is not a good way to approach investing. Relative to this year, 2021 was much more calm. Inflation was fairly subdued, recession was not on anyone’s radar and no one expected a war in Europe. However, what followed this very calm environment was an unprecedented storm with a major sell-off across both bonds and stocks.

Part of the reason the sell-off has been so painful is that the calm environment in 2021 came together with very expensive valuations – a very common pattern. With markets priced for perfection, there was little margin of safety for things to go wrong and wrong they went.

The situation now is very different – risk-free rates are elevated, CEF discounts are pretty wide, credit spreads are tighter than we would like but they’re not exactly tight.

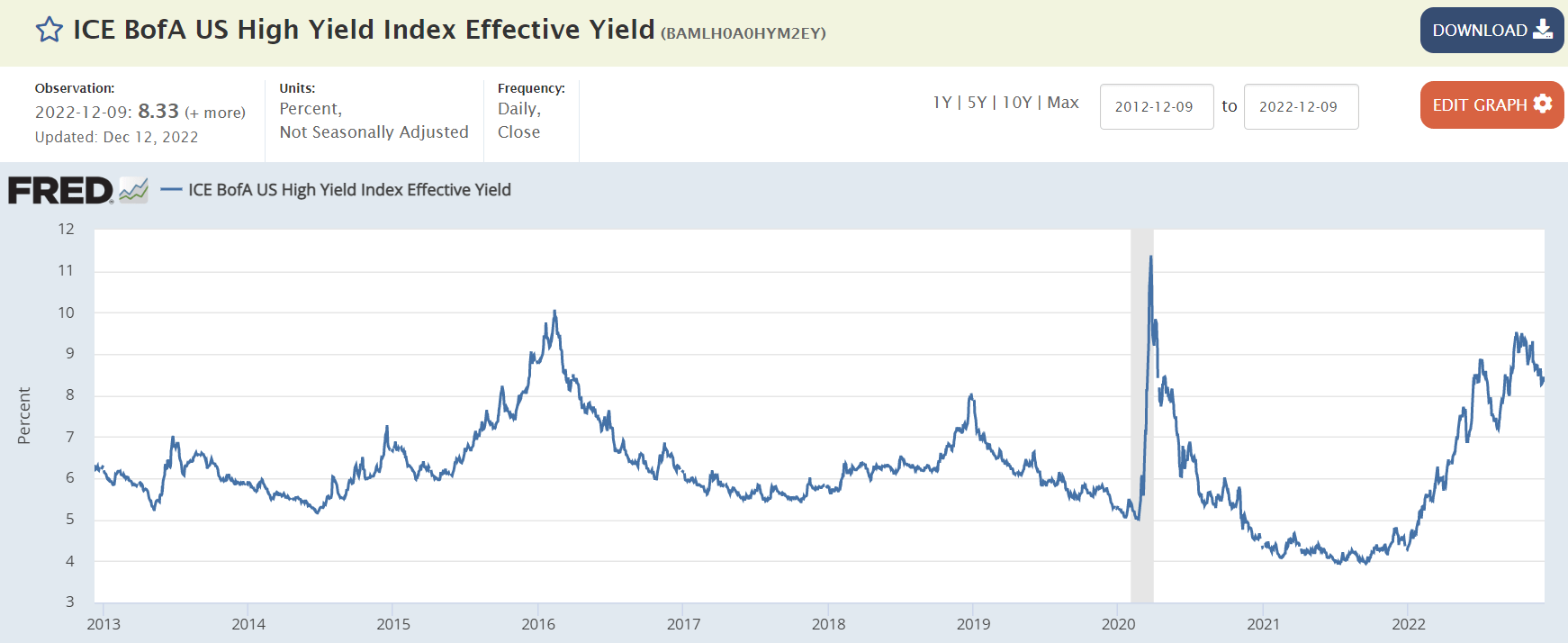

In summary, income assets are no longer priced for perfection with no margin of safety. Rather, they are priced fairly, offering decent compensation for investors if things worsen. A proxy we like to use for compensation to income investors is the high-yield corporate bond market yield shown below. Over the past 10 years, this figure has been higher only briefly. Yields were higher for an extended period during the Tech recession but not by much. And they were significantly higher during the GFC but not for long. In short, unless investors can pick the bottom in prices / top in yields with regularity, current valuations remain on the attractive side.

FRED

The current fair valuation of income assets also means that the risk to forward returns is fairly symmetric – prices could go up or down. This is in contrast to 2021 where the risk to prices was highly asymmetric – with much more downside potential than upside.

At the same time, the opportunity cost for being out of the market is much higher now than it was in 2021. For instance, BB yields (a good proxy for the preferreds sector or crossover rated corporate debt) went from 3% to 6.7% while municipal bond yields went from 1% to 4%. Clipping coupons at this higher yield level provides a greater allowance for things to go wrong as well as a higher cash-generation ability to accumulate dry powder to invest if things do turn out worse than what is currently priced in.

In short, waiting for the dust to settle down before allocating capital is unlikely to allow investors to achieve their goals. Of course, this doesn’t mean that investors need to always run their portfolios full tilt. Rather, as the experience of 2021 suggested, overall risk exposure needs to be tailored to the value on offer at any given time. Going all in when apparent risks are low and valuation is unattractive is much less compelling in our view than when valuation levels are attractive but risks are not small.

Some Ideas

Allocating capital in a difficult and uncertain environment, even when valuations are attractive can be uncomfortable. One way to mitigate this is to hold a portfolio that is diversified across various macro and market scenarios. Specifically, we continue to allocate to securities that benefit from rising short-term rates such as floating-rate preferreds and loans. However, we also hold medium-duration fixed-rate assets that can benefit if a macro slowdown is accompanied by a drop in interest rates which it very often is.

Another way to mitigate this uncertain environment is to allocate across the quality spectrum from high-quality to what we call decent-quality securities – those that are not necessarily investment-grade but not bottom-barrel either given the uncertainties around a potential recession. This two-dimensional diversification strategy across both interest rates and quality factors can provide much needed resilience for investor portfolios.

Here, we briefly highlight securities where we see value and which we continue to hold across our Income Portfolios:

- Agency Mortgage REIT Annaly Series F (NLY.PF) which has held up exceptionally well this year with a positive total return due to its floating-rate profile. The stock features a coupon of 3m Libor + 4.993% which equates to a yield a bit over 10% and which will continue to grow as the Fed continues to hike. The stock is trading sub-$25 so a redemption will provide a nice tailwind if it happens. This security provides a very attractive yield and additional tailwind if the Fed proves more hawkish than expected and/or inflation remains stickier than expected.

- Business Development Company OXSQ 2024 bond (OXSQL) which trades at a 8.95% yield and is also up on the year. The short maturity of the bond means it acts as a low-beta income asset regardless of what happens to interest rates. The benefit of a fixed-rate short-maturity security over floating-rate securities is that its price is much less likely to be affected in case the Fed starts to sharply cut rates, something which would hurt the prices of floating-rate assets as we saw in Q1 of 2020.

- CEF Nuveen Municipal Credit Income Fund (NZF) allocates to both investment-grade and unrated municipal tax-exempt bonds. The fund trades at a 10.7% discount and a 4.98% yield. It provides medium-term duration exposure as well as decent quality and can take advantage of a recessionary environment accompanied by falling longer-term interest rates.

Our key takeaway in this article is that waiting for the dust to settle before putting capital to work in the income market sounds good in theory but exposes investors to significant risks. Rising macroeconomic volatility and geopolitical tensions means we may never see the return of a totally calm environment.

Moreover, as 2021 clearly showed, a relatively calm environment can be quickly followed by multiple shocks which can decimate investor portfolios for the simple reason that a calm environment typically provides little valuation margin of safety, in contrast to today. Rather than waiting for the skies to clear, investors ought to pay more attention to valuations on offer (attractive now, less so in 2021) and diversify their portfolios across multiple risk factors. This strategy is more likely to allow investors to reach their goals.

Be the first to comment