vizualni/iStock via Getty Images

By Rob Isbitts

Strategy

Invesco S&P 500 BuyWrite ETF (NYSEARCA:PBP) aims to track an index that takes the S&P 500 and combines it with a 1-month “covered call option” position. A covered call option involves receiving a payment up front in exchange for the obligation to sell the underlying security (in this case, the S&P 500) at a certain price if it reaches that price by the option’s expiration date.

Proprietary ETF Grades

-

Offense/Defense: Offense

-

Segment: Tactical

-

Sub-Segment: Covered Call

- Risk Grade (vs. S&P 500): Low

Proprietary Technical Ratings

-

Short-Term Rating (next 3 months): Sell

-

Long-Term Rating (next 12 months): Sell

Holding Analysis

PBP buys the S&P 500 (all of it, in accordance with that index’s weighting to each stock), and supplements that by selling calls on the S&P 500 Index, with an option expiration of one month out. The option position is refreshed each month. The option position is small as compared to the total ETF assets (around 2% as of this writing). However, the “notional value” of the covered call option (the amount of stock controlled or represented by the option position) is about equal to the size of the fund. In other words, the portfolio is about fully “covered” by the option position.

Strengths

This is about as simple as the covered call writing concept gets. PBP owns the full S&P 500 and covers it with an option that expires in one month. Each month, it rolls that contract forward a month. That means that PBP gathers in option premium each month, but the portfolio of about 500 stocks is still there, performing as the S&P 500 does.

Weaknesses

I have a long-standing bias against covered call writing. Not the strategy itself. If used responsibly, it can be an excellent tool to have in one’s toolbox. But the ETF version of covered call writing seems to be more about creating a big headline with the fact that these funds bring a hefty income rate. However, what good is that high yield if you give all of it back in principal loss? As I see it, the ETF industry can be divided into 3 types of funds:

* Those that offer a solid, convenient way to access an investment strategy

* Those that exist, but add little if any value

* Those which are hyped as something that investors are innately attracted to, but the “fine print” renders them nothing more than sales gimmicks, designed to sell products to unsuspecting investors.

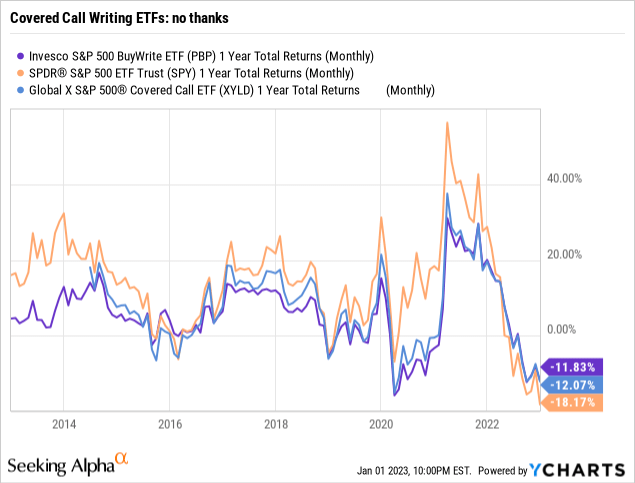

Which one does PBP fall into? You guessed it, the last one. The chart above shows PBP and also its bigger, slightly more useful peer, Global X S&P 500® Covered Call ETF (XYLD). The emphasis in that last sentence is on “slightly.”

You can see from that chart of 1-year total returns going back several years that both PBP and XYLD have a near-perfect record…of underperforming the S&P 500. Remember, PBP is the S&P 500. It just has a thin, additional layer that collects option premium each month. Sounds like a fun way to spice up your S&P 500 investing experience, eh? Not so much. The bottom line is that these funds have habitually added no consistent value. I would not ever expect them to outperform the un-covered S&P 500 during a sustained bull market move. But in rougher times, that option premium has to provide some sort of buffer. It doesn’t.

Opportunities

The main opportunity here, as our rating implies, is to sell this ETF. As noted, XYLD is a slightly better option (pun intended), but it is not the subject of this report. And so the Sell rating on PBP is not an implicit opinion about XYLD.

Threats

In the case of PBP, it has a double-whammy. Not only is it a way to consistently underperform the S&P 500, it doesn’t yield very much. And, since the total portfolio is “covered” by the option, that means your upside is limited. So, it is the worst of both worlds, so to speak. The S&P 500 ETF (SPY), while not something I recommend, at least gives you 1:1 tracking of that index. PBP often trails on the way up and the way down, as the graph shows. PBP is truly an ETF for no seasons. And, while PBP’s asset base is deservedly a fraction of what it once was, there is still more than $100mm of investors’ wealth in it.

Conclusions

ETF Quality Opinion

This ETF’s only redeeming quality is that it is simple and transparent. But ETFs typically are, so that is nothing to celebrate. The covered call concept is potentially attractive, but not at all in this specific form.

ETF Investment Opinion

We rate PBP a Sell, for all of the reasons noted above. Consider it the ETF equivalent of a “spam call.” Don’t answer it.

Be the first to comment