mariusz_prusaczyk/iStock via Getty Images

Investment Thesis

Peabody Energy (NYSE:BTU) had already pre-announced its Q2 2022 results, so investors should not have been surprised by its results.

What was disappointing and weighs on the stock is that Peabody’s 2022 operational performance does not seem to catch a break. More specifically, through a combination of weather, COVID-related absenteeism, and rail availability, Peabody had to revise its volume of coal sales downwards.

Clearly, with coal prices so hot right now, this isn’t causing investors to become too sour, nevertheless, investors would still wish for Peabody to be able to improve its performance.

That being said, with the stock priced at approximately 3x EPS, investors are already pricing in a lot of negativity.

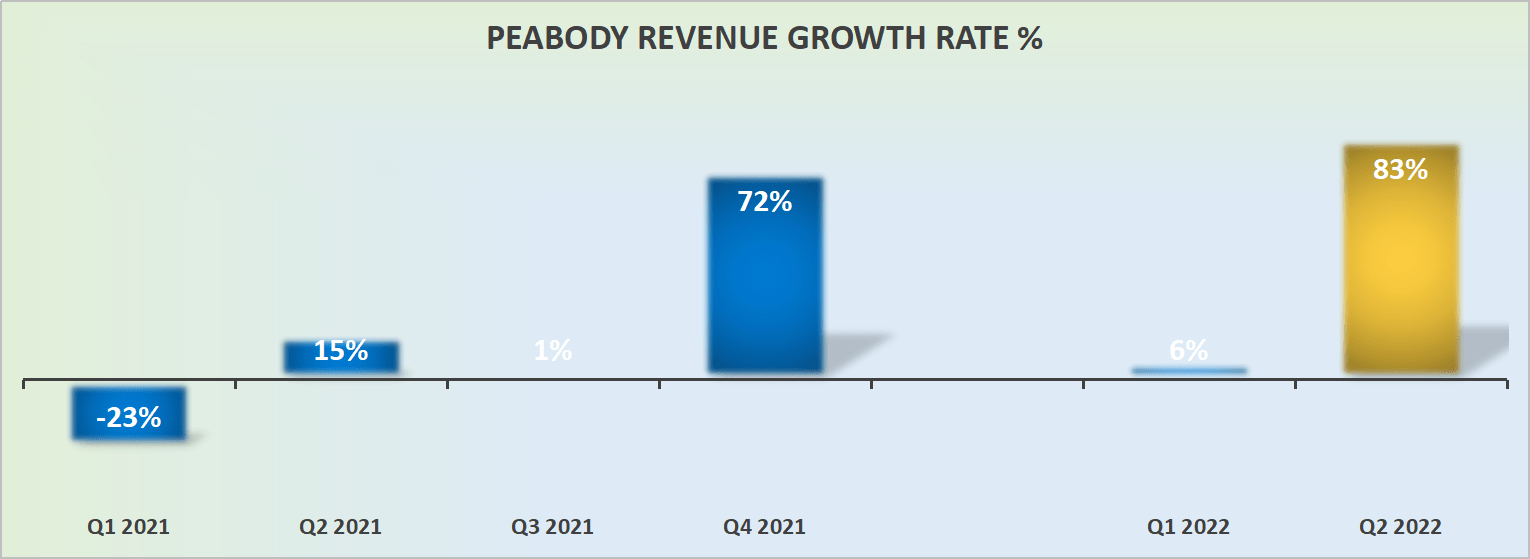

Peabody Energy’s Revenue Growth Rates Come In Strong

Peabody revenue growth rates

As a reminder, Peabody had pre-announced its Q2 results. Consequently, given that its revenues came in squarely within the midpoint of its guidance, should not have surprised investors.

And while Peabody doesn’t give any formal guidance on how Q3 is likely to come in, we do get a sense that Q3 is expected to see yet another quarter of strong growth.

However, the question as always is, just how strong?

Peabody’s Near-Term Prospects

Anyone following Peabody or the coal sector will know that demand for coal is sky high, particularly thermal coal. Yet, for now, Peabody continues to be restricted in benefitting from this strong demand on the back of poor rail availability.

Poor rail availability has been an issue throughout the first half of 2022, and the commentary on the earnings call implies that although there will be an improvement in the second half of 2022, that full availability is not expected until 2023.

Rail has been the confining factor to-date, assuming that rail is fixed and in regular conversations with rail providers and expect that to be fixed here as we go through the second half of this year and be back to full service levels next year. (Q2 2022 earnings call)

Separately, it’s worth noting that although investors have been allured toward thermal coal players, we should keep in mind that Peabody has exposure to both thermal and metallurgical coal.

And perhaps less obvious, but nevertheless, it is crucial to note that this time last year, Peabody’s Seaborne Metallurgical segment was running at a slight loss.

And not only did this turn around in Q1 2022, but in Q2 2022, the Seaborne Metallurgical segment saw its EBITDA reach approximately $300 million.

Accordingly, as of Q2 2022, just over half of Peabody’s total adjusted EBITDA comes from its progress on its Seaborn Metallurgical operations.

Moreover, keep in mind what Peabody’s peer, Arch Resources (ARCH) said during their earnings call:

It is nearly unprecedented to have thermal coal trading at a premium to coking coal and we don’t expect that to last.

Both Arch and Peabody made similar comments on this front.

Further emphasizing that peers in the coal space also expect metallurgical coal to remain strong over the near term, thus providing Peabody with further tailwinds to its operations.

Capital Returns Discussed

Peabody has no capital return program. This was noted during the earnings call:

We expect to continue that course and so we’ve eliminated the secured debt. We have about $600 million of that remaining. And once that’s repaid, we’ll then look to address the unfunded $320 million LC facility that matures in 2024. That facility is used right now for noncash collateral for the reclamation liabilities. That needs to be replaced as we continue to fund long-term reclamation liabilities.

Peabody may be making a lot of free cash flow per quarter, indeed, Q2 2022 saw Peabody make $324 million of free cash flow, but until Peabody has repaid debt holders Peabody will not be able to return any capital to shareholders.

BTU Stock Valuation – 3x EPS

Peabody is priced at somewhere near 3x this year’s EPS. We are now just 4 months from finishing 2022, and investors are increasingly starting to price in 2023. And wherein lies the big question.

Can investors truly bank on 2023 being just as good as 2022? Some would argue that 2022 saw a one-off spike in energy demand, while some expect 2023 to be largely the same as 2022.

Nevertheless, there’s clearly a significant amount of uncertainty on the cards. And given that Peabody doesn’t have any meaningful way to return capital to shareholders for at least another 12 months, if not longer, investors are having to bank on coal prices remaining stronger for longer.

The Bottom Line

When it comes to investing in coal stocks, the theme in 2022 has been largely consistent. Every quarter analysts upwards revise the next quarter and ”forecast” that the demand for coal is going to be robust for yet another period.

The same is happening here, where analysts now expect Q3 2022 to be on par with Q2, and up significantly y/y.

However, for investors, only one thing can possibly excite them, and that is to see Peabody returning capital to shareholders. And on this front, for now, investors are having to remain patient. The most expensive activity at the best of times. But in this market? When short-termism is ruling the day, investors are showing very little patience, irrespective of the stock being valued at approximately 3x earnings.

Be the first to comment