AsiaVision/E+ via Getty Images

A Quick Take On Dada Nexus

Dada Nexus (NASDAQ:DADA) went public in June 2020, raising $320 million in an upsized offering of 20 million ADSs.

The firm operates as an online grocery platform for consumers in China.

Until management can start to make serious progress towards operating breakeven while maintaining growth, I’m on Hold for DADA, although the stock is worth putting on a watch list.

Overview

Shanghai, China-based Dada was founded to provide consumers with food and grocery goods delivered to their home or place of business via their on-demand online system and mobile app.

The company was founded by Philip Kuai, who was previously vice president of Anjuke.com, an online real estate platform in China.

The company’s primary offerings include:

-

Dada Now – Delivery from merchants and individual senders

-

JDDJ – Delivery & marketing between brand owners, retailers & consumers

The firm provides its intra-city services to more than 700 cities and counties in China and its last-mile services to more than 2,400 cities and counties.

DADA sells its services to retailers and brands and provides a range of related services including integrated e-commerce websites to enhance delivery efficiency.

The company has deep relationships with large retailers like Walmart, JD.com, Yonghui and CR Vanguard.

The firm also recruits riders to provide delivery services. As of March 31, 2020, its network counted more than 634,000 active riders (delivery providers).

Market

According to a 2019 market research report referenced by China Daily, the market for food delivery services reached nearly $66 billion in 2018.

This represents a 112% increase from the previous year.

The market is expected to more than double by 2021, with the effects of the Covid 19 pandemic likely to increase demand substantially due to the increased desire of consumers to receive their food and groceries via delivery.

The largest players in the industry also include Meituan and Ele.me and China’s ride-hailing firm Didi also entered the market in 2018.

Recent Financial Performance

-

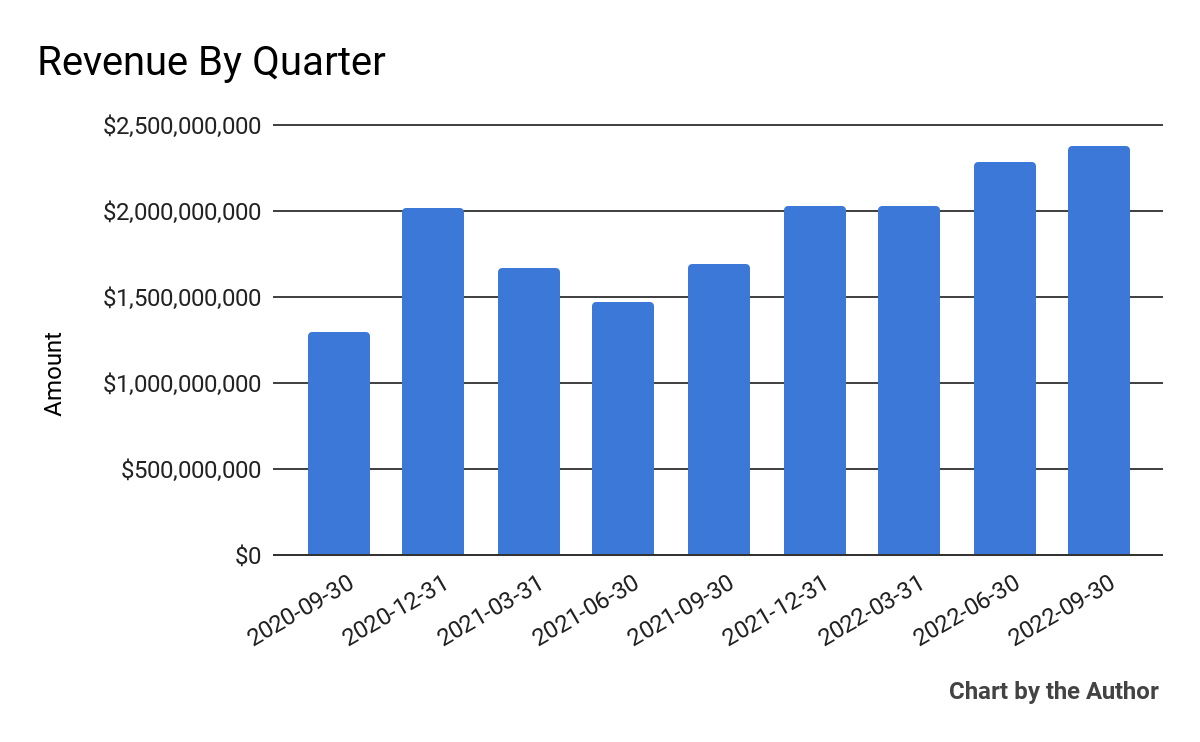

Total revenue by quarter has risen markedly in recent quarters:

9 Quarter Total Revenue (Financial Modeling Prep)

-

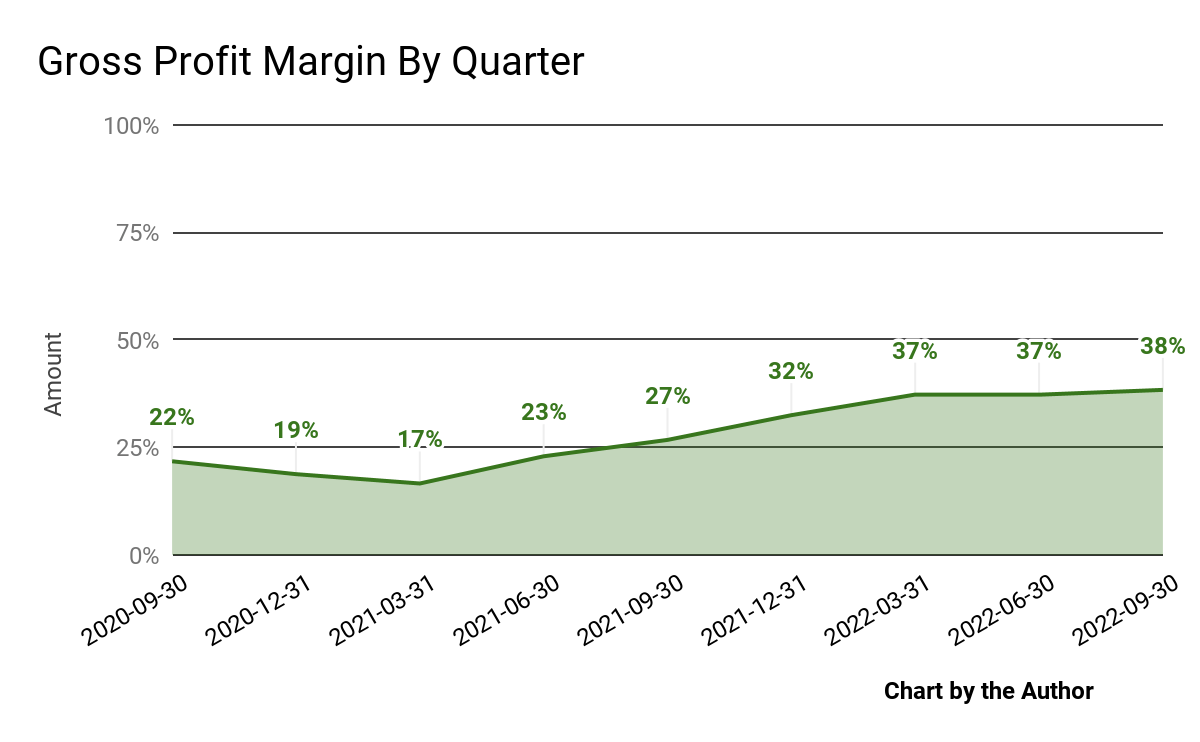

Gross profit margin by quarter has also grown appreciably, as the chart shows below:

9 Quarter Gross Profit Margin (Financial Modeling Prep)

-

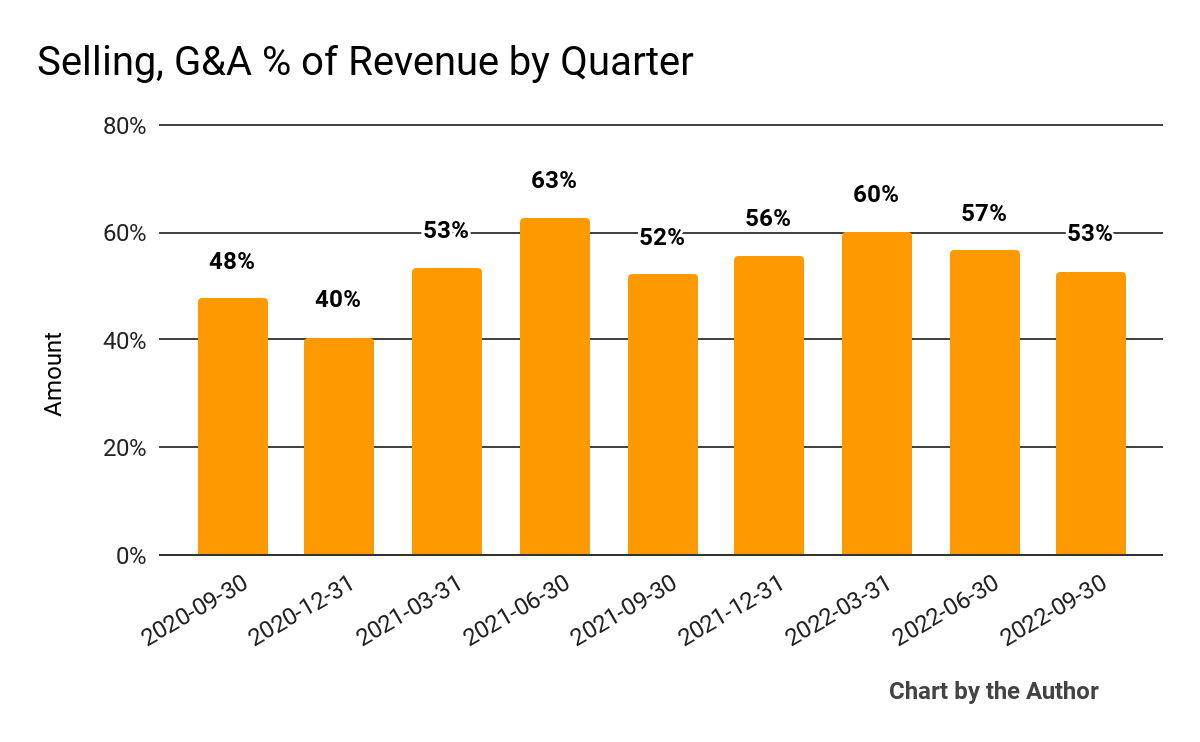

Selling, G&A expenses as a percentage of total revenue by quarter have varied as follows:

9 Quarter Selling, G&A % Of Revenue (Financial Modeling Prep)

-

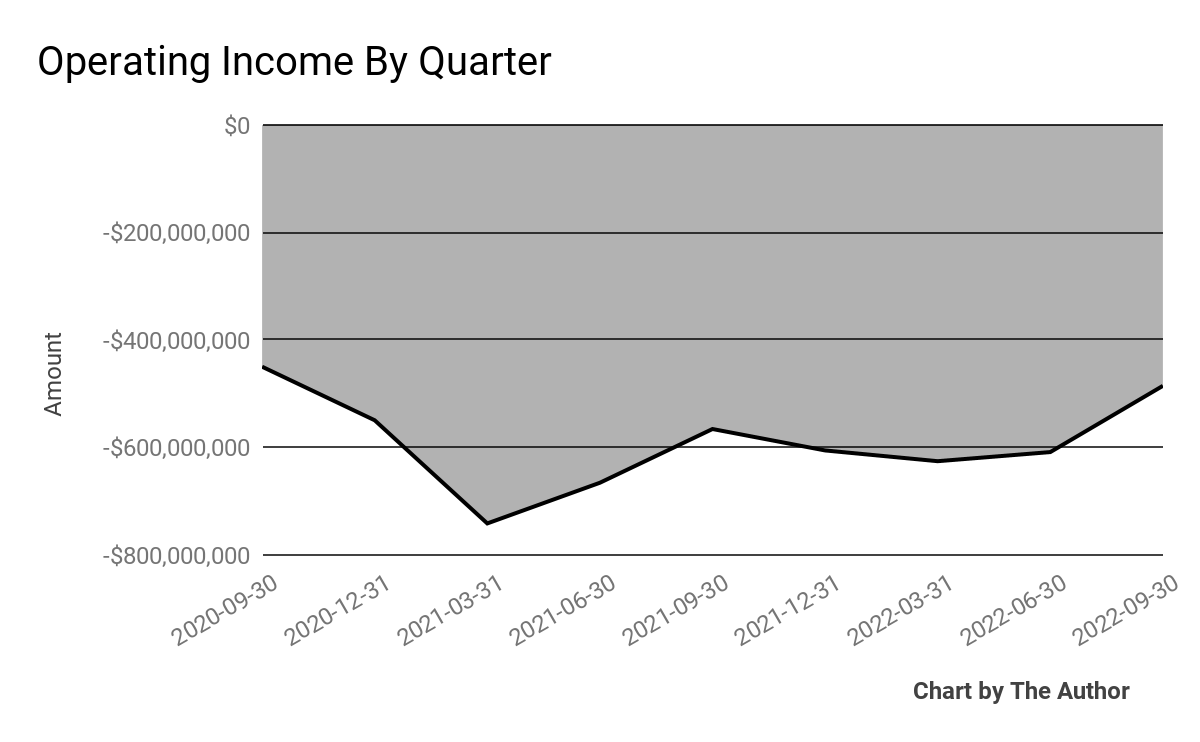

Operating losses by quarter have remained substantial:

9 Quarter Operating Income (Financial Modeling Prep)

-

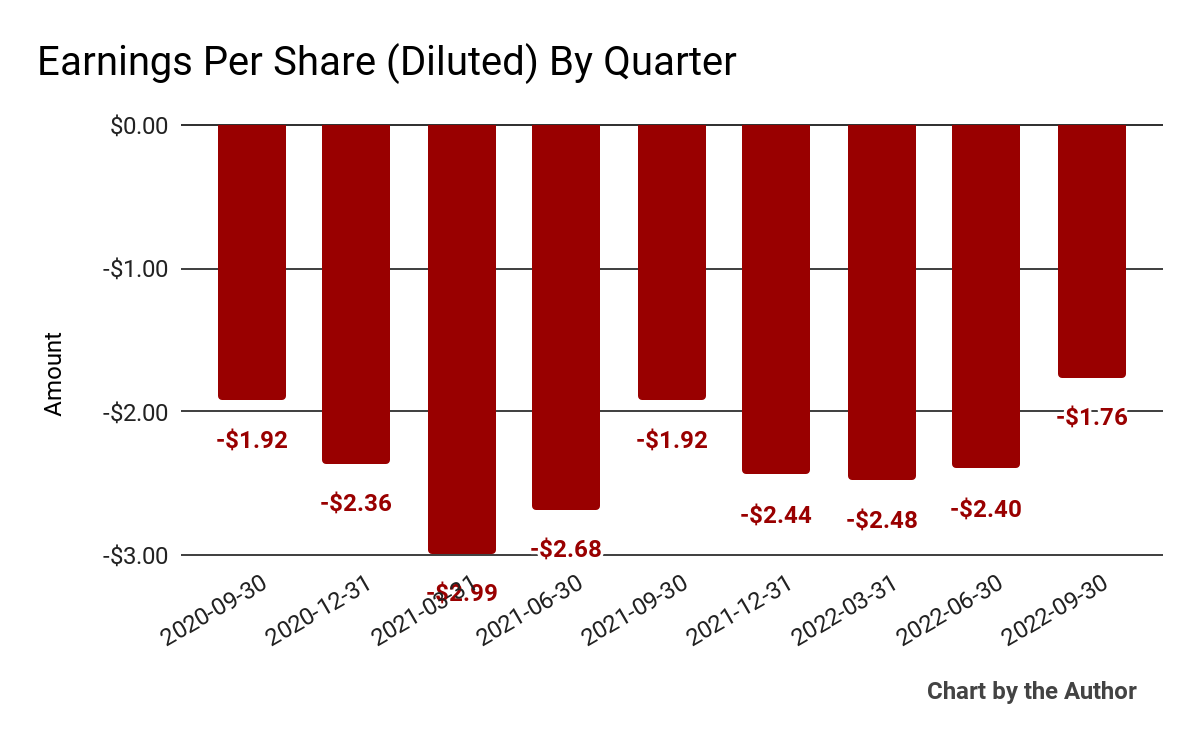

Earnings per share (Diluted) have also remained heavily negative:

9 Quarter Earnings Per Share (Financial Modeling Prep)

(All data in the above charts is GAAP)

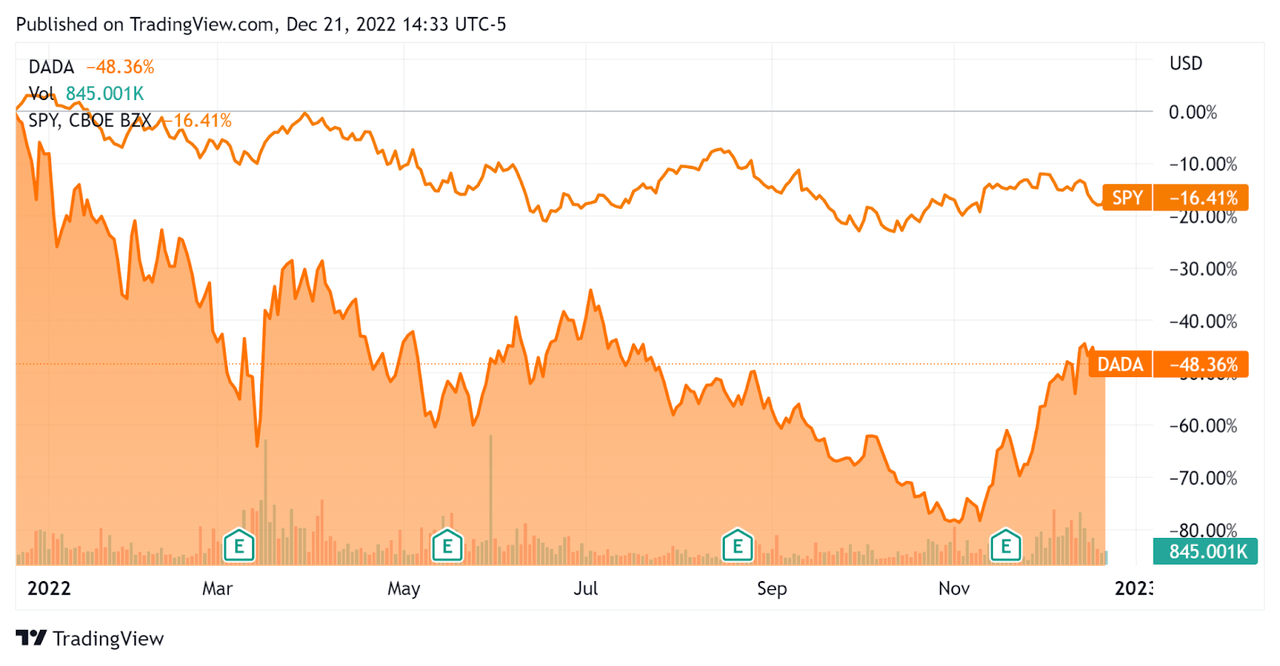

In the past 12 months, DADA’s stock price has fallen 48.4% vs. the U.S. S&P 500 index’s drop of around 16.4%, as the chart below indicates:

52-Week Stock Price Comparison (Seeking Alpha)

Valuation And Other Metrics

Below is a table of relevant capitalization and valuation figures for the company:

|

Measure [TTM] |

Amount |

|

Enterprise Value / Sales |

0.2 |

|

Enterprise Value / EBITDA |

-0.9 |

|

Revenue Growth Rate |

27.3% |

|

Net Income Margin |

-25.4% |

|

GAAP EBITDA % |

-25.5% |

|

Market Capitalization |

$1,863,243,752 |

|

Enterprise Value |

$2,062,599,125 |

|

Operating Cash Flow |

-$244,540,000 |

|

Earnings Per Share (Fully Diluted) |

-$9.08 |

(Source – Financial Modeling Prep)

As a reference, a relevant partial public comparable would be Meituan (OTCPK:MPNGF); shown below is a comparison of their primary valuation metrics:

|

Metric [TTM] |

Meituan |

Dada Nexus Limited |

Variance |

|

Enterprise Value / Sales |

4.6 |

0.2 |

-94.9% |

|

Enterprise Value / EBITDA |

0.0 |

-0.9 |

— |

|

Revenue Growth Rate |

24.8% |

27.3% |

9.9% |

|

Net Income Margin |

-5.2% |

-25.4% |

386.7% |

|

Operating Cash Flow |

$1,250,000,000 |

-$244,540,000 |

-119.6% |

(Source – Seeking Alpha and Financial Modeling Prep)

Commentary On Dada Nexus

In its last earnings call (Source – Seeking Alpha), covering Q3 2022’s results, management highlighted the growth of its partnership with JD.com, with its JDDJ segment.

The company has also further invested in partnerships with large supermarket chains, stating that it has ‘now established a partnership with 88 out of the top 100 supermarket chains in China.’

For its Dada Now segment, the firm has produced significant growth due in part to lower-tier city expansion and while optimizing its unit economics.

As to its financial results, total net revenue rose 41% year-over-year while gross profit margin also increased markedly.

Of the 41% net revenue growth, JDDJ accounted for 44% growth, while Dada Now grew by 36%.

GAAP operating losses, while still very heavy, improved year-over-year as did negative earnings per share.

The company is still spending heavily on ‘incentives to JDDJ consumers, an increase in advertising and marketing expenses to attract new consumers to JDDJ platform and the amortization of the business cooperation agreement arising from share subscription transaction with JD.com in February this year.’

For the balance sheet, the firm finished the quarter with $699.3 million in cash, equivalents and short-term investments and $14.1 million in short-term borrowings.

As of quarter end, the company had repurchased 57 million ADSs out of a 70 million ADS repurchase program.

Looking ahead, management guided to 32.5% revenue growth at the midpoint of the range for Q4 2022.

Regarding valuation, the market is valuing DADA at significantly lower multiples than competitor Meituan despite Dada’s stronger topline revenue growth rate.

The primary risk to the company’s outlook is the unknown impact of the sharp rise in COVID-19 cases in China over the coming months, as the previous ‘zero-COVID’ is being dropped.

A potential upside catalyst to the stock could include stronger growth due to greater Chinese consumer desire to have grocery products delivered and continuing optimization strategies as the company pursues lower-tier city penetration.

For me, the big unknown is the effect of the COVID resurgence on the firm’s business, which could be a boon, a bust, or no real net change.

For optimistic investors, DADA’s recent growth surge may be cause for interest in the stock, but the company is still generating enormous operating losses as it spends on customer ‘incentives’ in its JDDJ segment.

Until management can start to make serious progress towards operating breakeven while maintaining growth, I’m on Hold for DADA, although the stock is worth putting on a watch list.

Be the first to comment