Torsten Asmus

By Valuentum Analysts

With the markets swooning during 2022, investors may be looking to de-risk their portfolios by adding a few high-yielding stocks here and there. Strong dividend payers also held up better than other areas in the market last year, and this resilience may continue.

There are hundreds of dividend stocks to choose from, so we ran a screen of stocks that were yielding at least 5% and had at least 15 consecutive years of dividend growth for further examination. There were a few that met the criteria of this screen, and three stocks stood out to us in particular. Let’s have a look.

Verizon (VZ)

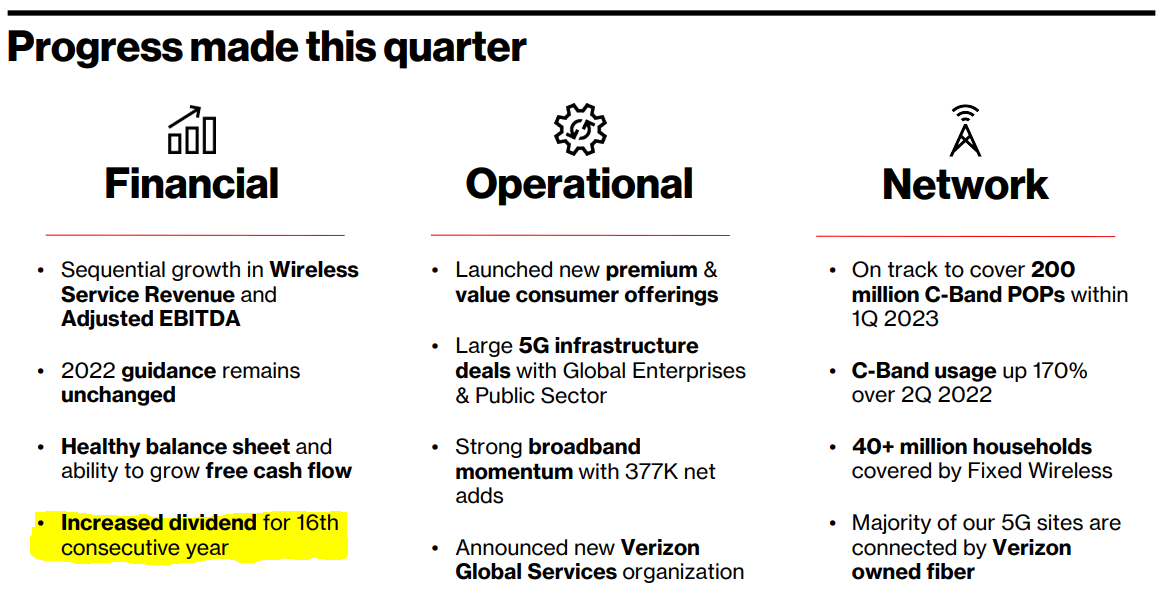

Verizon has increased its dividend for the past 16 consecutive years. (Image Source: Verizon)

Everybody knows Verizon. Perhaps its “Can You Hear Me Now” commercials were among the most impactful that we’ve seen in the wireless arena. Do you remember them? Verizon’s stock was down more than 25% on a price-only basis during the past year, but this has only padded its dividend yield, which stands at ~6.5% at the time of this writing. Verizon is trading at ~7.7x current earnings estimates, too.

But all of this may be a bit misleading. A company’s price-to-earnings (P/E) ratio may say little about whether the stock is cheap or not. For entities with simple capital structures, a company’s value is determined by summing up its discounted enterprise future free cash flows, subtracting its net debt to arrive at equity value, and then dividing by shares outstanding. Sometimes, companies should have low P/E ratios, if there massive net debt positions pressure their equity values.

This is the case with Verizon, and why the company has both a high dividend yield and low P/E ratio. As of the end of the third quarter, Verizon had total debt of $147.9 billion, which is a massive amount, particularly when compared to its meager $2.1 billion cash position. When we perform our discounted cash flow valuation of Verizon, we arrive at a fair value estimate of $44 per share, meaning that to a large degree, Verizon’s high-single-digit P/E is justified.

That said, Verizon is also a strong free cash flow generator, and the company has been able to generate free cash flow in excess of cash dividends paid. For example during the first nine months of 2022, Verizon’s free cash flow generation stood at $12.4 billion, which is greater than the $8.1 billion in cash dividends paid over the same time horizon. The free cash flow coverage of the dividend has fallen from last year’s stronger performance, but it still remains decent.

It’s hard to dislike Verizon’s 16-year dividend growth track record, but investors should know that just because a stock has a low P/E ratio doesn’t make it cheap. Deteriorating free cash flow coverage of the dividend and a massive net debt position are just two of the many concerns we have with Verizon’s shares. An investment in Verizon is not without substantial risks.

Walgreens Boots (WBA)

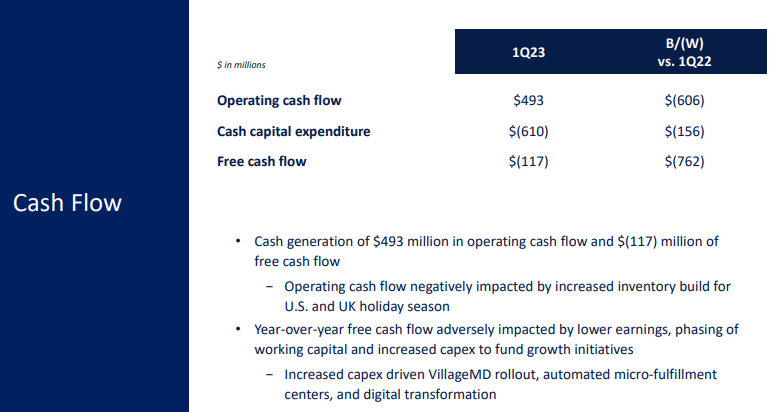

Walgreens’ free cash flow has fallen into negative territory during the first quarter of fiscal 2023 after deteriorating during fiscal 2022. (Image Source: Walgreens Boots)

Walgreens used to be a simple story prior to its purchase of Alliance Boots years ago. The company has continued its acquisitive path in recent years, and despite the firm’s strategic initiatives, its stock was among the worst performers in the Dow Jones Industrial Average during 2022. Unlike Verizon, Walgreens Boots debt load isn’t out of control, with long-term debt of $10.62 billion and short-term debt of $1.06 billion versus cash of $1.36 billion and marketable securities of $1.11 billion at the end of August 2022.

What has pressured Walgreens’ stock, however, driving its dividend yield higher, has been its deteriorating traditional free cash flow performance, as measured by cash flow from operations less all capital spending. It wasn’t but during fiscal 2021 that the company generated $5.55 billion in operating cash flow and spent $1.38 billion in capital spending, good enough for free cash flow generation of $4.18 billion, which was far in excess of the cash dividends of $1.62 billion it paid during that fiscal year.

However, during fiscal 2022, Walgreens’ cash flow from operations dropped to $3.9 billion while capital spending jumped to $1.73 billion. Though free cash flow for the fiscal year of $2.17 billion was still in excess of the cash dividends paid of $1.66 billion, one can see what some are getting a bit concerned about Walgreens’ dividend health. Quite simply, free cash flow coverage of the dividend has fallen, and this continued into the first quarter of 2023, where free cash flow was negative, falling $762 million on a year-over-year basis.

We’re concerned about Walgreens’ dividend health in light of free cash flow trends, but that may present an opportunity for income investors if the firm can get things back on track, which unfortunately is far from guaranteed. Walgreens has raised its dividend in each of the past 47 years, and while its ~5.4% dividend yield is attractive, the company’s fundamentals have seen better days. Investors should be cautious on this struggling component of the Dow Jones Industrial Average.

Enterprise Products Partners (EPD)

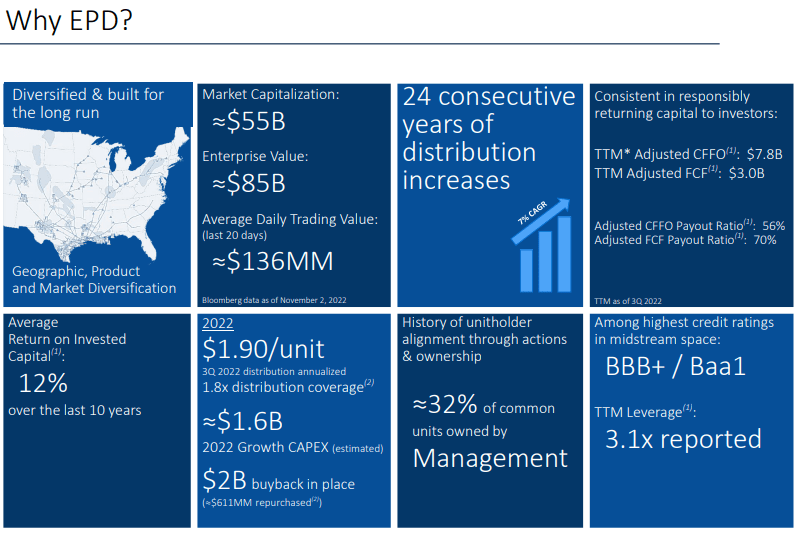

Enterprise Products Partners has put up 24 consecutive years of dividend increases. (Image Source: EPD)

Historically, we’ve been cautions on the midstream energy arena in light of their huge net debt positions and traditional free cash flow generation, as measured by cash flow from operations less all capital spending, that often has come up short relative to cash dividends paid. However, the numbers are looking much better for energy pipeline master limited partnerships [MLPs] more recently.

During the first nine months of 2022, for example, Enterprise Products Partners hauled in $5.31 billion in cash flow from operations and spent only $1.2 billion in capital expenditures, resulting in free cash flow of $4.11 billion, which handily covered its distributions paid over the same time period of $3.2 billion. Enterprise Products Partners still retains a massive net debt position of ~$29 billion, but this free cash flow coverage of the payout is solid.

Things have changed for the better for most of the midstream MLP group during the past five years, and if we had to probably pick our favorite idea among the three ideas on this list, it would be Enterprise Products Partners. The MLP has among the highest credit ratings in the midstream space, and it has backed that up with 24 consecutive years of dividend increases. Shares yield ~7.6% at this time.

Concluding Thoughts

These three companies are at the high end of the risk spectrum, in our view. Though each of them has a strong dividend growth track record of at least 15 years while boasting a dividend yield north of 5%, all three have rather large net debt positions that weigh on their valuations. Verizon’s net debt position is uncomfortably huge, and that’s something that’s worth monitoring closely, as is Walgreen’s deteriorating free cash flow generation relative to its payout. Though it, too, has a large net debt position, Enterprise Products Partners may be the cleanest story among these three considerations, while it boasts the highest dividend yield on this list. If you enjoyed this list, please consider reading: 3 Stocks With 8%+ Yields And 10 Consecutive Years Of Dividend Growth. Thank you!

This article or report and any links within are for information purposes only and should not be considered a solicitation to buy or sell any security. Valuentum is not responsible for any errors or omissions or for results obtained from the use of this article and accepts no liability for how readers may choose to utilize the content. Assumptions, opinions, and estimates are based on our judgment as of the date of the article and are subject to change without notice.

Be the first to comment