(This article was co-produced with Hoya Capital Real Estate)

alicat/E+ via Getty Images

Introduction

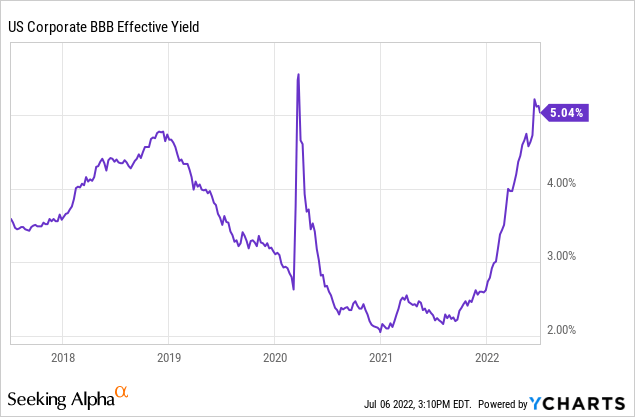

Most experienced Fixed Income investors know PIMCO as a major player in managing debt CEFs, having a total of 19 entries, including five they classify as Corporate funds, versus Multi-Sector or Muni-focused. Despite holding assets other than corporate debt, the PIMCO Corporate & Income Strategy Fund (NYSE:PCN) is listed under that tag. As the above chart shows, the recent interest-rate environment has not been helpful to Fixed Income assets.

PIMCO Corporate & Income Strategy Fund review

Seeking alpha describes this CEF as:

The investment seeks high current income with secondary objectives of capital preservation and appreciation. The fund invests at least 80% of its total assets in a combination of corporate debt obligations of varying maturities, other corporate income-producing securities, and income-producing securities of non-corporate issuers. It normally invests at least 25% of its total assets in corporate debt obligations and other corporate income-producing securities. The fund invests up to 25% of its total assets (measured at the time of investment) in non-U.S. dollar denominated securities. PCN started in 2001. Benchmark: ICE BofA US HY TR USD.

Source: PCN (Seeking Alpha)

PIMCO adds these statements explaining their investment strategy:

Using a dynamic asset allocation strategy that focuses on duration management, credit quality analysis, risk management techniques, and broad diversification among issuers, industries and sectors, the multi-sector fund seeks high current income, with a secondary objective of capital preservation and appreciation.

The portfolio manager attempts to identify investments that provide high current income through fundamental research, driven by independent credit analysis and proprietary analytical tools, and also uses a variety of techniques designed to manage risk and minimize exposure to issues that are more likely to default or otherwise depreciate in value over time.

Source: PCN (PIMCO)

PCN has $520m in assets and shows a Forward yield of 10.5%. PIMCO charges 115bps in fees, broken down as:

- Management fees: 81bps

- Other costs: 4bps

- Leverage expenses: 30bps

Current leverage is about 39%, financed mostly via Reverse Repurchase Agreements (33.6%), with equal amounts of Preferred shares and Credit Default Swaps (2.6% each).

Holdings review

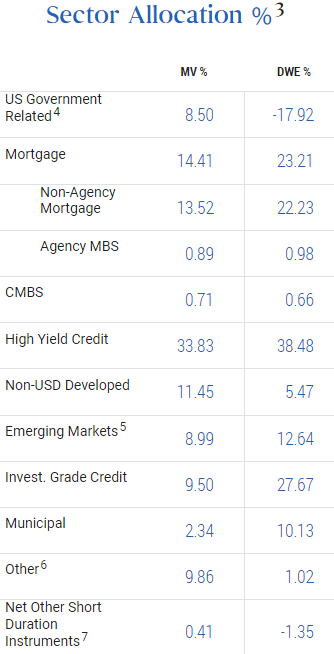

The next chart shows why I first wondered PIMCO classifies PCN under Corporates and not Multi-Sector. My calculation shows about 25% of the portfolio is in non-corporate type instruments, thus Corporate debt is the driving force behind the portfolio, which probably determined the classification.

PCN holdings (PIMCO)

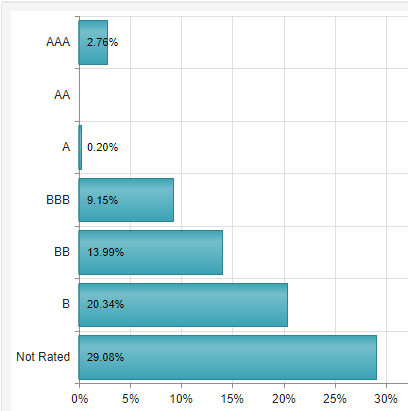

About 40% of the EM exposure is Sovereign debt, the rest Corporates. The portfolio is heavily weighted to non-investment-grade assets. Some of the non-rated could be investment-grade but my data sources didn’t show individual ratings to gauge that possibility.

PCN (CEFConnect)

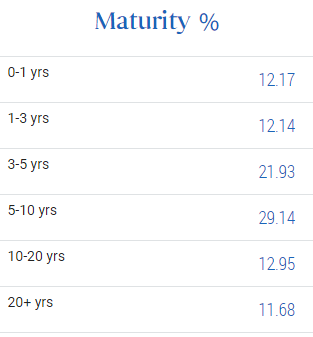

PCN shows a 3.6-year duration and 8.9-year average maturity, with the following maturity allocations:

LCN maturity (PIMCO)

With 24.3% of the portfolio maturing over the next three years, half of that in the next year, PCN has an opportunity to pick up new debt at more favorable coupons than those retiring. While the current average coupon is 5.6%, the WAC for assets maturing thru 2025 is closer to 6%. That factor and the sub-4-year duration help protect the CEF’s NAV if rates continue to climb over the next year or two. Currently, the average bond price is $90.72.

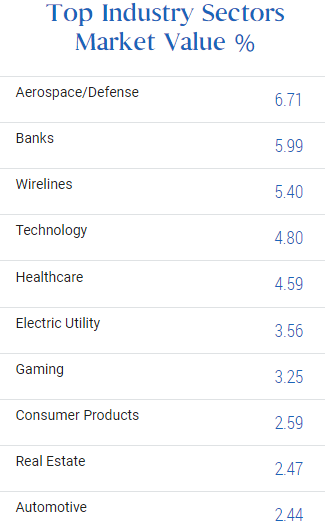

The corporate debt (bonds/loans) is spread out very well across industries, with no one dominating the list.

Industries (PIMCO)

Based on market value, the portfolio is 80% in US assets, with the UK, Brazil, Luxembourg, and Italy accounting for most of the foreign holdings. PCN does trade Currency futures to minimize the effect of currency movements against the USD.

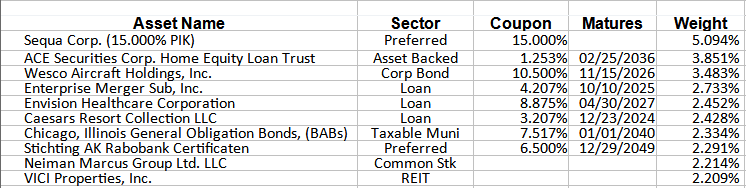

Top holdings

PIMCO; compiled by Author

The Top 10 equal 29% of the portfolio weight, out of 941 assets. Note that the largest holding is not paying that 15% coupon in cash, but in more bonds. Along with the assets for investment purposes, PCN holds 22 Currency Forwards, 22 Interest Rate Swaps (both sides), and over 100 Reverse Repurchase Agreements in support of the leverage employed.

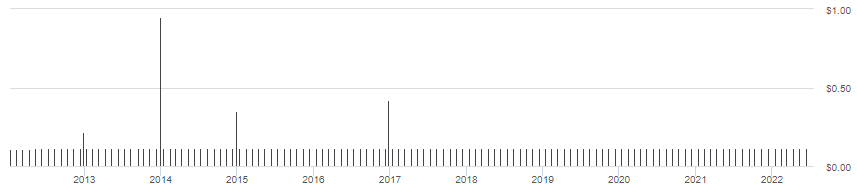

Distribution review

PCN DVDs (Seeking Alpha)

The monthly payout has been at $.1125 for over ten years now, and no special payout has occurred since late 2017. The UNII report shows PCN increasing their coverage ratio from the prior 6- and 12-month levels.

UNII xls (PIMCO)

Unlike like CEFs from other managers, PIMCO CEFs do not show any tendency to use a Managed Distribution Policy. I saw no indication that any of the payouts required ROC funds.

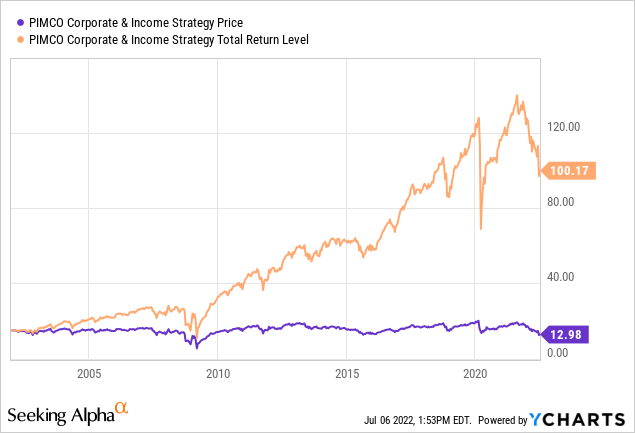

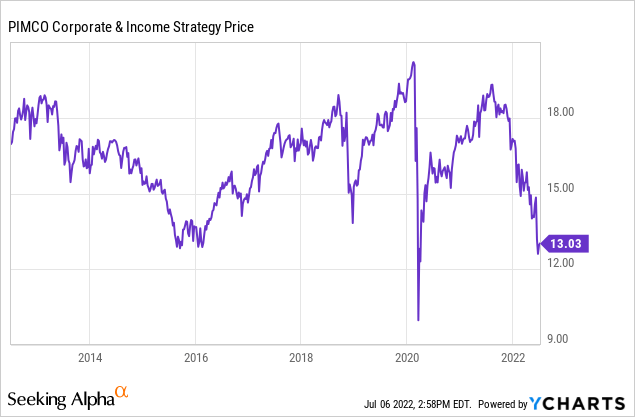

Price and NAV review

Since it started, PCN is currently showing a price loss of around $2/share. Investors who reinvested their payouts have experienced a 9.5% CAGR, versus only a 5.4% CAGR for those who did not.

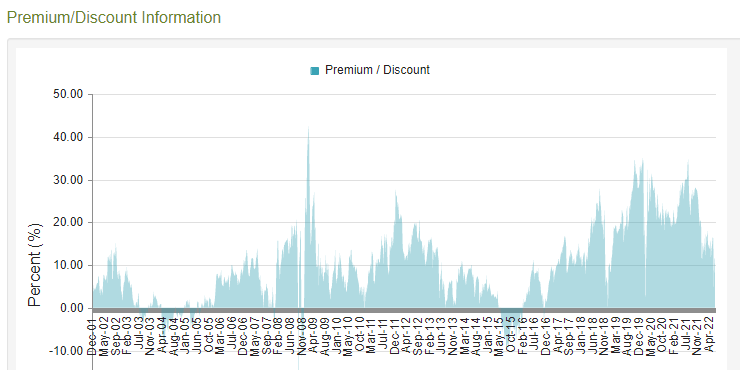

CEFConnect

PCN is one of those PIMCO CEFs that trades above PAR most of the time. That said, the current 11.91% premium, while down from over 30% recently, is still above the average for this fund.

Portfolio strategy

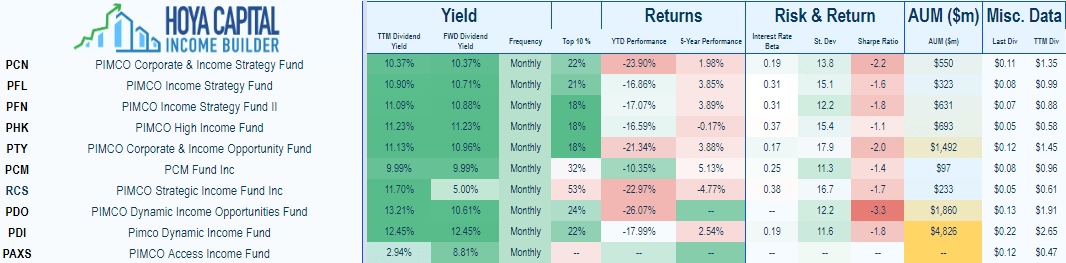

As I was writing this, the Wall Street Journal reported that commodity prices were trending downward as the second quarter closed compared to where they were at the start of the quarter; the implication being we might see smaller Fed hikes going forward than anticipated. If so, maybe the price and NAV damage to Fixed Income funds will slow or even recapture some of the declines experienced since last fall. At times like this, a fund’s asset mix and duration/maturity allocations become more important, i.e., have we reached the point where fixed rates are better than floating rate debt and are longer duration funds again where investors want to be? I never went beyond ECON 101 in college, so I won’t attempt to answer my own question, but here is a list of all the PIMCO Corporate and Multi-Sector CEFs to compare PCN against.

PIMCO; compiled by Author

Despite my concern that PCN’s premium is over 11%, PIMCO has other CEFs at even higher levels; only two currently trade at a discount. One thing investors would want to check is what each CEF’s top premium levels have been and how low they have gone; Z-scores are useful for evaluating this factor. The next table provides other useful data points to compare funds.

Hoya Capital Income Builder

Final thought

With the exception of those who caught the COVID bottom, PCN investors probably are sitting on a capital loss on this CEF. If owned in a taxable account, one strategy would be to sell PCN and buy another PIMCO CEF to replace it. Five of the funds listed above have better returns over the last five years; a good set to start one’s due diligence with.

Be the first to comment