fotokostic/iStock via Getty Images

Investment Thesis

Nutrien (NYSE:NTR) is cheaply valued, but there’s more to this story than just a low valuation. On one hand, NTR is priced at 8x this year’s EPS. And that’s clearly a cheap multiple.

However, until potash prices start to firm up, investors will remain unenthused about NTR. Put another way, only the most patient investors are likely to have the stamina to continue with this trade.

Bull Thesis Didn’t Play Out

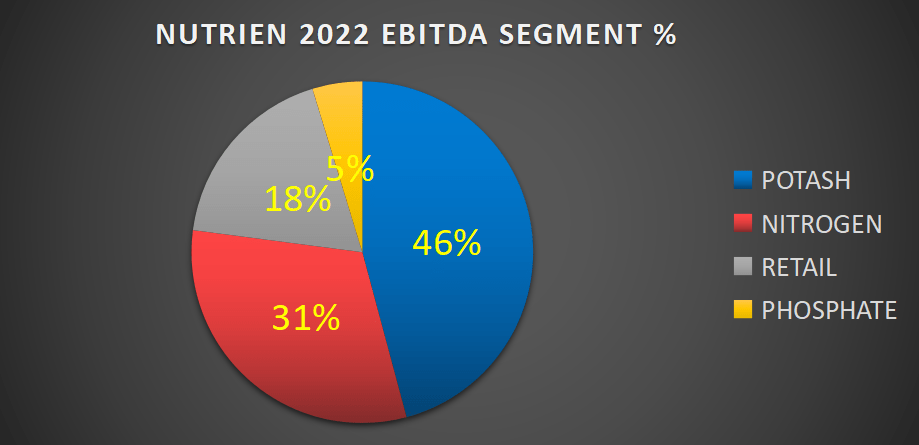

Nutrien finished Q4 2022 with the following breakdown, where you see that very close to half the bottom line profitability came from potash.

Author’s calculations, not including eliminations

This leads us to discuss expectations versus reality.

Anyone interested in this space knows the geopolitical drivers that caused the spiking of potash prices. Case in point, there was a substantial question as to the reliable supply of potash after February 2022.

Furthermore, there was the perception that it would be difficult to get buy potash from Russia. This translated into strong potash prices.

Meanwhile, farmers decided that with potash, and other fertilizer crops being elevated, they sought to minimize their inventory consumption. The focus here is on potash, but other fertilizers such as nitrogen were also impacted. Albeit through more indirect drivers, including high energy prices.

Nonetheless, to put it blankly, there was a thesis unfolding that created a lot of excitement. However, that thesis didn’t play out as expected.

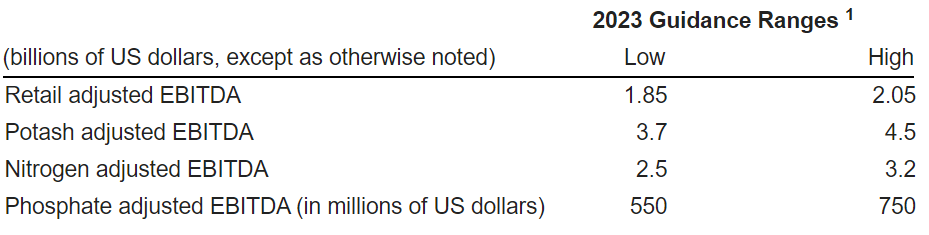

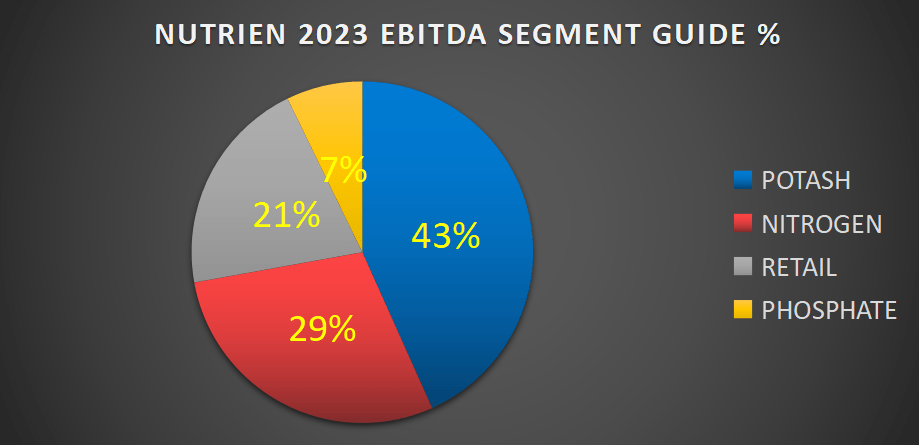

With this context in mind, let’s take on board Nutrien’s guidance.

What you see here is that potash EBITDA is guided for about $4 billion, down approximately 30% y/y from 2022.

NTR Q4 2022

Accordingly, let’s now turn our discussion to how this will impact Nutrient’s profitability in 2023.

Author’s calculations, not including eliminations

As you can see above, Nutrien’s biggest segment, its potash segment, is going to shrink meaningfully in 2023.

So, now that we have more visibility into 2023, let me make something clear. Painfully clear.

2022 Was a Black Swan, It Will Not Repeat

Implicitly or explicitly, many Nutrien investors got involved with Nutrien because they bought into a narrative that didn’t play out. Many people assumed there would be a re-run of the 2007 playbook, where potash prices would soar.

And when Russia’s invasion took place, many investors thought that history would repeat itself. The problem with the market is that it doesn’t repeat itself.

All that being said, I’m not convinced that this is where the story ends. Yes, that charge and intensity in the shortage of grain haven’t played out. The animal spirits and investor flows are not repositioning back into the fertilizer trade.

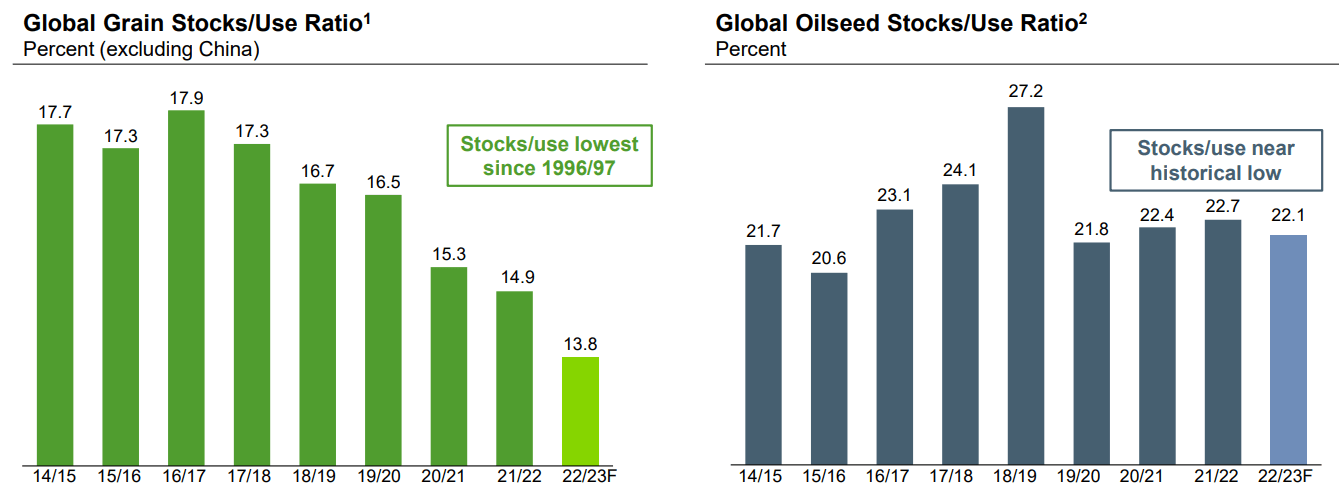

That being said, consider the graphics that follow, showing the global grain stocks/use ratio.

NTR Q4 2022

The stocks/use ratio is a supply-demand equation. A measure of the relationship between the amount of a commodity that is held in inventory versus the amount consumed.

A low stock-to-usage ratio means there’s tightness. While oilseed stocks are ”only” at the low end of their 5-year range, grain stocks are the lowest in a quarter of a century.

So yes, we all understand, the trade didn’t play out how we thought it would. But surely, the whole argument with a demand-supply equation is that even though customers are not motivated to buy what they need right now, there’s nevertheless a significant amount of price inelasticity in this fertilizer equation. Farmers have to buy, particularly when crop yields are so high.

On the other, the word cautious was heard 10 times on the earnings call. So, we can all pretend and wish that the thesis is about to play out, but I believe that in reality, we are all in a wait-and-see mode. But that’s ok too.

NTR Stock Valuation – Roughly 8x EPS

On the surface, NTR is cheap. But cheap stocks can always get cheaper.

NTR guidance

As you can see here, NTR is priced very roughly at 8x this year’s EPS. That being said, keep in mind that NTR’s guidance points towards its EPS figure coming down approximately 20% y/y.

So everyone can recognize that NTR is not expensive. But until investors actually see farmers returning to restock their inventory, Nutrien will require its shareholders to be patient.

The Bottom Line

I’ve been a focal bull of Nutrien for a while. And indeed, I strongly believe that you do not learn anything about investing when you make the right call. When you make a good call and the stock goes up, you’ve not learned anything.

It’s only when you have a thesis, and it doesn’t unfold the way you thought it would, that you actually learn something. Call it the cost of your tuition.

On yet the other hand, while I recognize that patience is the most expensive commodity an investor can be asked to pay, I believe that in 6 to 12 months, we’ll all be having a very different and more positive discussion when it comes to NTR.

Be the first to comment