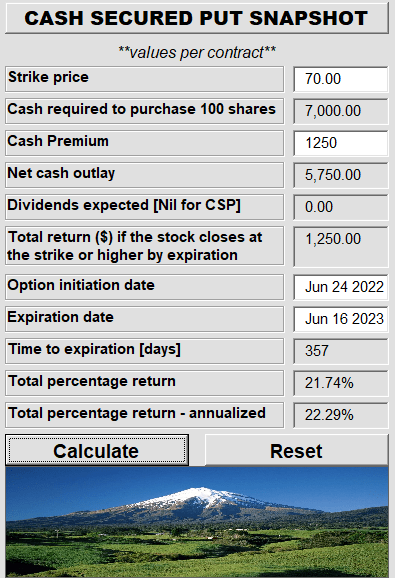

When we last covered PayPal Holdings, Inc. (NASDAQ:PYPL) we argued that the stock, while down from its highs, offered poor return prospects. We suggested that investors bullish the stock, instead consider using the cash secured puts. Our idea back then was to go for the $70 strike cash secured puts, for July 2023.

Investors need to throw out the past growth which is not coming back. They also need to throw out the past multiple which is never ever coming back. Rather than buy a stock where the return profile is 5-7% annual returns for the long run, we can get a 22.29% annualized return, even if the stock drops from here.

The cash secured puts we suggested are now trading near $8.00. So, if you sold them, you would be sitting on a small profit and handily beating the stock. We tell you where we would go next by examining the Q3-2022 results.

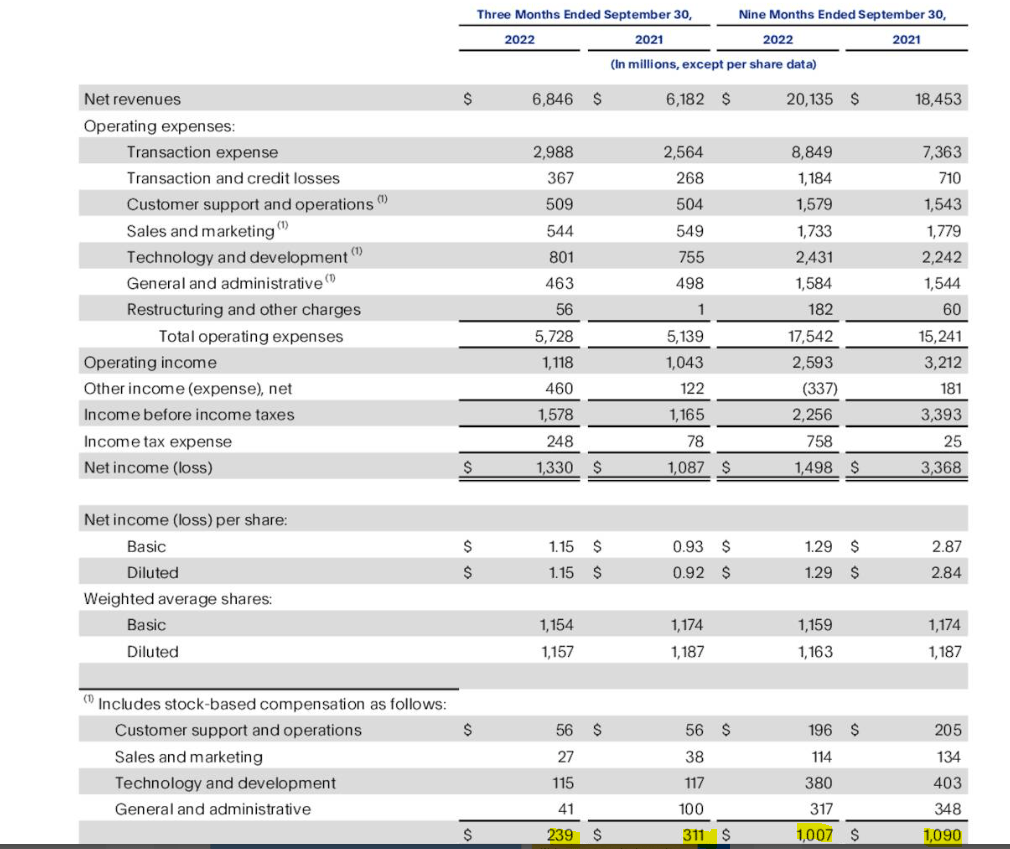

Revenues Coming In Tepid

11% or 12% revenue growth may not be considered tepid by many, but we think these numbers are just that.

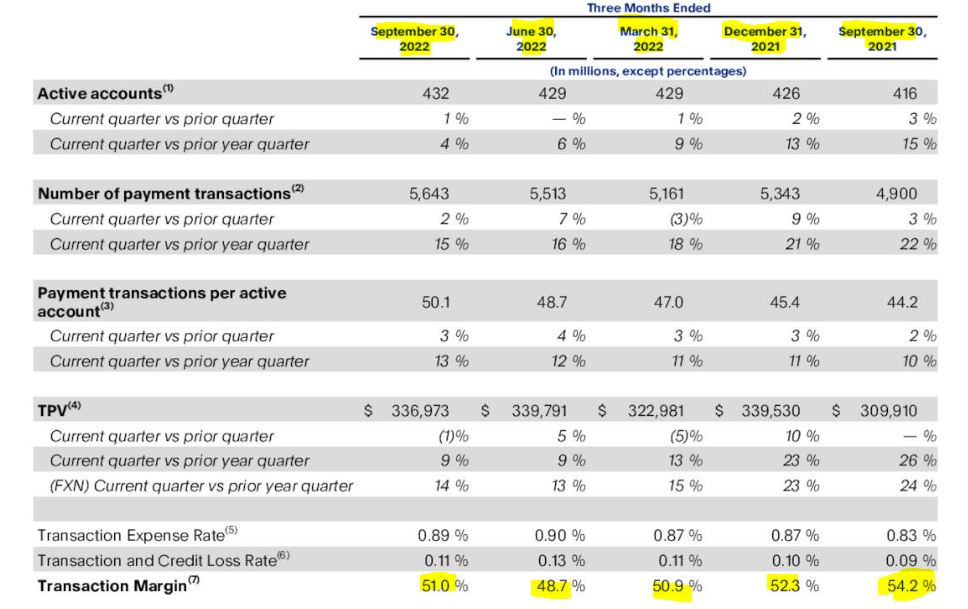

PYPL Q3-2022 Presentation

We have real GDP growth of around 2% and inflation measures near 9%. So nominal GDP is rising at a 11% rate. For a transaction processor, a 11% revenue run-rate is about as mediocre as you can get in this environment and that is what PYPL delivered. A perfectly middling experience. The stock was down as other sales metric were notably weaker including total payment volume that slipped quarter over quarter.

Margins Are The Story For This Year And The Next Two

Why was PYPL offering such poor return prospects this year? The answer was that in a bubble, margins, just like investor egos, are inflated. In April of this year, we suggested that PYPL’s margins would drop like a rock and anyone pricing this off those 2021 margins would be disappointed.

We expect PYPL’s gross margins to drop decisively below 50% in 2022 and stay there. At the end of the day, we think PYPL’s 2022 and 2023 earnings, and we are referring to the Non-GAAP version, will come in below that of 2021. Two years of no growth will require a big mindset change to absorb and we don’t think the stock will make headway with a legion of analysts downgrading it.

We saw the drop in 2022 but PYPL’s third quarter was actually far better than what we expected in this regard.

PYPL Q3-2022 Presentation

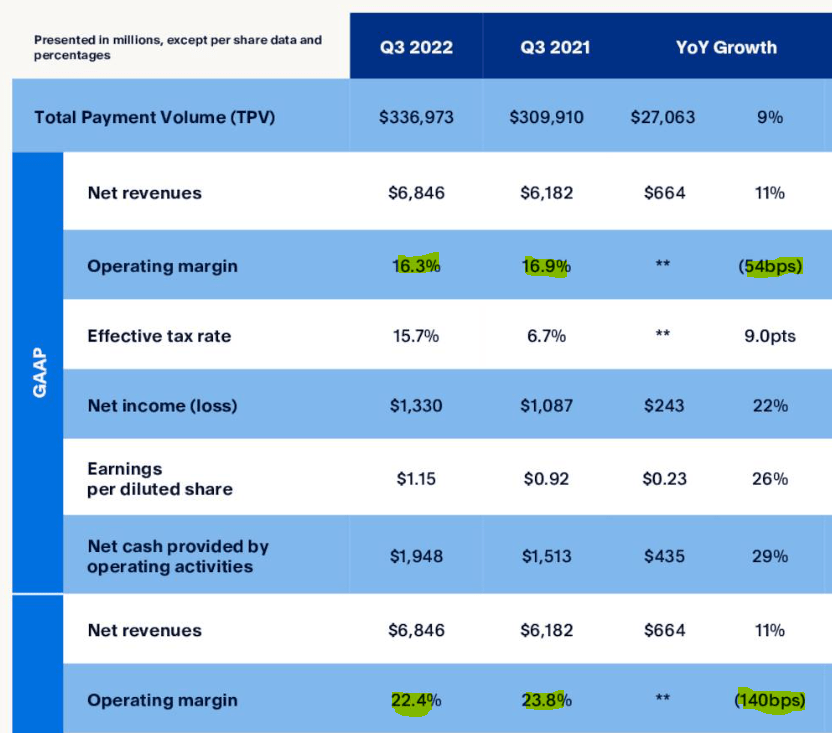

A number over 50% (while down from Q3-2021) suggests that the franchise strength is holding up well despite assaults on multiple fronts from competitors. Operating margins were also down year over year, in both GAAP and non-GAAP terms, but again a shade ahead of our estimates.

PYPL Q3-2022 Presentation

The next few quarters will still be telling as we think margins are still too high for this network. A 5-percentage point drop in gross margins and a similar drop in operating margins will spell a whole new disaster for even long positions at this level as it will crater earnings.

Valuation

Growth is gone. Non-GAAP earnings estimates are now for $4.08 in 2022 vs $4.60 in 2021. The crowd is expecting $4.77 for 2023 and we think that circled analyst at the low-end is likely to be correct.

Seeking Alpha

If that is the case, we would be looking at two years of declining earnings. That makes it tough to value PYPL as a growth stock. Of course, at 16-18X earnings, the value crowd starts to nibble at potential growth stories. We don’t think that number is accurate as it ignores the massive stock-based compensation.

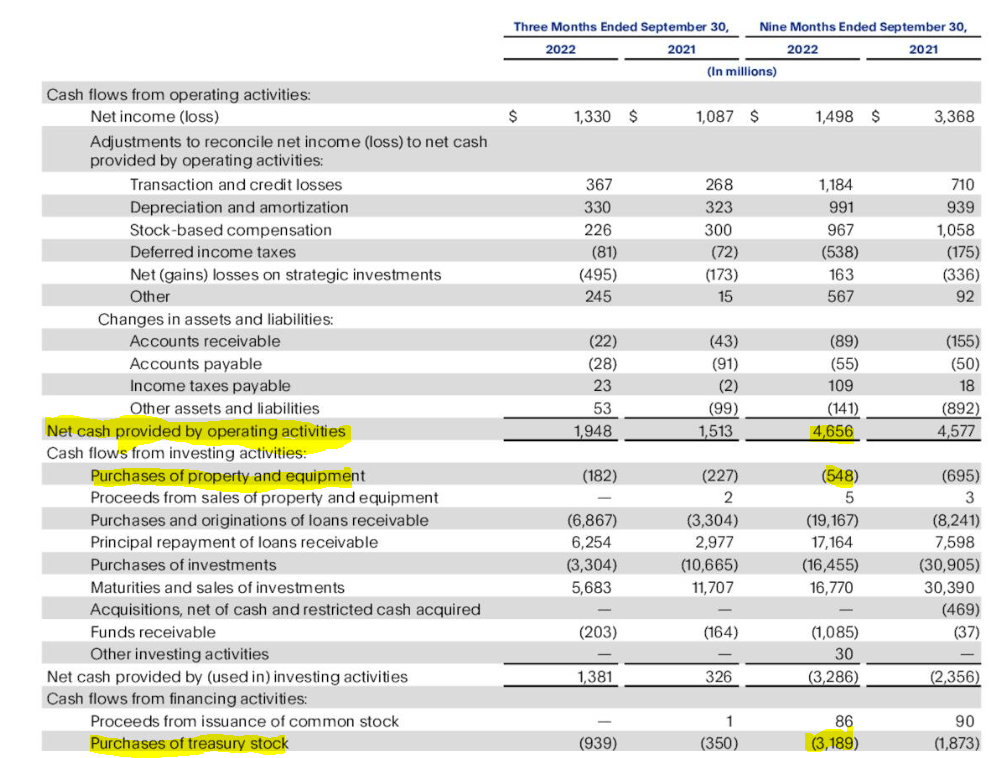

PYPL Q3-2022 Presentation

That compensation is running at about $1.4 billion a year. The best way to value PYPL is to look at adjusted free cash flow yield. That is free cash flow yield adjusted for stock-based compensation. This is calculated by taking free cash flow and then subtracting out stock-based compensation. PYPL spend this amount of free cash flow just keeping share counts from getting diluted, so this is a very fair metric. If we use $6.0 billion for operating cash flow, $700 million for property and equipment purchase and $1.4 billion of treasury stock purchases required to keep share count flat, you get about $4.0 billion in annual free cash flow. Note that actual buybacks are already way higher than that year to date, but we are looking at the amount required to offset stock-based compensation.

PYPL Q3-2022 Presentation

The $4 billion in annual free cash flow actually gets us right back to a 17X multiple on the stock.

PYPL is fairly valued today and unlikely to move much higher. Downside risks stem from margin compression and a possible recession. At 5% risk free rates, one could argue that PYPL should be valued at a 13-15X free cash flow multiple, especially since there is growth on the immediate horizon. We rate the stock at neutral/hold. We would now consider option entries only at $60 or lower and would close out our earlier suggested cash secured puts for $70 strike.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment