Ridofranz/iStock via Getty Images

If you must speak ill of another, do not speak it, write it in the sand near the water’s edge. ― Napoleon Hill

Today, we are circling back on Paratek Pharmaceuticals (NASDAQ:PRTK) for the first time since we posted this piece on this small antibiotic concern back in October of last year. Even as the company has demonstrated solid revenue growth, shareholders have not been rewarded in this name over the past year and patience is starting to wear thin. We update our investment thesis around Paratek Pharmaceuticals via the analysis below.

Seeking Alpha

Company Overview

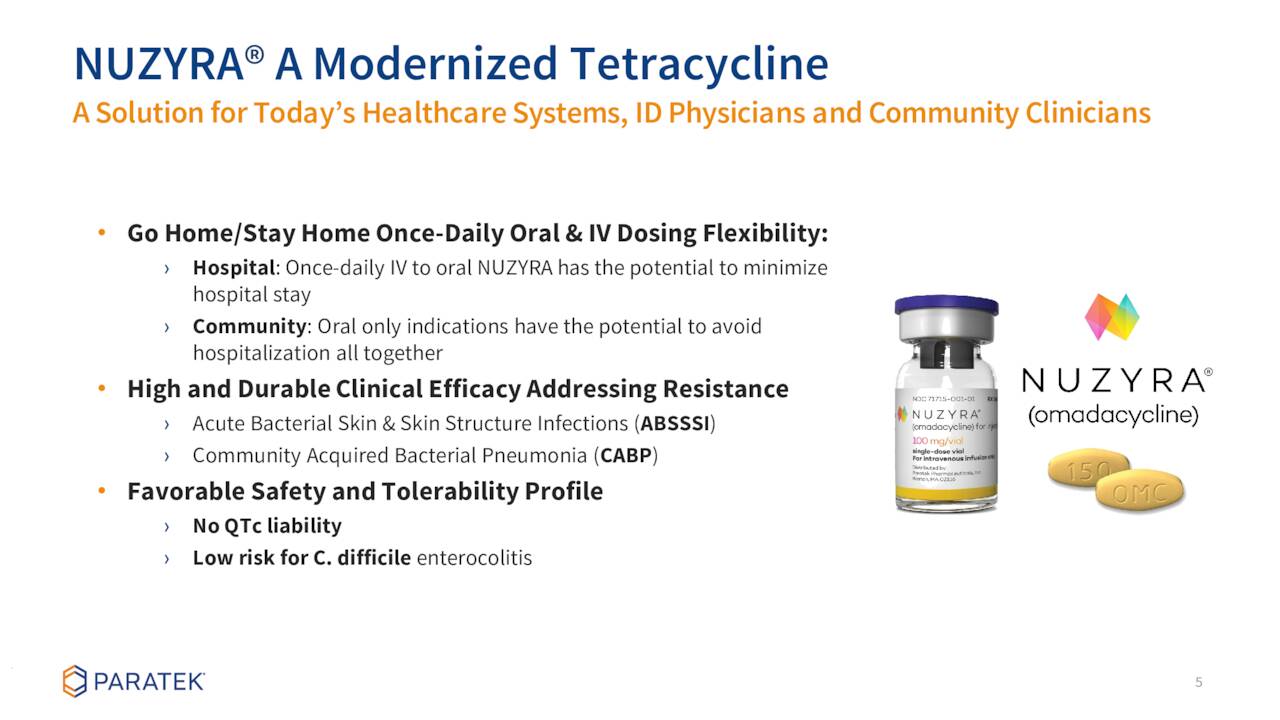

Paratek Pharmaceuticals is a Boston based antibiotic concern. The company’s primary asset is NUZYRA. This is a once-daily oral and intravenous broad-spectrum antibiotic approved for the treatment of adult patients with community-acquired bacterial pneumonia and acute bacterial skin and skin structure infections caused by susceptible pathogens. The stock sells for around $2.75 a share and sports an approximate market cap of just under $150 million.

August Company Presentation

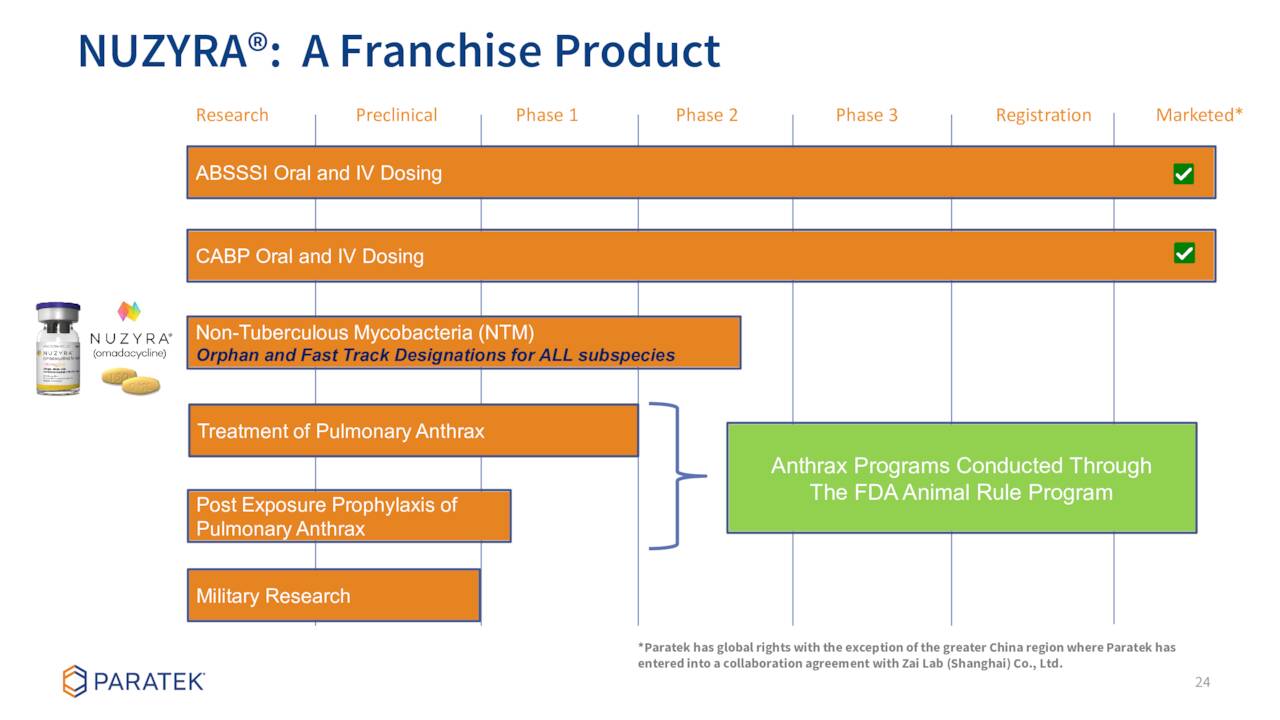

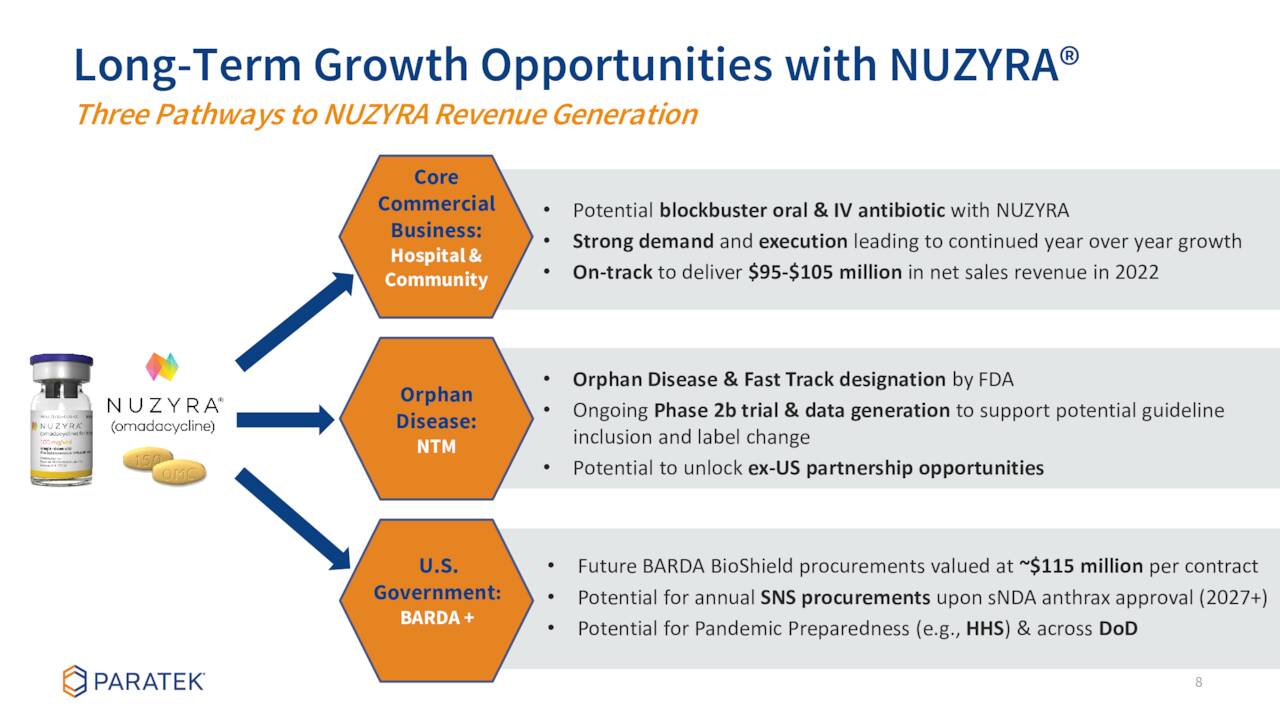

The company has some earlier stage candidates in its pipeline. None of them of note to this analysis given they are early in development. The company is advancing NUZYRA in Phase 2 development for Non-Tuberculous Mycobacteria or NTM for which it has Orphan Drug and Fast Track designations from the FDA.

August Company Presentation

Second Quarter Results

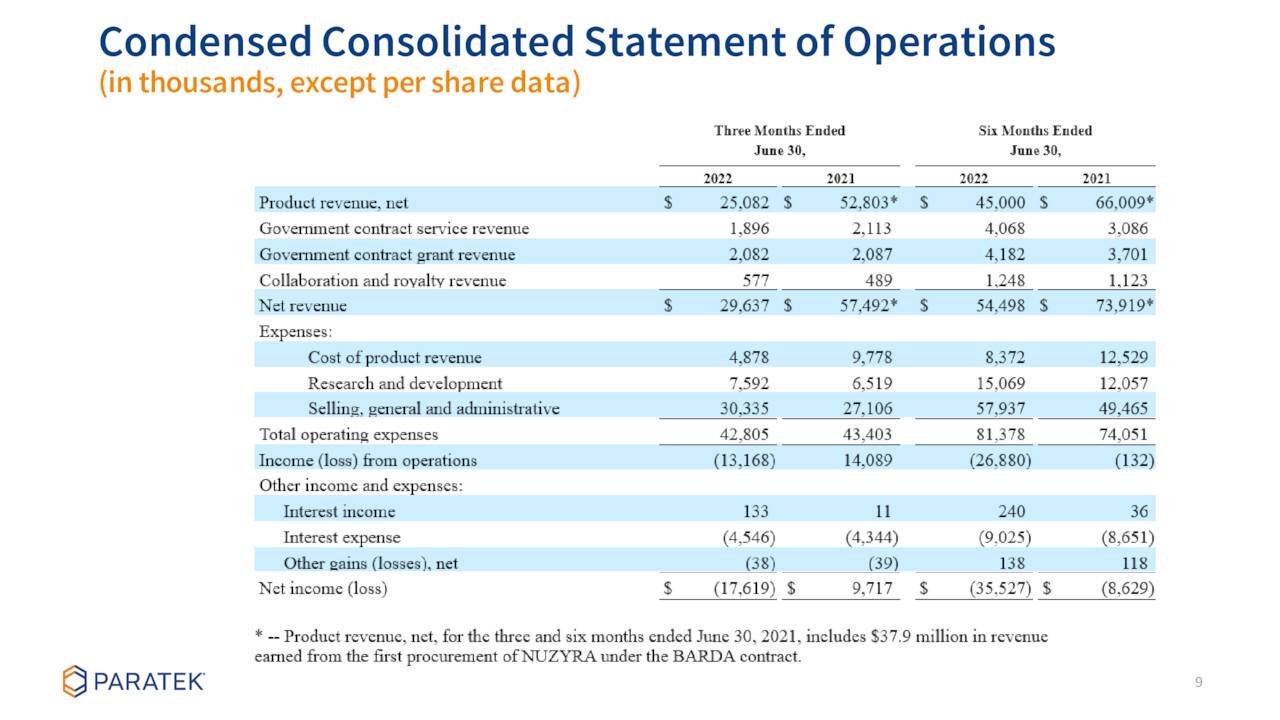

On August 3rd, the company posted second quarter numbers. Paratek posted a GAAP loss of 33 cents a share, just a tad above the consensus. Net revenue for the second quarter of 2022 was $29.6 million. This compares to $19.6 million in 2Q2021 when excluding the first procurement of NUZYRA under the BARDA contract of $37.9 million (more detail on that contract in the last section of this article).

August Company Presentation

The $29.6 million in sales for the quarter included $25.1 million of revenues from NUZYRA’s core commercial business. This was up from $14.9 million from the same period a year ago. The company also booked $4 million in sales from the BARDA contract and $600,000 in royalty revenue from SEYSARA, a tetracycline designed for the treatment of moderate to severe acne vulgaris.

August Company Presentation

Analyst Commentary & Balance Sheet

Only three analyst firms have chimed in around Paratek so far in 2022. On February 10th, WBB Securities upgraded the shares to a Strong Buy with a $11 price target as the analyst there believes ‘Nuzyra is a critically important antibiotic that has anchored the franchise‘. This month BTIG ($30 price target) and H.C. Wainwright ($20 price target) both maintained their Buy ratings on the stock.

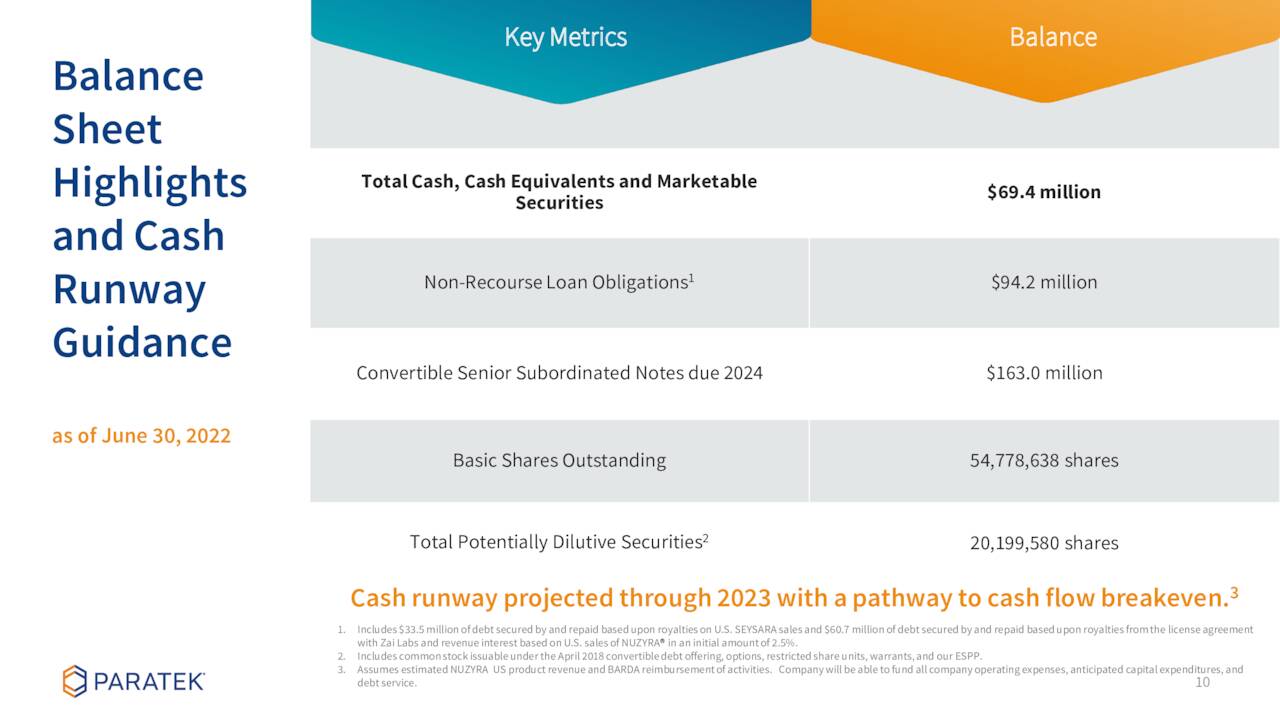

Just under 10% of the outstanding float is currently held short. Four insiders sold just over $300,000 worth of shares collectively in August. That has been the only insider activity in the equity so far in 2022. The company ended the first half of this year with nearly $70 million in cash and marketable securities on its balance sheet. Management stated within its second quarter earnings press release that:

Based upon the company’s current operating plan, Paratek anticipates its existing cash, cash equivalents and marketable securities of $69.4 million as of June 30, 2022, provides for a cash runway through the end of 2023 with a pathway to cash flow break-even.

August Company Presentation

Verdict

The current analyst consensus has the company losing a bit over 80 cents a share in FY2022 as revenues rise in the mid teens to some $150 million. Projections from three analyst firms that have provided estimates for FY2023 are in wide range both for earnings (A 42 cent a share loss to profits of $1.37 a share) and revenues ($195 million to $315 million).

August Company Presentation

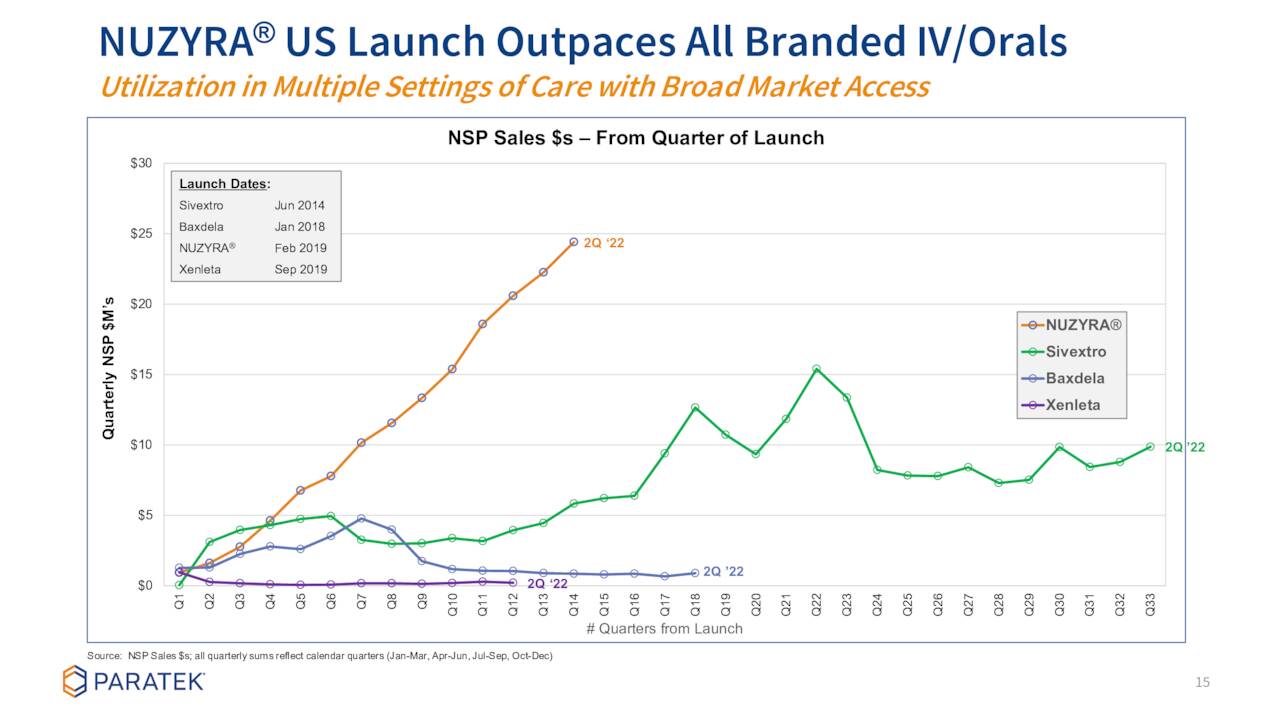

NUZYRA was launched in 2019 and has shown superior sales trajectory compared to the rest of the antibiotic space in this category. In addition, soon after this antibiotic’s approval, BARDA awarded Paratek a five-year contract, valued at up to $285 million for the development of NUZYRA for the treatment of pulmonary anthrax. This large contract provides some long-term tailwinds for NUZYRA sales growth.

August Company Presentation

All that said, the antibiotic space tends to be one that is hard to make a profit in despite the great need for these compounds.

August Company Presentation

NUZYRA does seem to have numerous growth drivers in place and leadership continues to insist funding is in place to get to cash flow break even status at some point in 2023. However, given the extent of quarterly losses, I take that view with a bit of a grain of salt. In addition, shareholders have to be somewhat concerned about the potential for dilution is 2024 from Paratek’s convertible senior subordinated notes due that year.

If we cut recent analyst price targets in half, PRTK would still be undervalued and valuation is very reasonable on a price to sales basis. Options are available against this equity and the March $2.50 call strikes are particularly liquid and lucrative at the moment. Therefore, I plan to continue to hold my small stake in PRTK via covered call orders for the potential upside as well as the downside risk mitigation available with this simple option strategy.

Patience can be bitter but her fruit is always sweet. ― Habeeb Akande

Be the first to comment